La prévision est un art difficile … surtout quand elle ... · La prévision est un art difficile...

74

P.Batteau ECCOREV Journée modélisation Février 2010 La prévision est un art difficile … surtout quand elle concerne l’avenir Mark Twain (Et Pierre Dac) Marchés financiers et climat Modéliser les extravagances

Transcript of La prévision est un art difficile … surtout quand elle ... · La prévision est un art difficile...

P.Batteau ECCOREV Journée modélisation Février 2010

La prévision est un art difficile … surtout quand elle concerne l’avenir

Mark Twain (Et Pierre Dac)

Marchés financiers et climat Modéliser les extravagances

P.Batteau ECCOREV Journée modélisation Février 2010

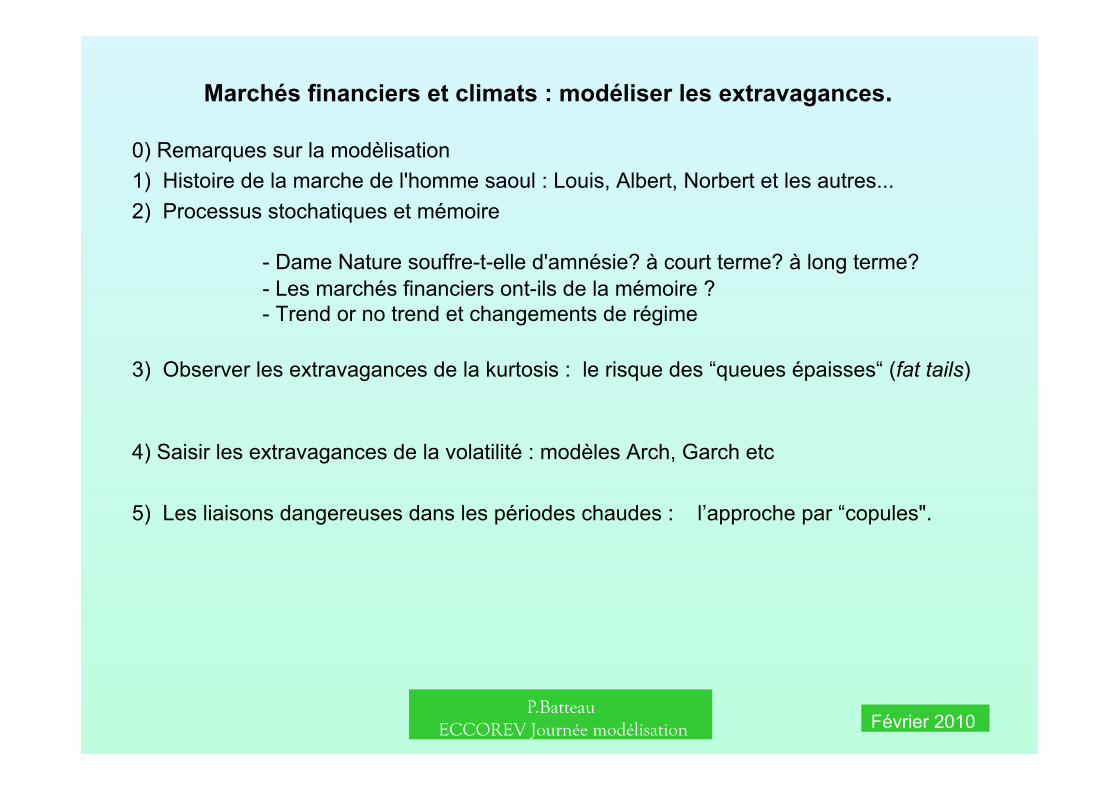

Marchés financiers et climats : modéliser les extravagances.

0) Remarques sur la modèlisation 1) Histoire de la marche de l'homme saoul : Louis, Albert, Norbert et les autres... 2) Processus stochatiques et mémoire

- Dame Nature souffre-t-elle d'amnésie? à court terme? à long terme? - Les marchés financiers ont-ils de la mémoire ? - Trend or no trend et changements de régime

3) Observer les extravagances de la kurtosis : le risque des “queues épaisses“ (fat tails)

4) Saisir les extravagances de la volatilité : modèles Arch, Garch etc

5) Les liaisons dangereuses dans les périodes chaudes : l’approche par “copules".

P.Batteau ECCOREV Journée modélisation Février 2010

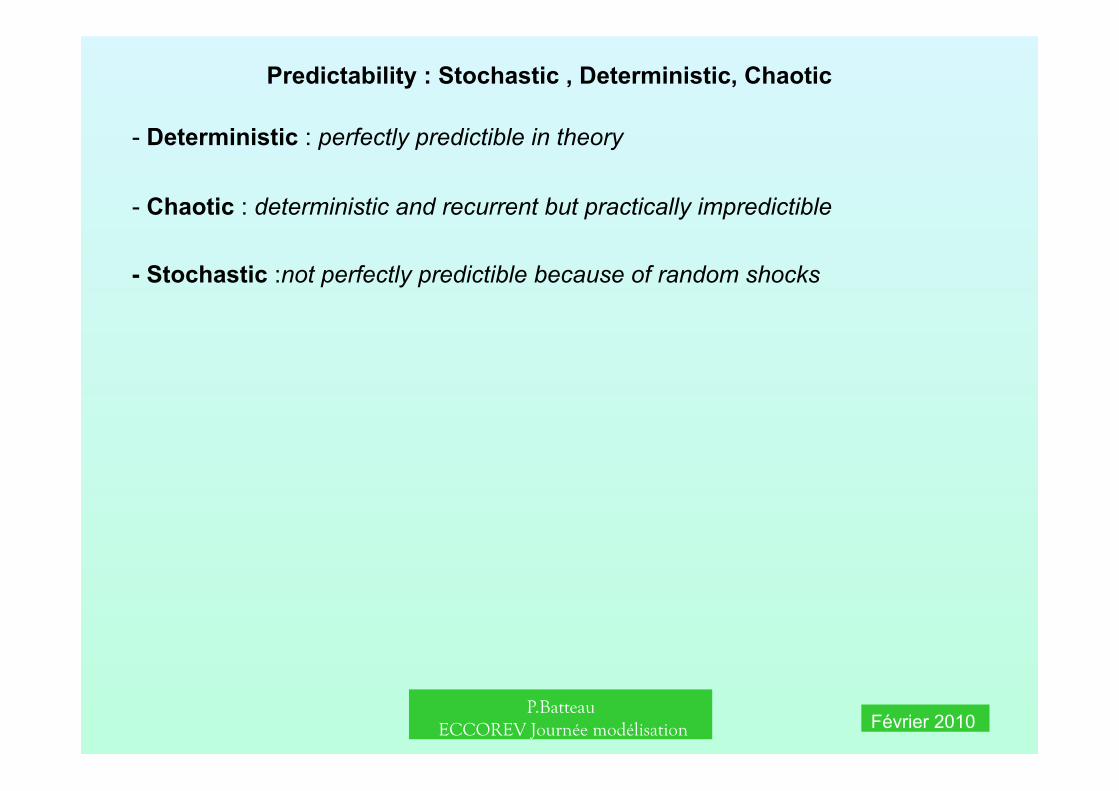

Predictability : Stochastic , Deterministic, Chaotic

- Deterministic : perfectly predictible in theory

- Chaotic : deterministic and recurrent but practically impredictible

- Stochastic :not perfectly predictible because of random shocks

P.Batteau ECCOREV Journée modélisation Février 2010

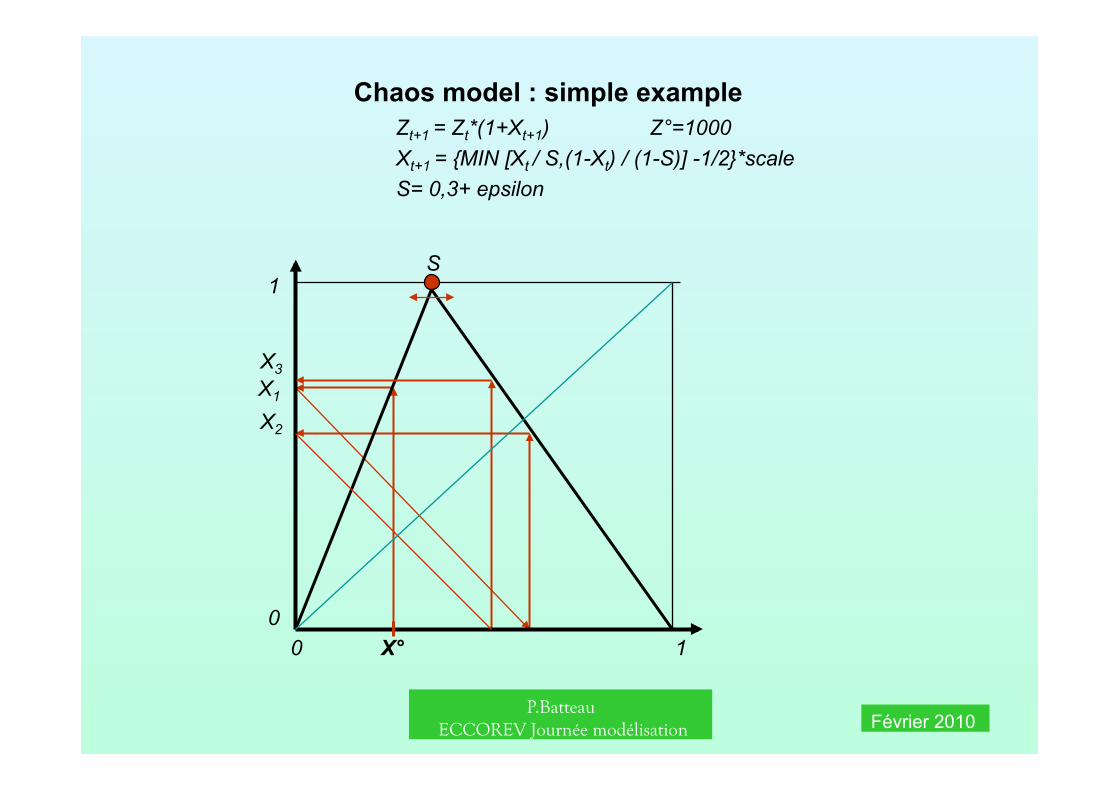

Chaos model : simple example Zt+1 = Zt*(1+Xt+1) Z°=1000 Xt+1 = {MIN [Xt / S,(1-Xt) / (1-S)] -1/2}*scale S= 0,3+ epsilon

0 1 0

1 S

X°

X1

X2

X3

P.Batteau ECCOREV Journée modélisation Février 2010

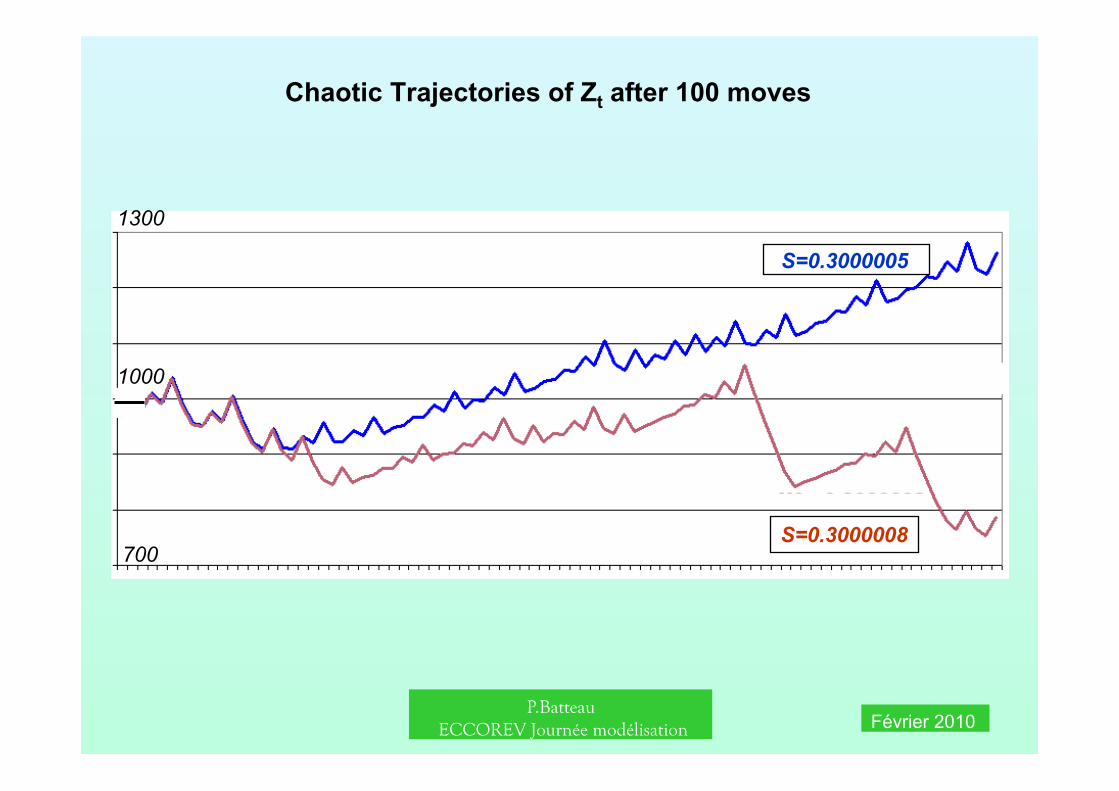

Chaotic Trajectories of Zt after 100 moves

700

1300

1000

S=0.3000005

S=0.3000008

P.Batteau ECCOREV Journée modélisation Février 2010

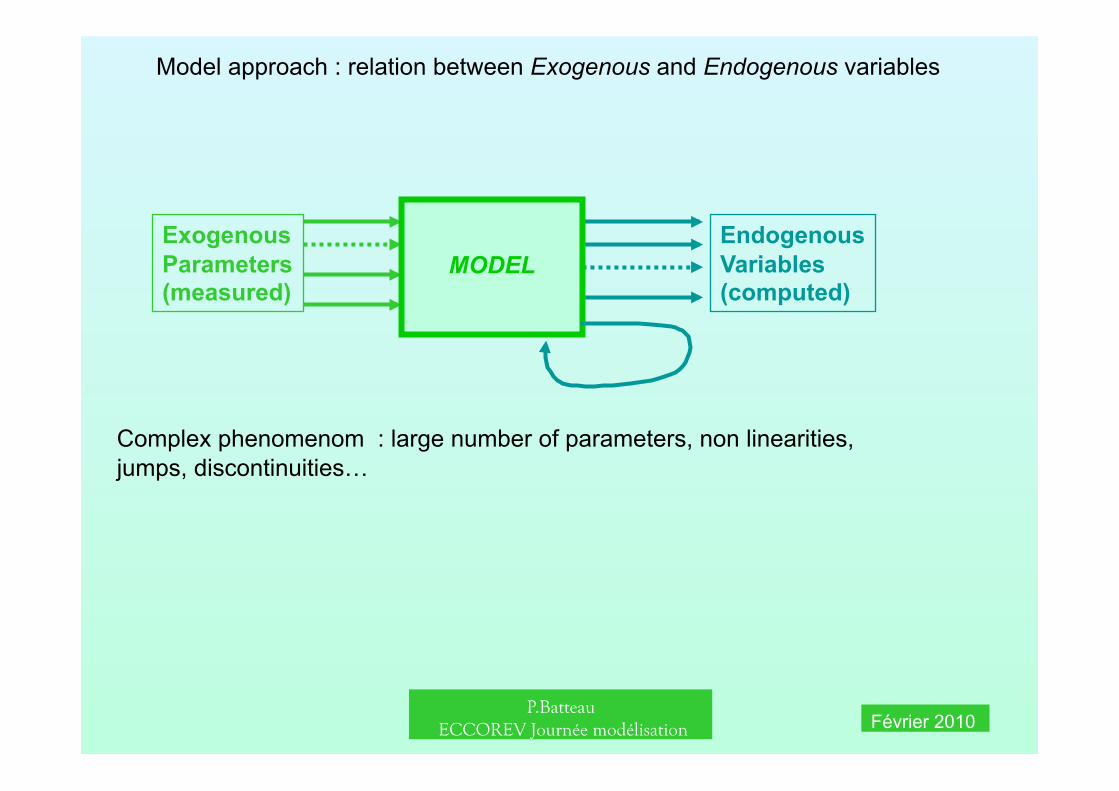

Model approach : relation between Exogenous and Endogenous variables

Endogenous Variables (computed)

Exogenous Parameters (measured)

MODEL

Complex phenomenom : large number of parameters, non linearities, jumps, discontinuities…

P.Batteau ECCOREV Journée modélisation Février 2010

Models of complex systems

P.Batteau ECCOREV Journée modélisation Février 2010

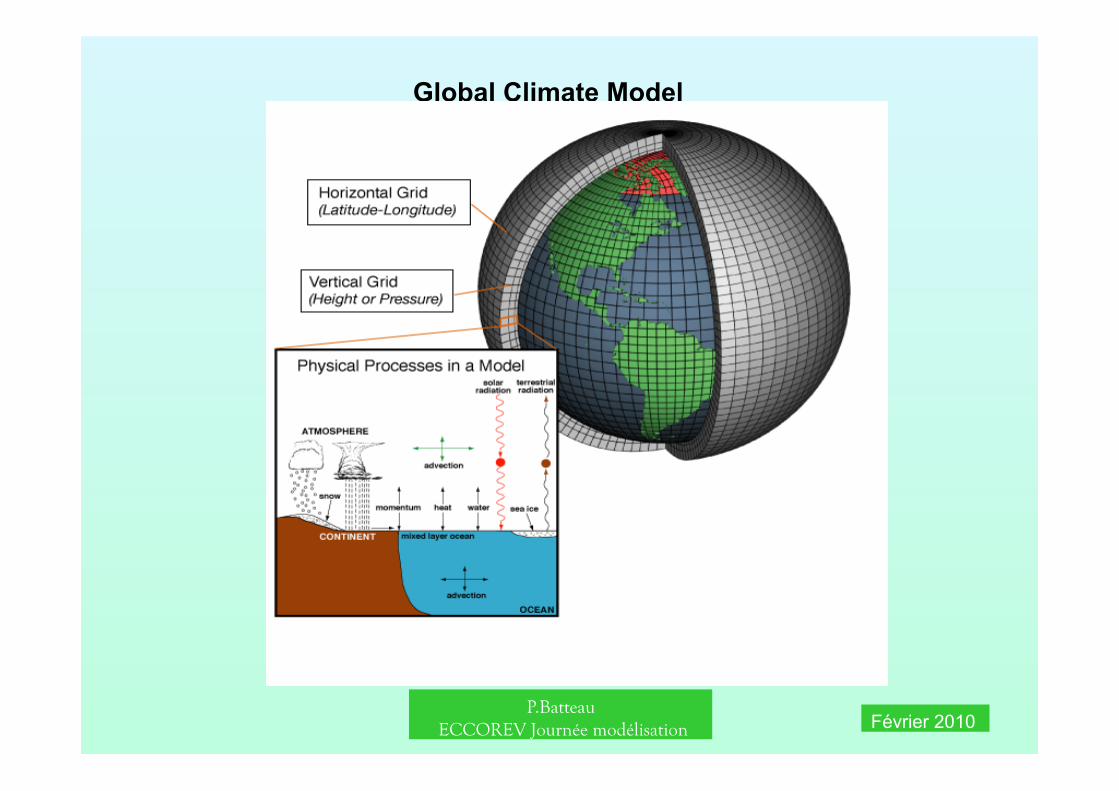

Global Climate Model

P.Batteau ECCOREV Journée modélisation Février 2010

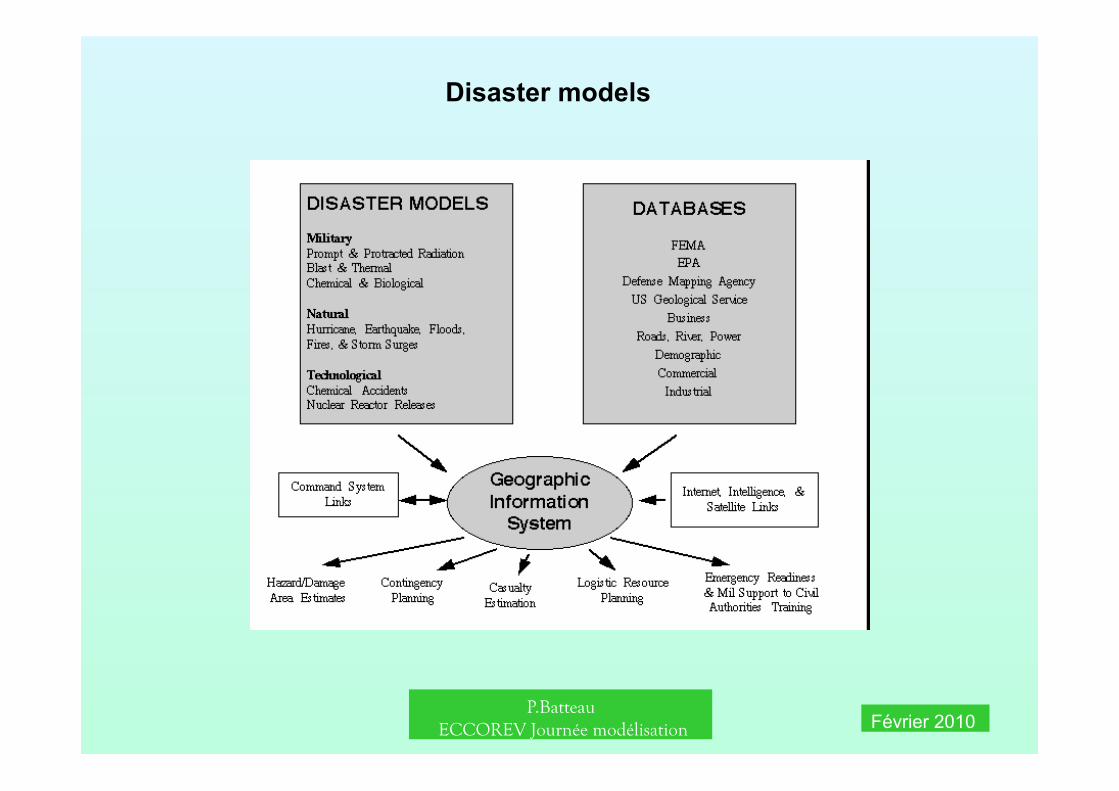

Disaster models

P.Batteau ECCOREV Journée modélisation Février 2010

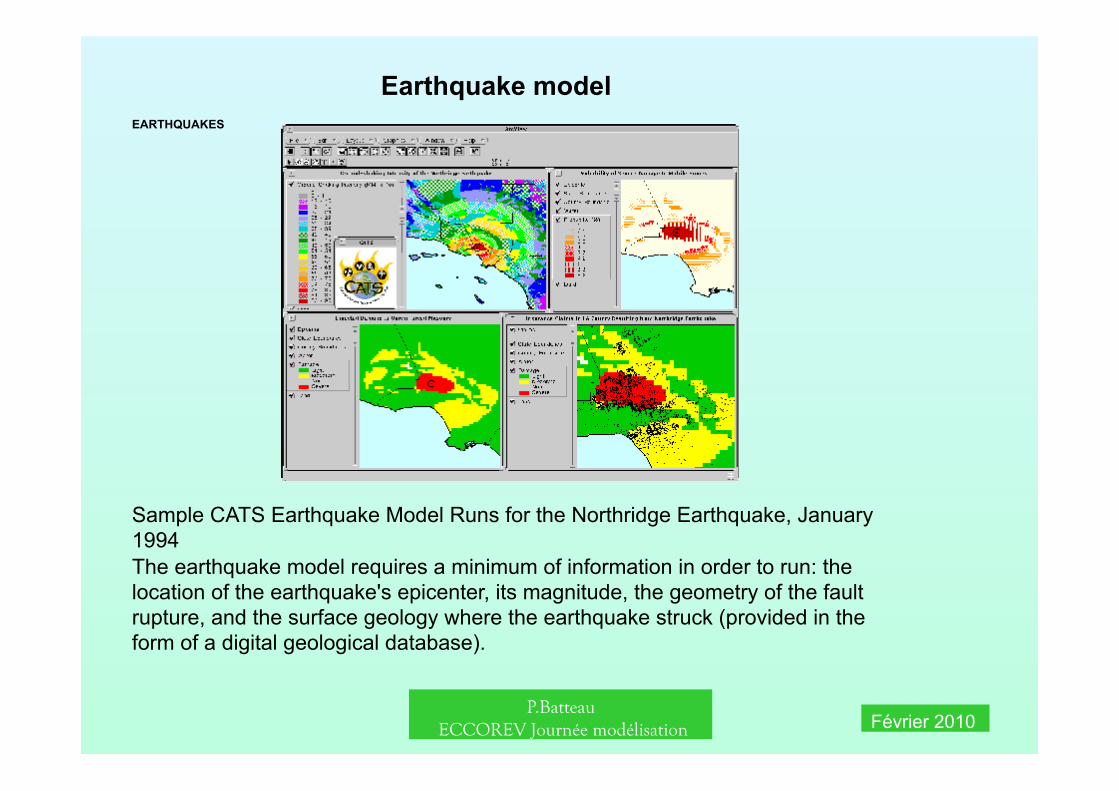

EARTHQUAKES

Sample CATS Earthquake Model Runs for the Northridge Earthquake, January 1994 The earthquake model requires a minimum of information in order to run: the location of the earthquake's epicenter, its magnitude, the geometry of the fault rupture, and the surface geology where the earthquake struck (provided in the form of a digital geological database).

Earthquake model

P.Batteau ECCOREV Journée modélisation Février 2010

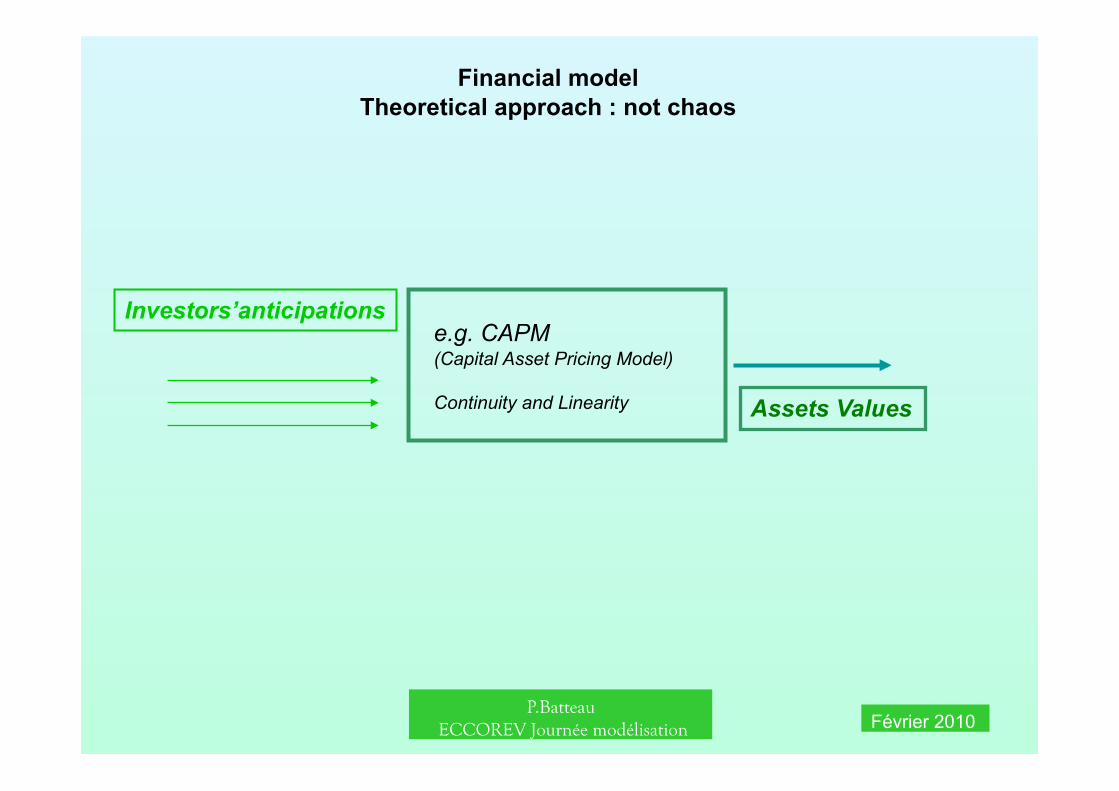

Financial model Theoretical approach : not chaos

Investors’anticipations

Assets Values

e.g. CAPM (Capital Asset Pricing Model)

Continuity and Linearity

P.Batteau ECCOREV Journée modélisation Février 2010

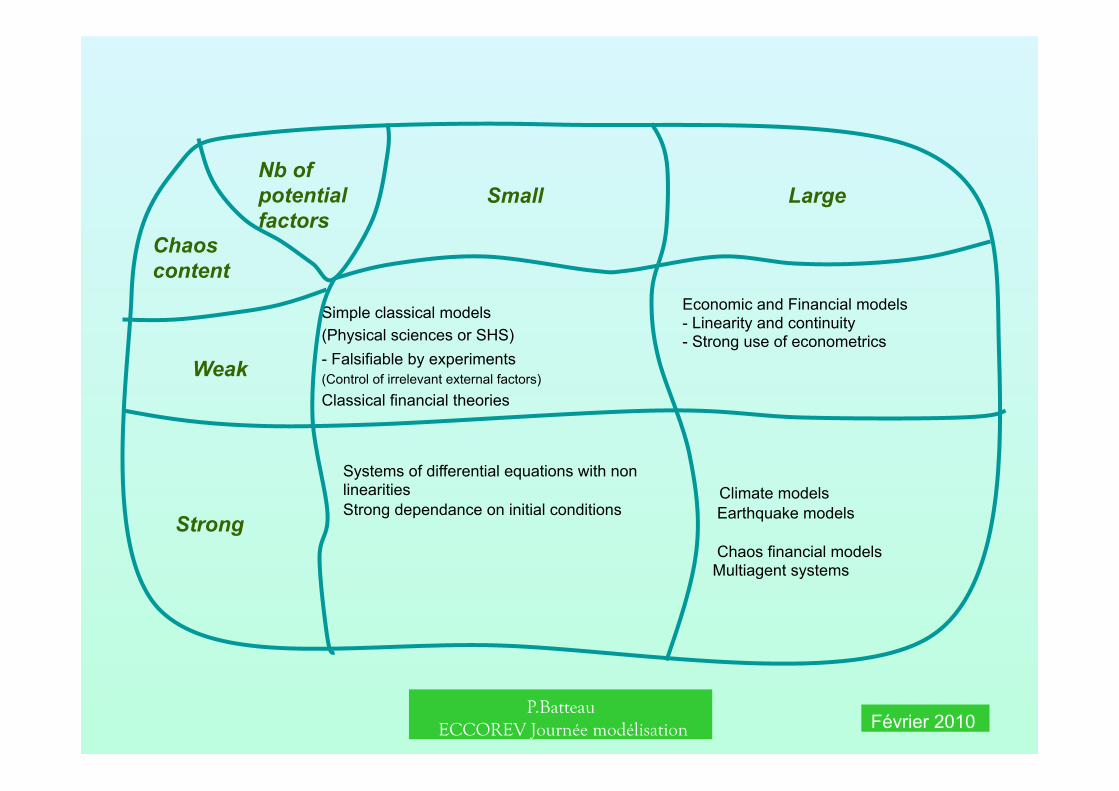

Simple classical models (Physical sciences or SHS) - Falsifiable by experiments (Control of irrelevant external factors) Classical financial theories

Economic and Financial models - Linearity and continuity - Strong use of econometrics

Systems of differential equations with non linearities Strong dependance on initial conditions

Climate models Earthquake models

Chaos financial models Multiagent systems

Small Large

Weak

Strong

Nb of potential factors

Chaos content

P.Batteau ECCOREV Journée modélisation Février 2010

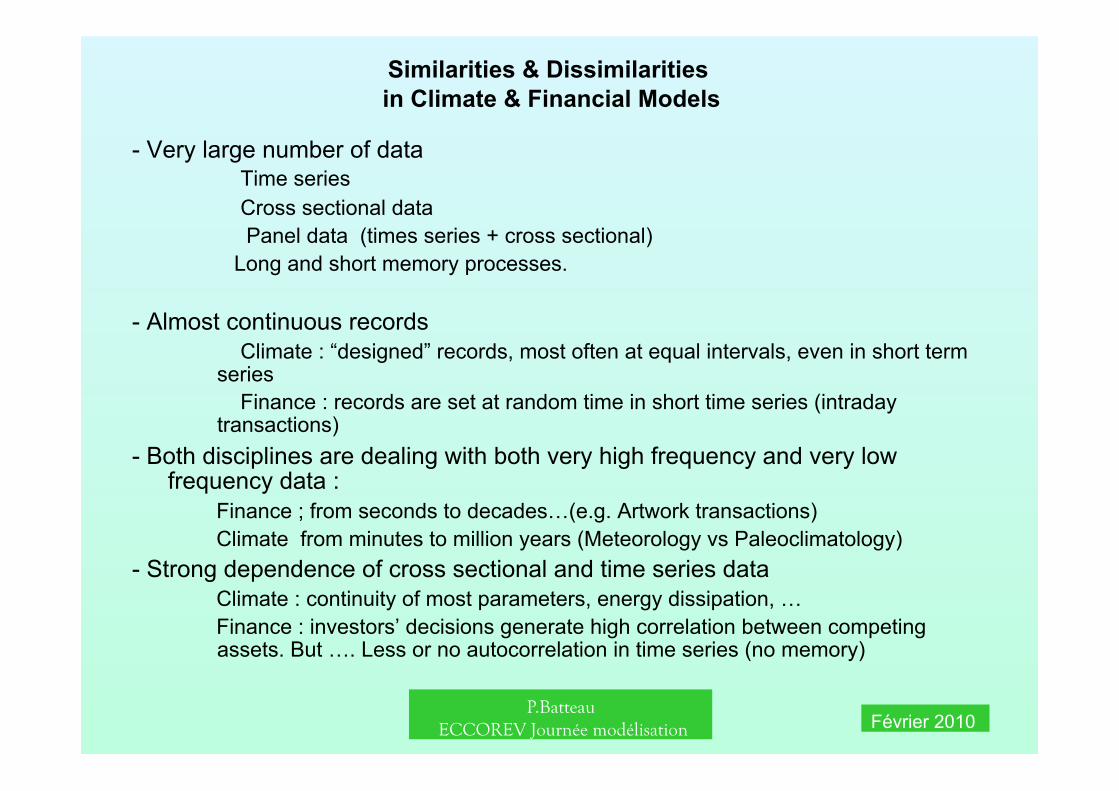

Similarities & Dissimilarities in Climate & Financial Models

- Very large number of data Time series Cross sectional data Panel data (times series + cross sectional) Long and short memory processes.

- Almost continuous records Climate : “designed” records, most often at equal intervals, even in short term series

Finance : records are set at random time in short time series (intraday transactions)

- Both disciplines are dealing with both very high frequency and very low frequency data :

Finance ; from seconds to decades…(e.g. Artwork transactions) Climate from minutes to million years (Meteorology vs Paleoclimatology)

- Strong dependence of cross sectional and time series data Climate : continuity of most parameters, energy dissipation, … Finance : investors’ decisions generate high correlation between competing assets. But …. Less or no autocorrelation in time series (no memory)

P.Batteau ECCOREV Journée modélisation Février 2010

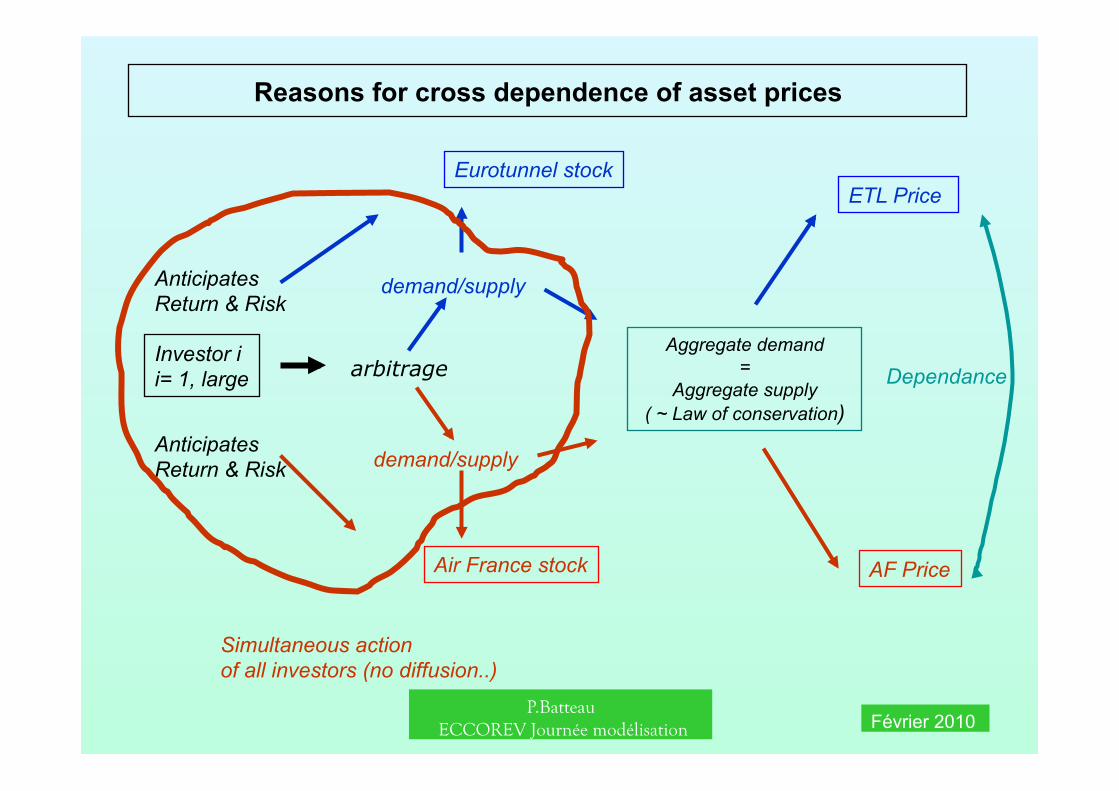

Reasons for cross dependence of asset prices

demand/supply

demand/supply

Investor i i= 1, large

Eurotunnel stock ETL Price

Air France stock

Aggregate demand =

Aggregate supply ( ~ Law of conservation)

AF Price

Dependance

Anticipates Return & Risk

Anticipates Return & Risk

arbitrage

Simultaneous action of all investors (no diffusion..)

P.Batteau ECCOREV Journée modélisation Février 2010

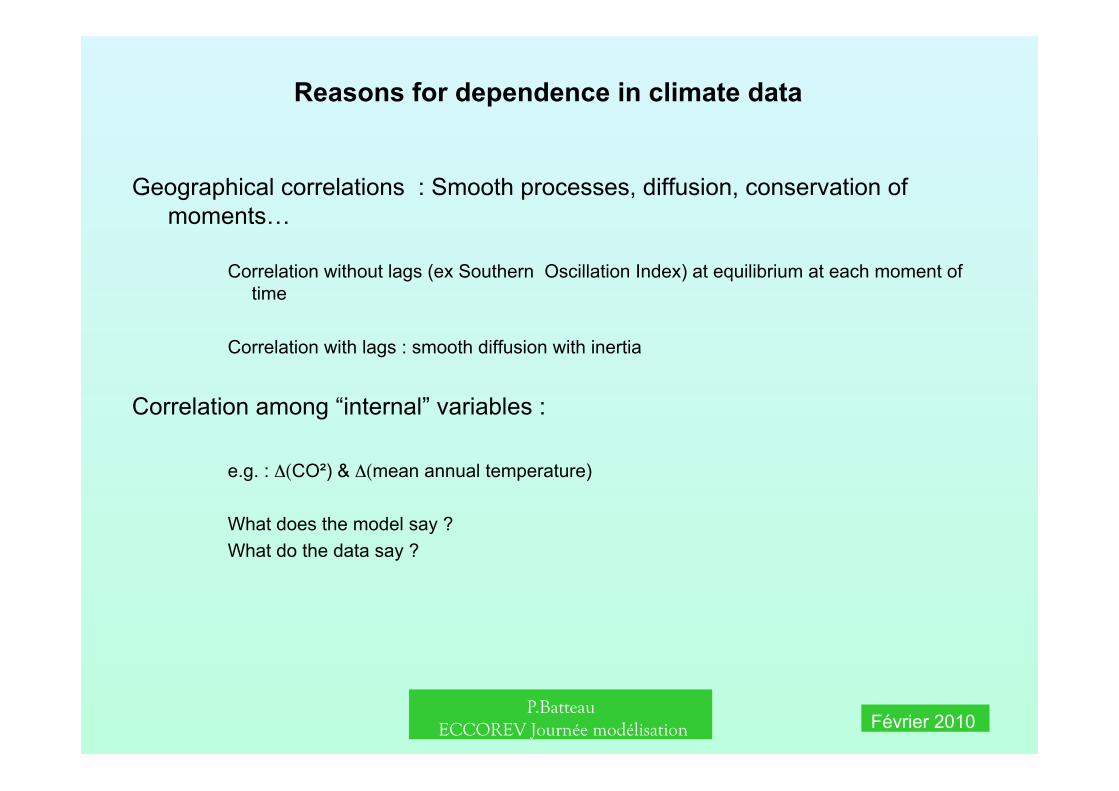

Reasons for dependence in climate data

Geographical correlations : Smooth processes, diffusion, conservation of moments…

Correlation without lags (ex Southern Oscillation Index) at equilibrium at each moment of time

Correlation with lags : smooth diffusion with inertia

Correlation among “internal” variables :

e.g. : Δ(CO²) & Δ(mean annual temperature)

What does the model say ? What do the data say ?

P.Batteau ECCOREV Journée modélisation Février 2010

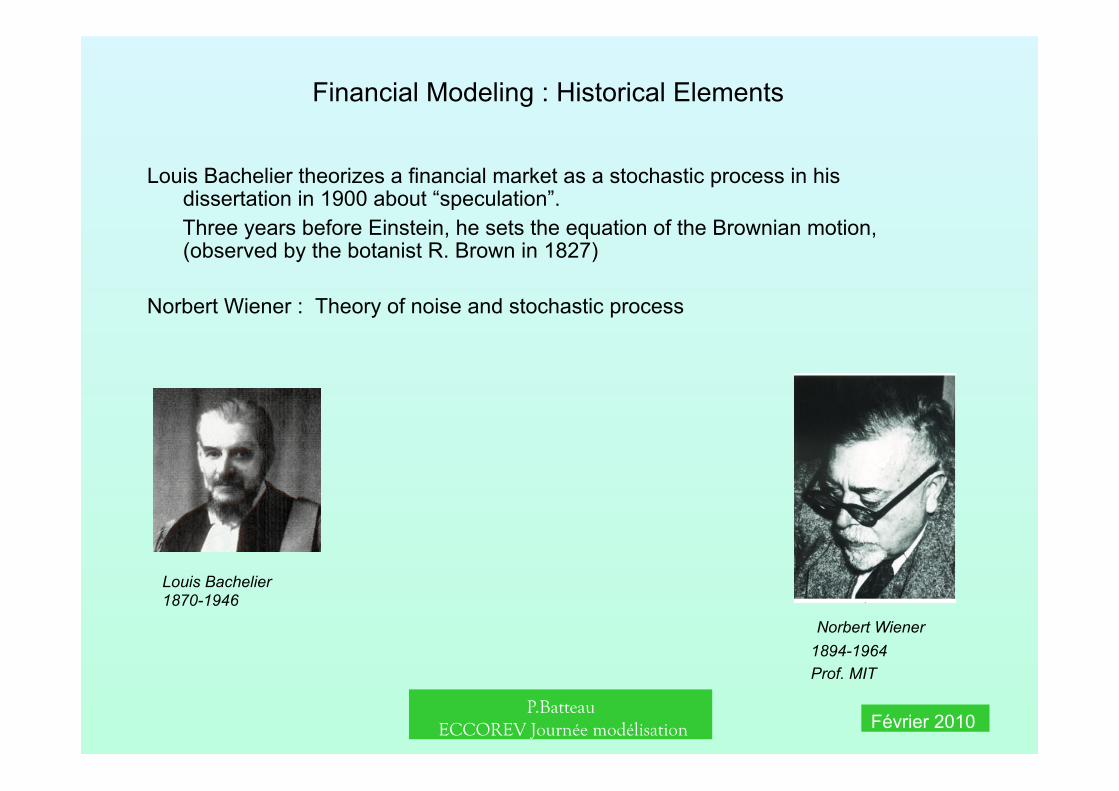

Financial Modeling : Historical Elements

Louis Bachelier theorizes a financial market as a stochastic process in his dissertation in 1900 about “speculation”.

Three years before Einstein, he sets the equation of the Brownian motion, (observed by the botanist R. Brown in 1827)

Norbert Wiener : Theory of noise and stochastic process

Norbert Wiener 1894-1964 Prof. MIT

Louis Bachelier 1870-1946

P.Batteau ECCOREV Journée modélisation Février 2010

Random Walk Properties

- For any ·t<t’<t” X(t”) – X(t’) and X(t’)- X(t) are independent variables (independent increments) -The distribution of the increment X(t + d) – X(t) does not depend on t (stationary increments) - The process {B(t) : t >0} has (almost surely) continuous paths.

Lemma :There exists a vector m and a matrix S such that for every t > 0 and d > 0 , B(t + h) - B(t) is multivariate normally distributed with

mean h and covariance matrix hm and hSSt

P.Batteau ECCOREV Journée modélisation Février 2010

Unidimensional Random Walk

X Y’

Y

1- X and Y are independent 2- Y and Y’ : same distribution 3 – X, Y, Y’ : normal distribution with variance proportional to time

X

P.Batteau ECCOREV Journée modélisation Février 2010

Brownian motion or Wiener process

Bt = value reached at time t

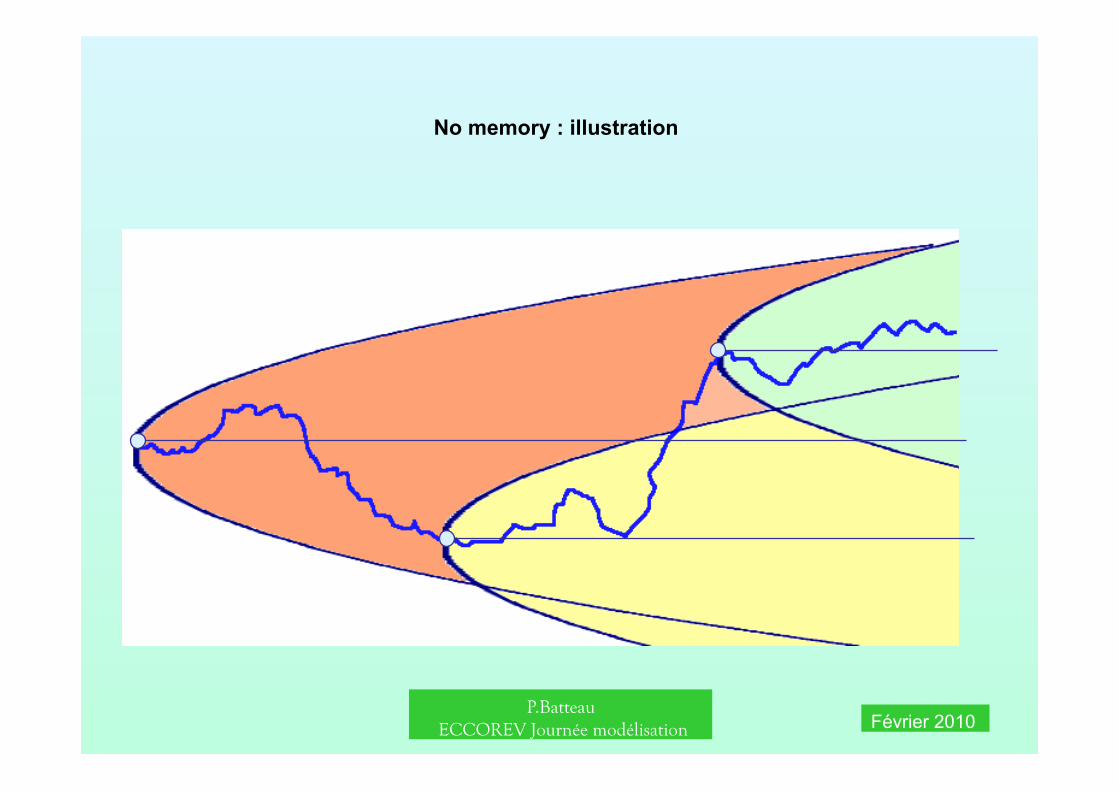

- 1) Markovian property : no memory : only the current value Bt at time t determines the distribution of the future values. Past trajectories are irrelevant. (captures the idea of “market efficiency” in Finance)

- Independent increment (previous slides)

- The increment over any finite interval follows a Normal (Gaussian) distribution with a variance proportional to the length of the interval (i.e. standard deviation increases as the square root of time)

Unit Wiener process : The variance per unit of time is ONE.

When discritized (t=1,2,…j,…), the series of Bt is not stationary but the increments are.

P.Batteau ECCOREV Journée modélisation Février 2010

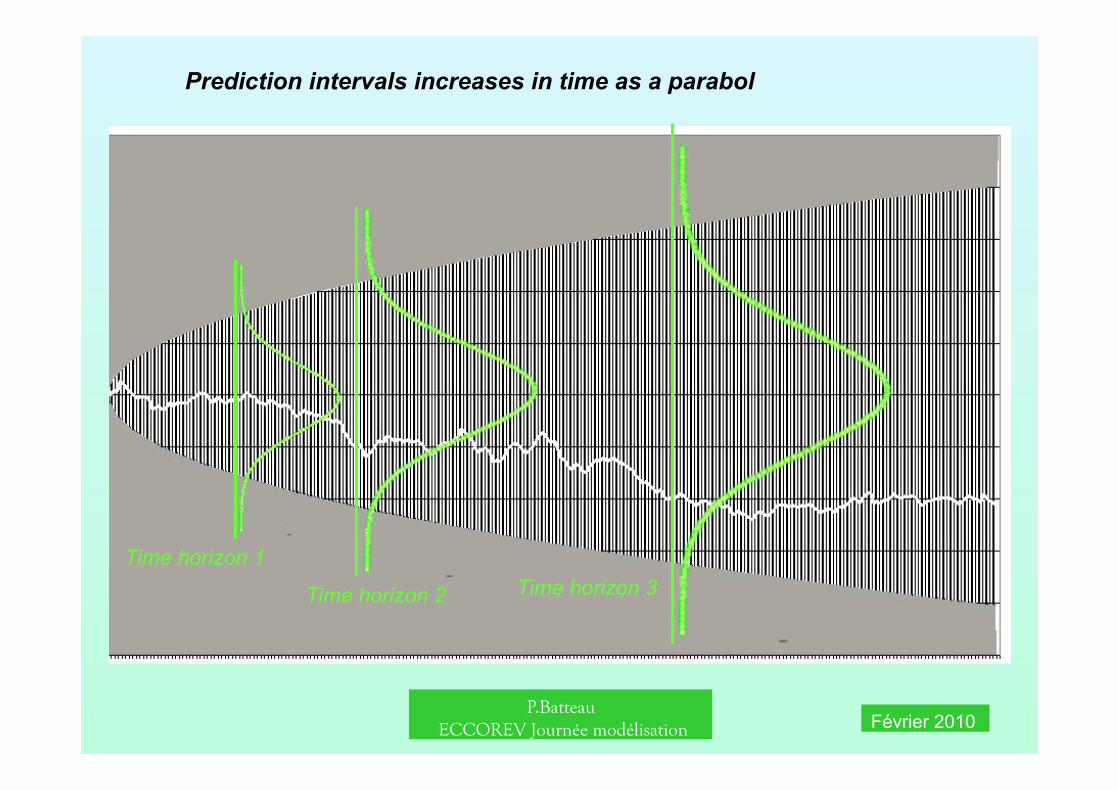

Time horizon 1

Time horizon 2 Time horizon 3

Prediction intervals increases in time as a parabol

P.Batteau ECCOREV Journée modélisation Février 2010

No memory : illustration

P.Batteau ECCOREV Journée modélisation Février 2010

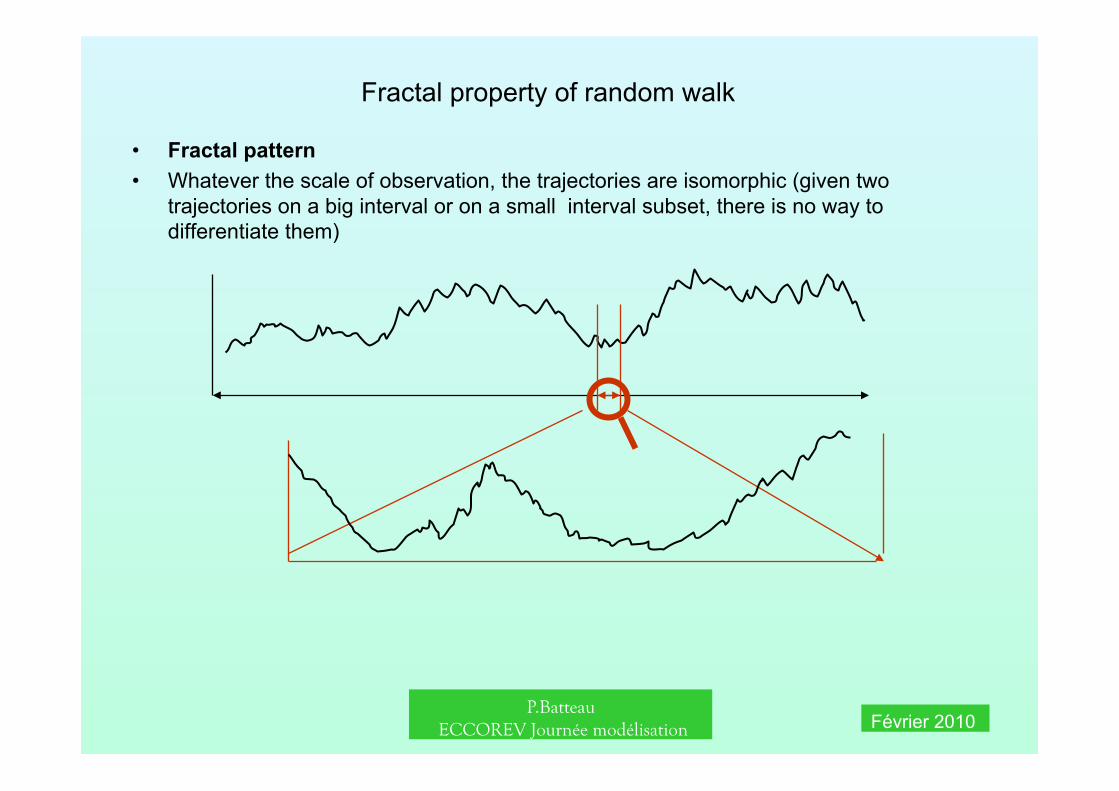

Fractal property of random walk

• Fractal pattern • Whatever the scale of observation, the trajectories are isomorphic (given two

trajectories on a big interval or on a small interval subset, there is no way to differentiate them)

P.Batteau ECCOREV Journée modélisation Février 2010

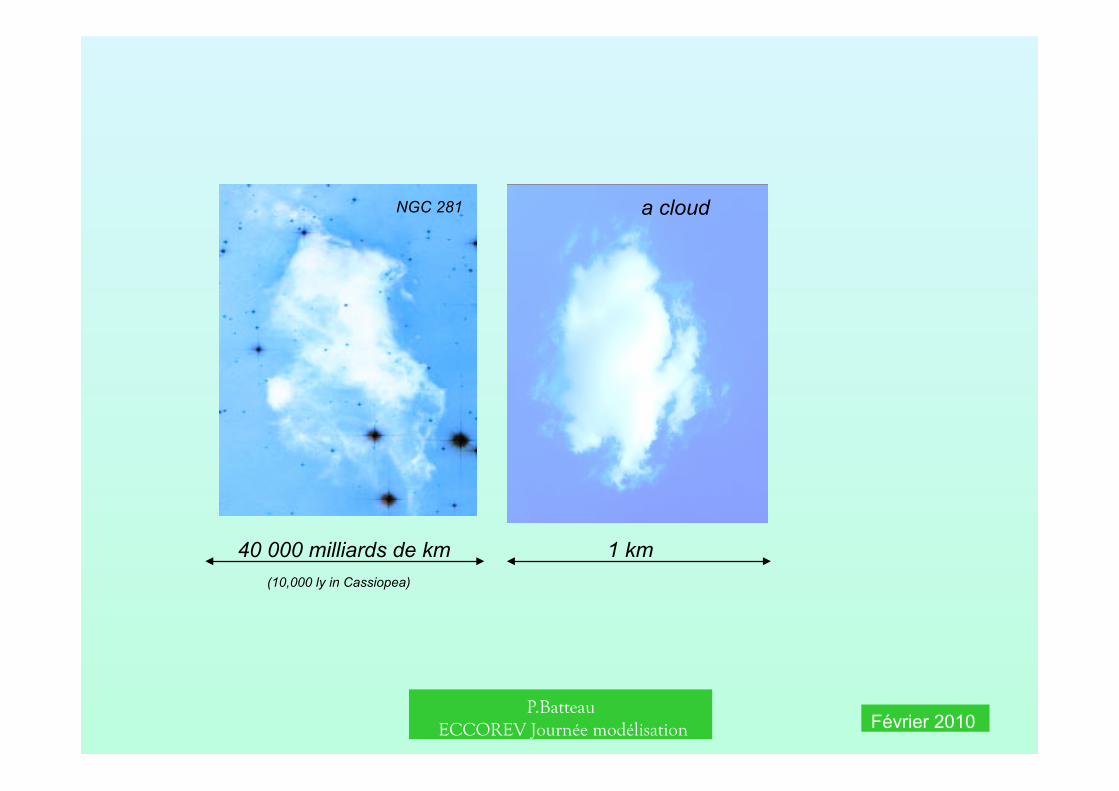

40 000 milliards de km 1 km

a cloud NGC 281

(10,000 ly in Cassiopea)

P.Batteau ECCOREV Journée modélisation Février 2010

Applications in Finance

P.Batteau ECCOREV Journée modélisation Février 2010

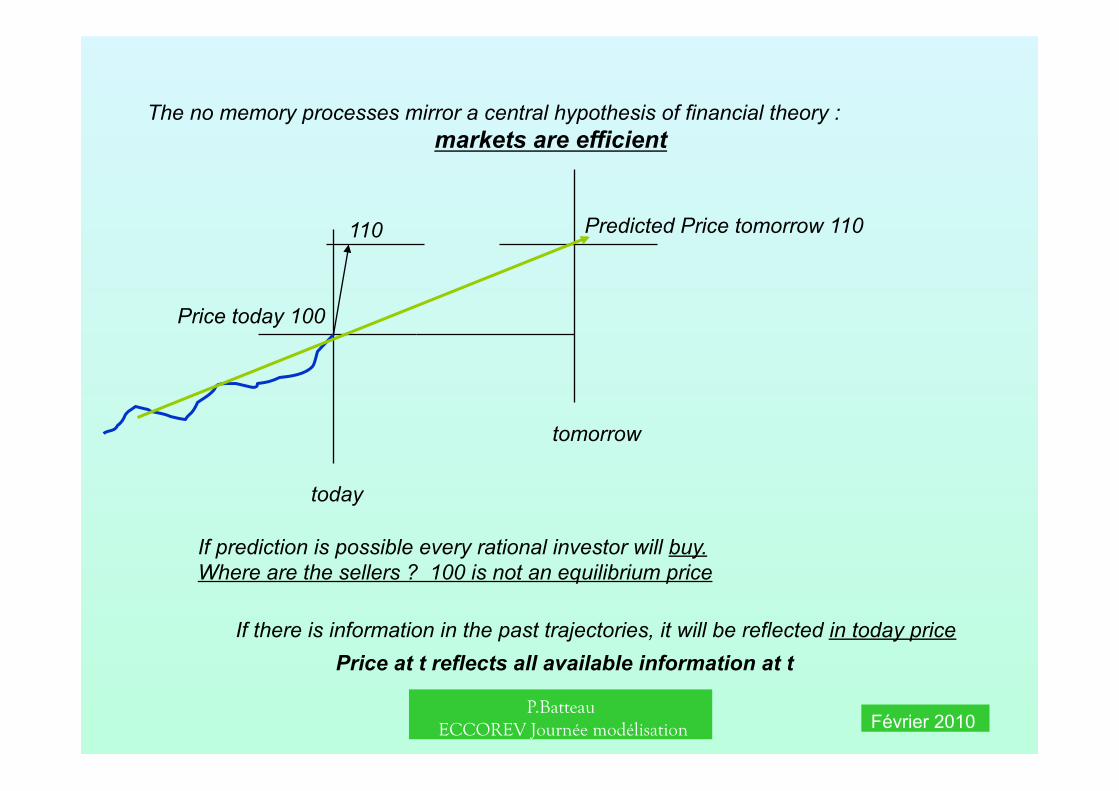

The no memory processes mirror a central hypothesis of financial theory : markets are efficient

today

Price today 100

tomorrow

Predicted Price tomorrow 110

If prediction is possible every rational investor will buy. Where are the sellers ? 100 is not an equilibrium price

110

If there is information in the past trajectories, it will be reflected in today price Price at t reflects all available information at t

P.Batteau ECCOREV Journée modélisation Février 2010

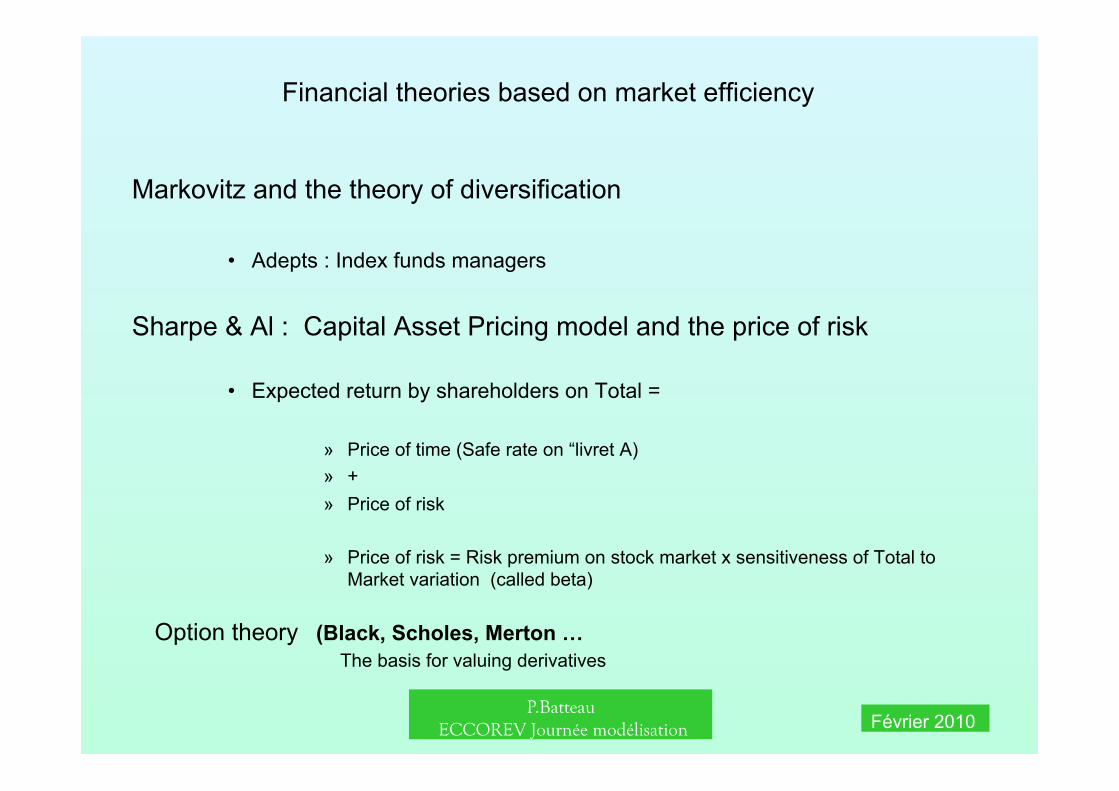

Financial theories based on market efficiency

Markovitz and the theory of diversification

• Adepts : Index funds managers

Sharpe & Al : Capital Asset Pricing model and the price of risk

• Expected return by shareholders on Total =

» Price of time (Safe rate on “livret A) » + » Price of risk

» Price of risk = Risk premium on stock market x sensitiveness of Total to Market variation (called beta)

Option theory (Black, Scholes, Merton … The basis for valuing derivatives

P.Batteau ECCOREV Journée modélisation Février 2010

The mysteries of derivatives

• Every day several hundred billions dollars of derivative contratcs are exchanged on the financial markets and among banks

P.Batteau ECCOREV Journée modélisation Février 2010

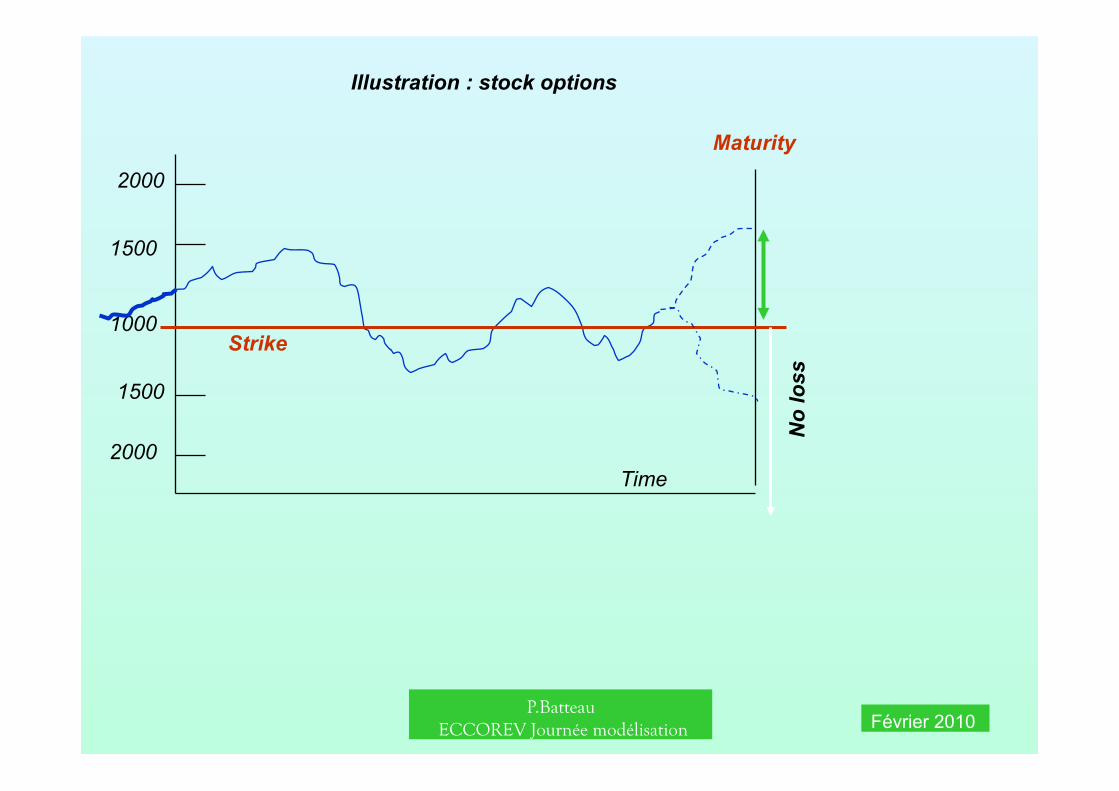

Illustration : stock options

Time

1000

1500

2000

2000

1500

Strike

Maturity

No

loss

P.Batteau ECCOREV Journée modélisation Février 2010

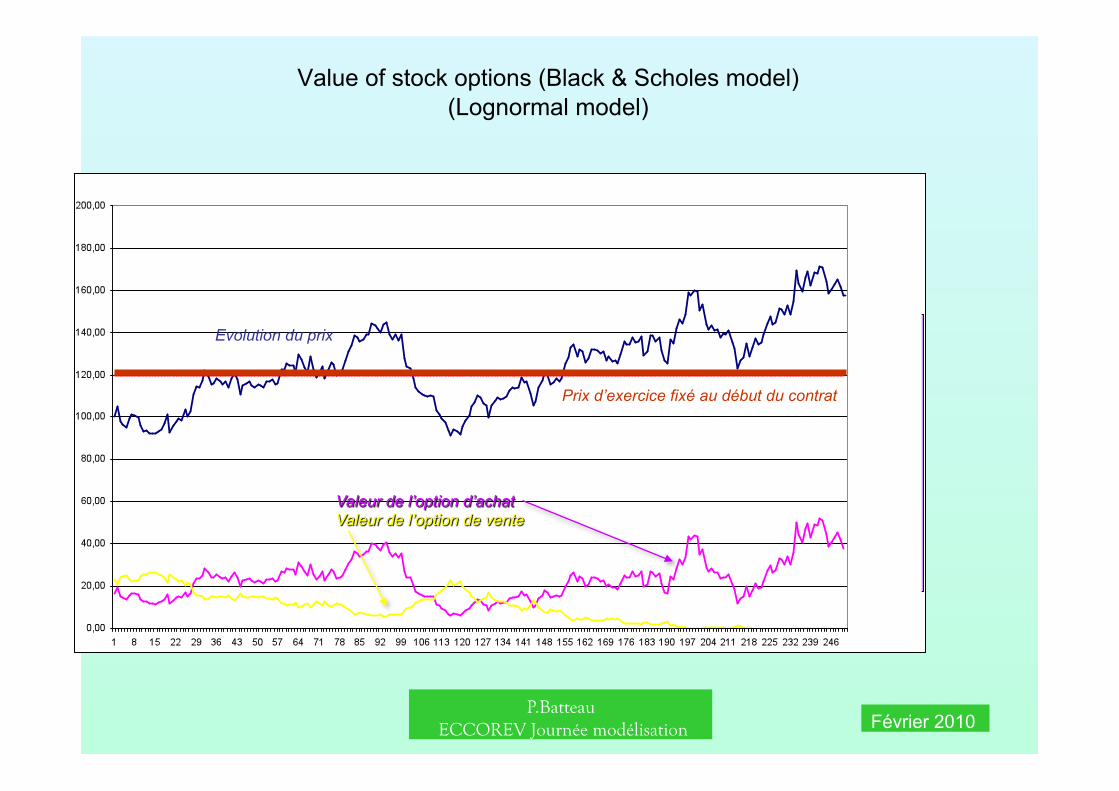

Value of stock options (Black & Scholes model) (Lognormal model)

Prix d’exercice fixé au début du contrat

Evolution du prix

P.Batteau ECCOREV Journée modélisation Février 2010

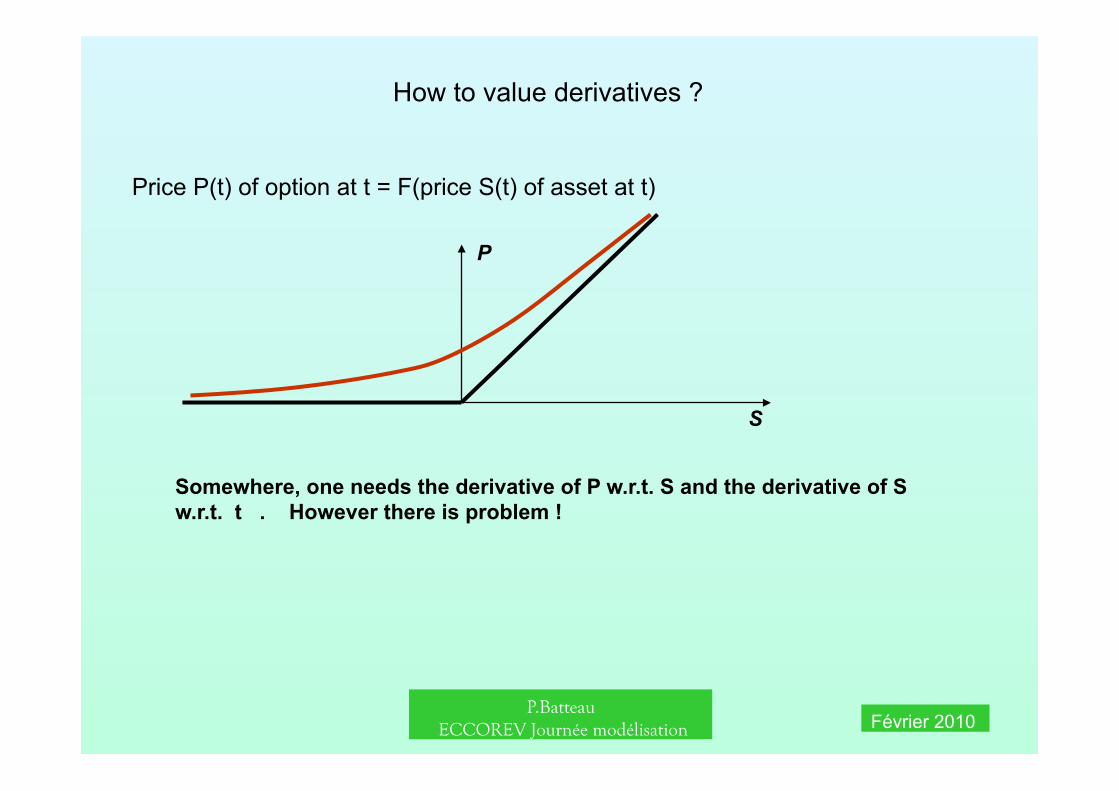

How to value derivatives ?

Price P(t) of option at t = F(price S(t) of asset at t)

S

P

Somewhere, one needs the derivative of P w.r.t. S and the derivative of S w.r.t. t . However there is problem !

P.Batteau ECCOREV Journée modélisation Février 2010

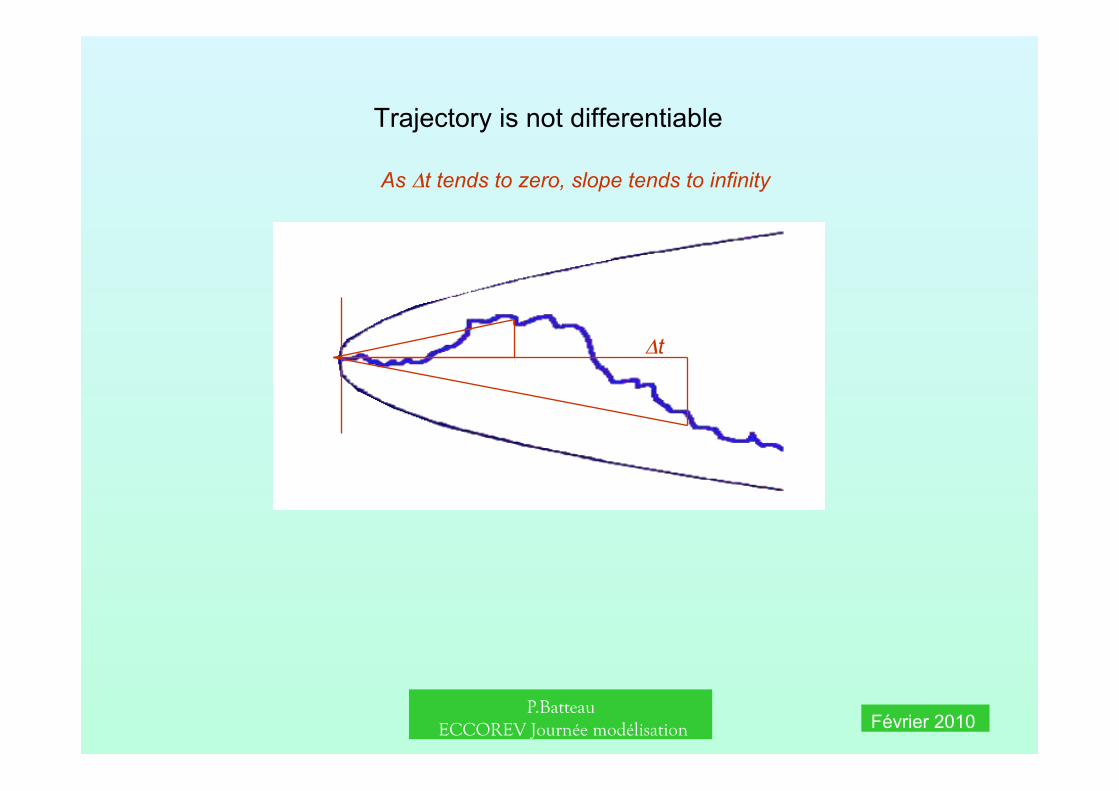

Trajectory is not differentiable

Δt

As Δt tends to zero, slope tends to infinity

P.Batteau ECCOREV Journée modélisation Février 2010

Stochastic differential equation

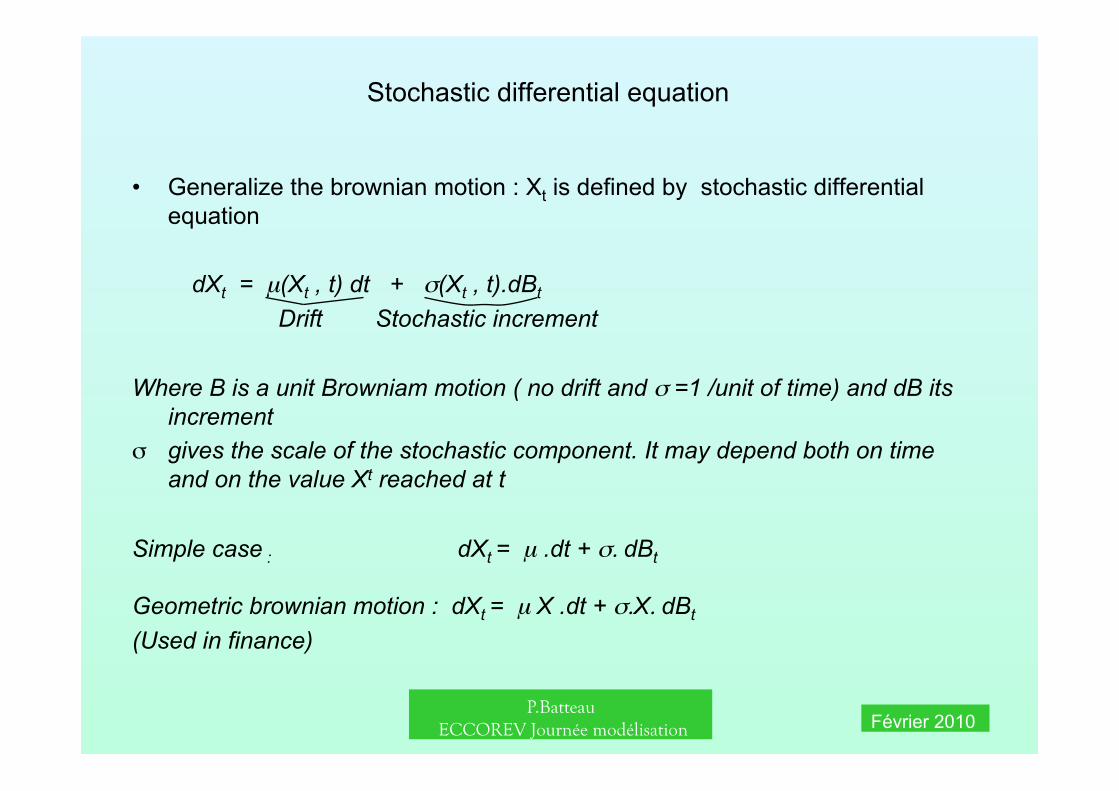

• Generalize the brownian motion : Xt is defined by stochastic differential equation

dXt = µ(Xt , t) dt + σ(Xt , t).dBt

Drift Stochastic increment

Where B is a unit Browniam motion ( no drift and σ =1 /unit of time) and dB its increment

σ gives the scale of the stochastic component. It may depend both on time and on the value Xt reached at t

Simple case : dXt = µ .dt + σ. dBt

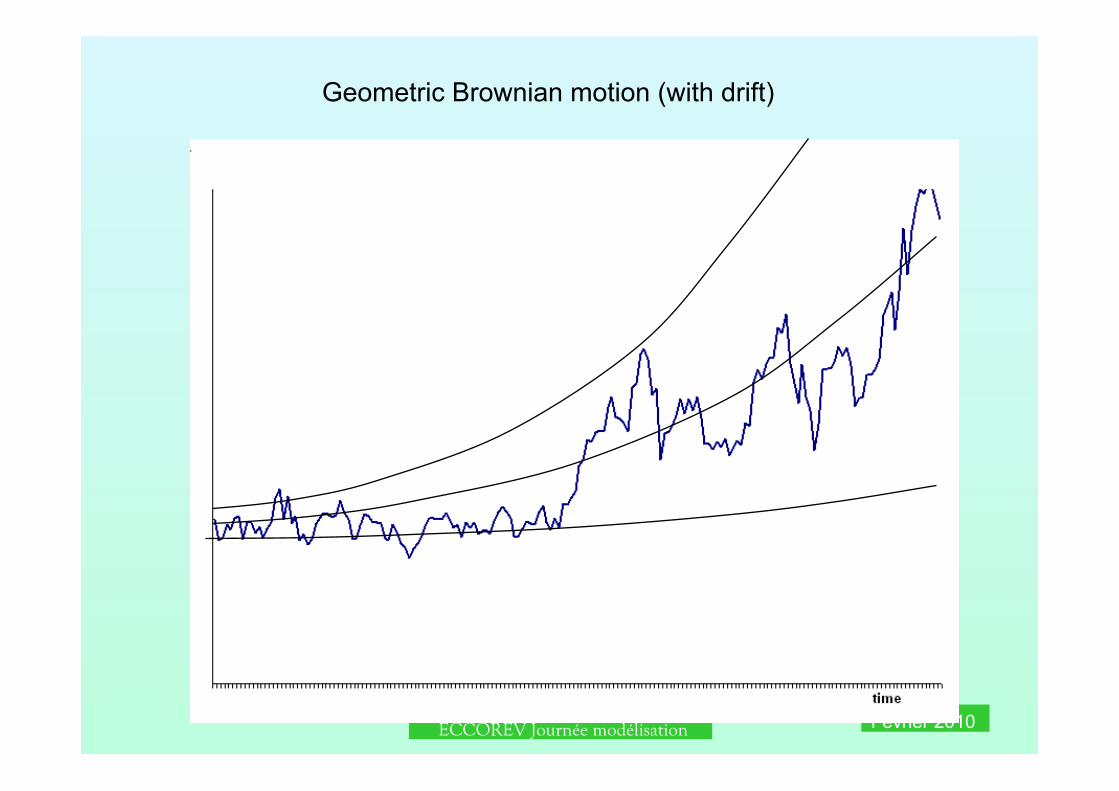

Geometric brownian motion : dXt = µ X .dt + σ.X. dBt

(Used in finance)

P.Batteau ECCOREV Journée modélisation Février 2010

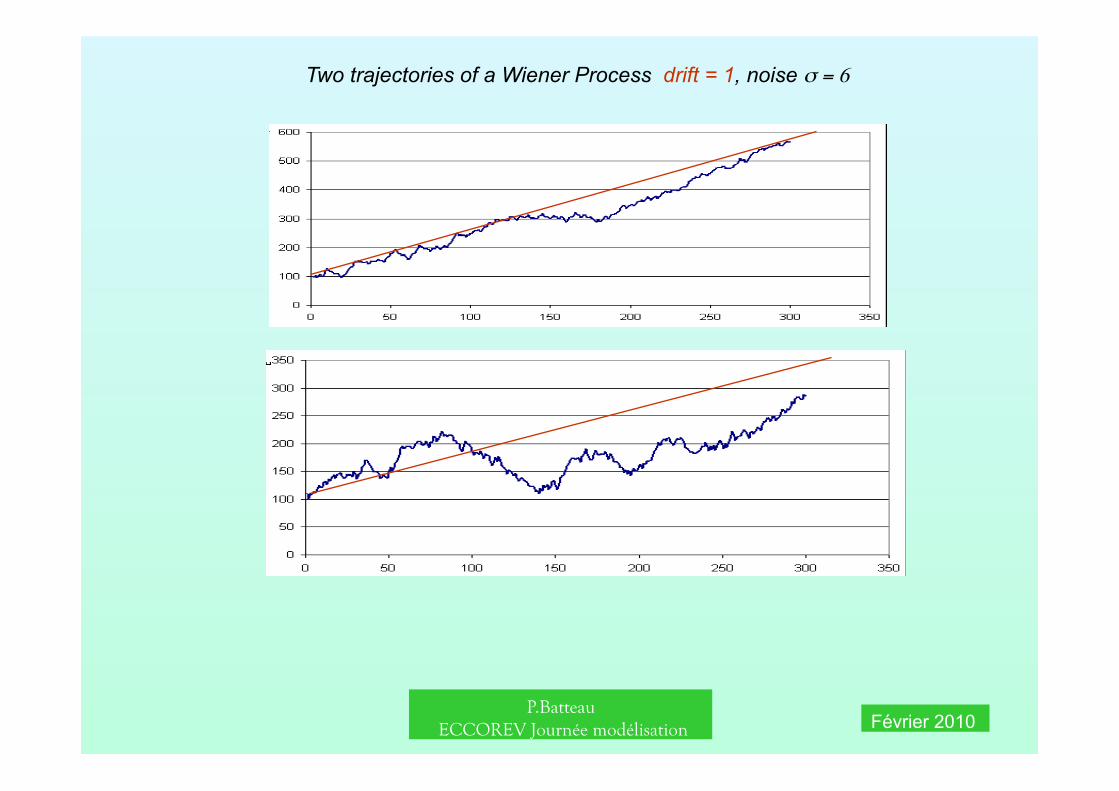

Two trajectories of a Wiener Process drift = 1, noise σ = 6

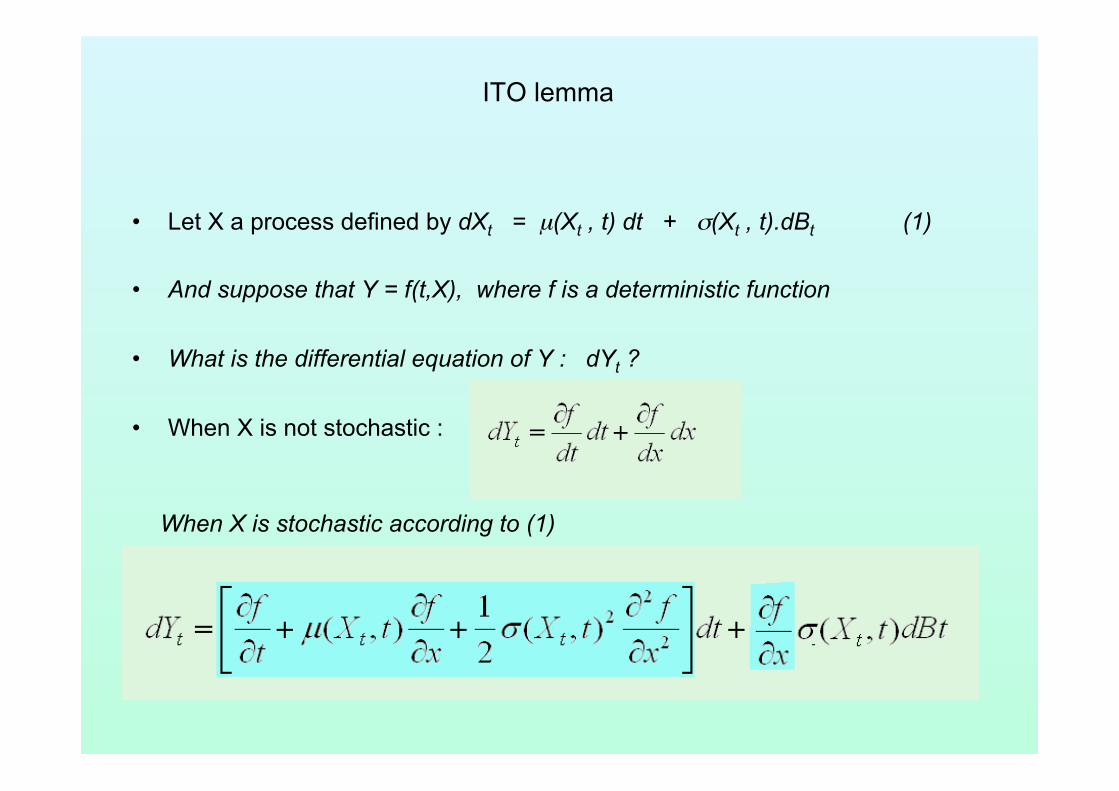

ITO lemma

• Let X a process defined by dXt = µ(Xt , t) dt + σ(Xt , t).dBt (1)

• And suppose that Y = f(t,X), where f is a deterministic function

• What is the differential equation of Y : dYt ?

• When X is not stochastic :

When X is stochastic according to (1)

P.Batteau ECCOREV Journée modélisation Février 2010

Geometric Brownian motion (with drift)

P.Batteau ECCOREV Journée modélisation Février 2010

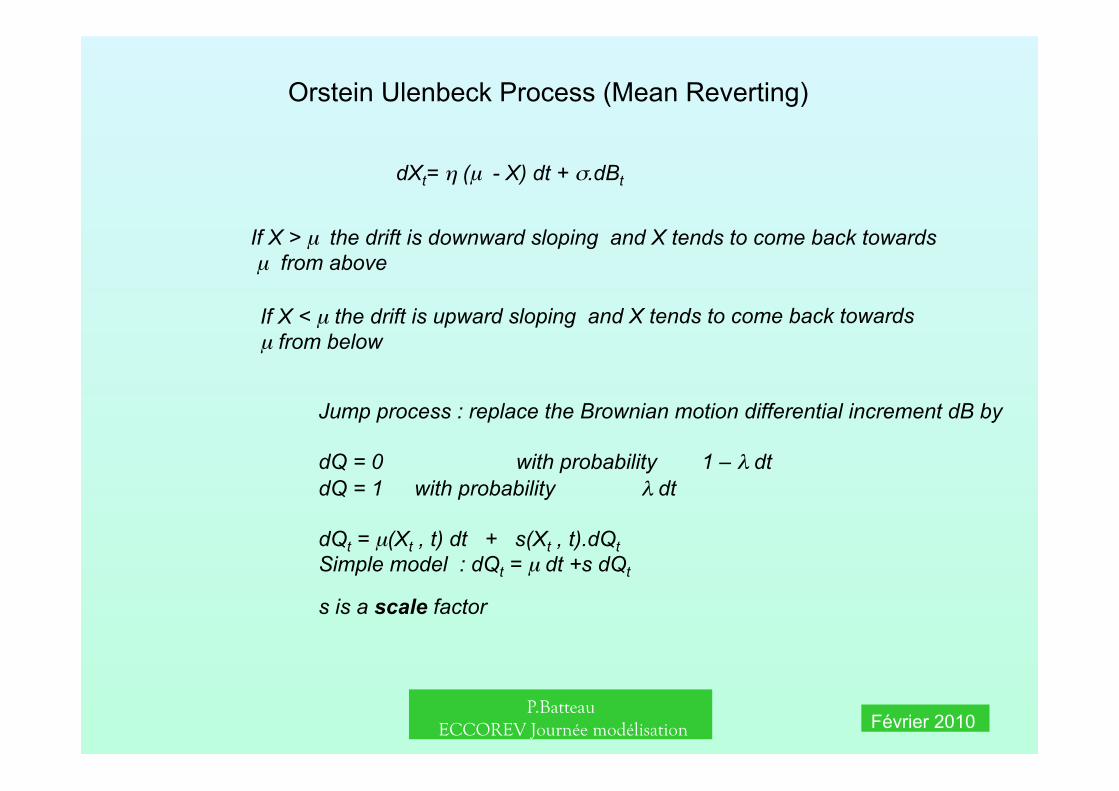

Orstein Ulenbeck Process (Mean Reverting)

dXt= η (µ - X) dt + σ.dBt

If X > µ the drift is downward sloping and X tends to come back towards µ from above

If X < µ the drift is upward sloping and X tends to come back towards µ from below

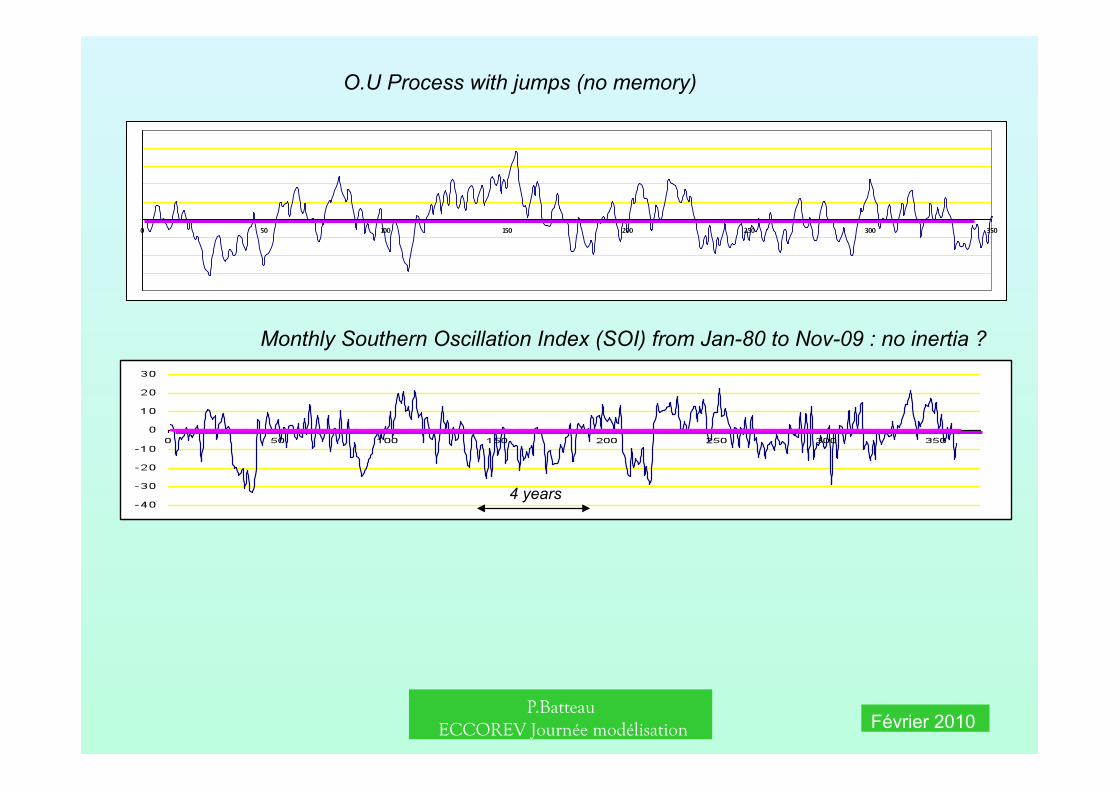

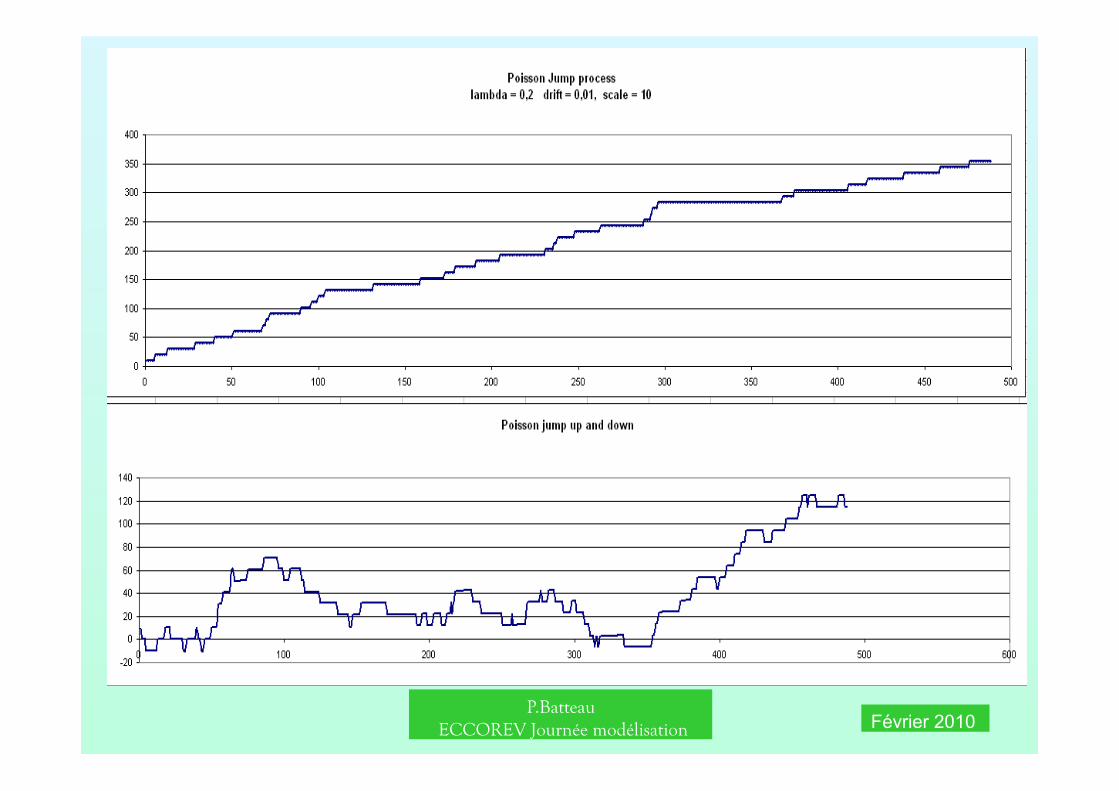

Jump process : replace the Brownian motion differential increment dB by

dQ = 0 with probability 1 – λ dt dQ = 1 with probability λ dt

dQt = µ(Xt , t) dt + s(Xt , t).dQt Simple model : dQt = µ dt +s dQt

s is a scale factor

P.Batteau ECCOREV Journée modélisation Février 2010

4 years

Monthly Southern Oscillation Index (SOI) from Jan-80 to Nov-09 : no inertia ?

O.U Process with jumps (no memory)

P.Batteau ECCOREV Journée modélisation Février 2010

P.Batteau ECCOREV Journée modélisation Février 2010

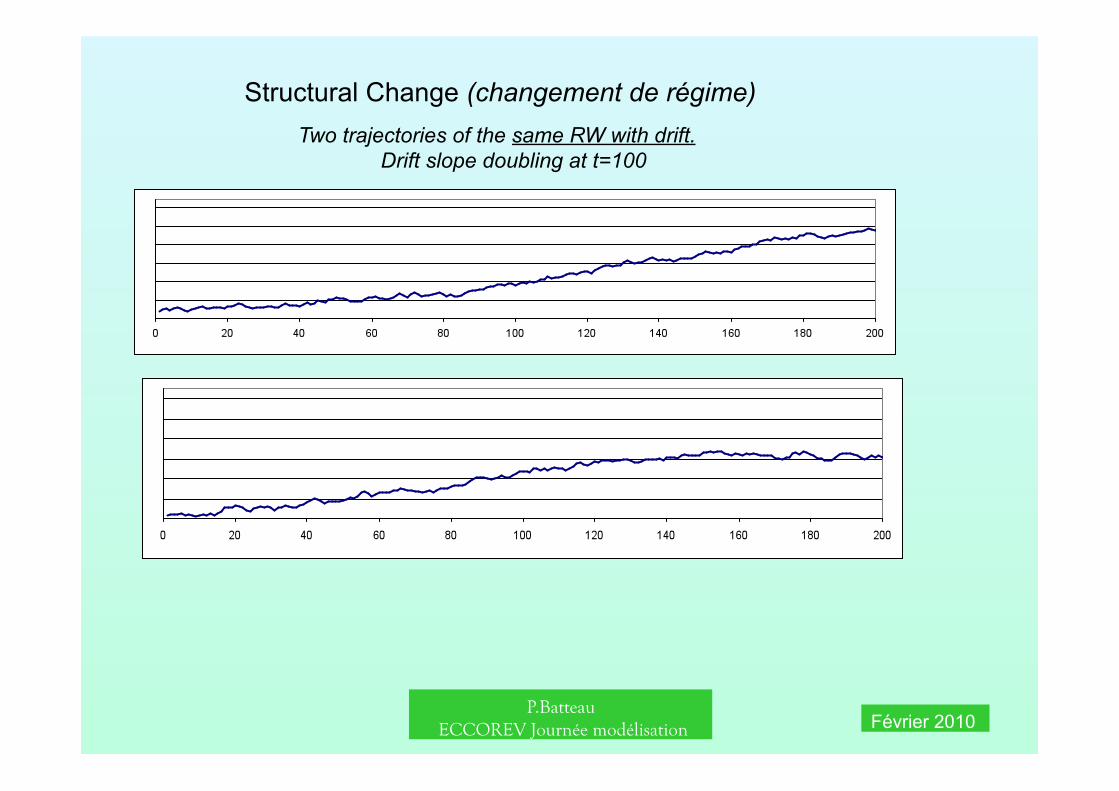

Structural Change (changement de régime) Two trajectories of the same RW with drift. Drift slope doubling at t=100

P.Batteau ECCOREV Journée modélisation Février 2010

,

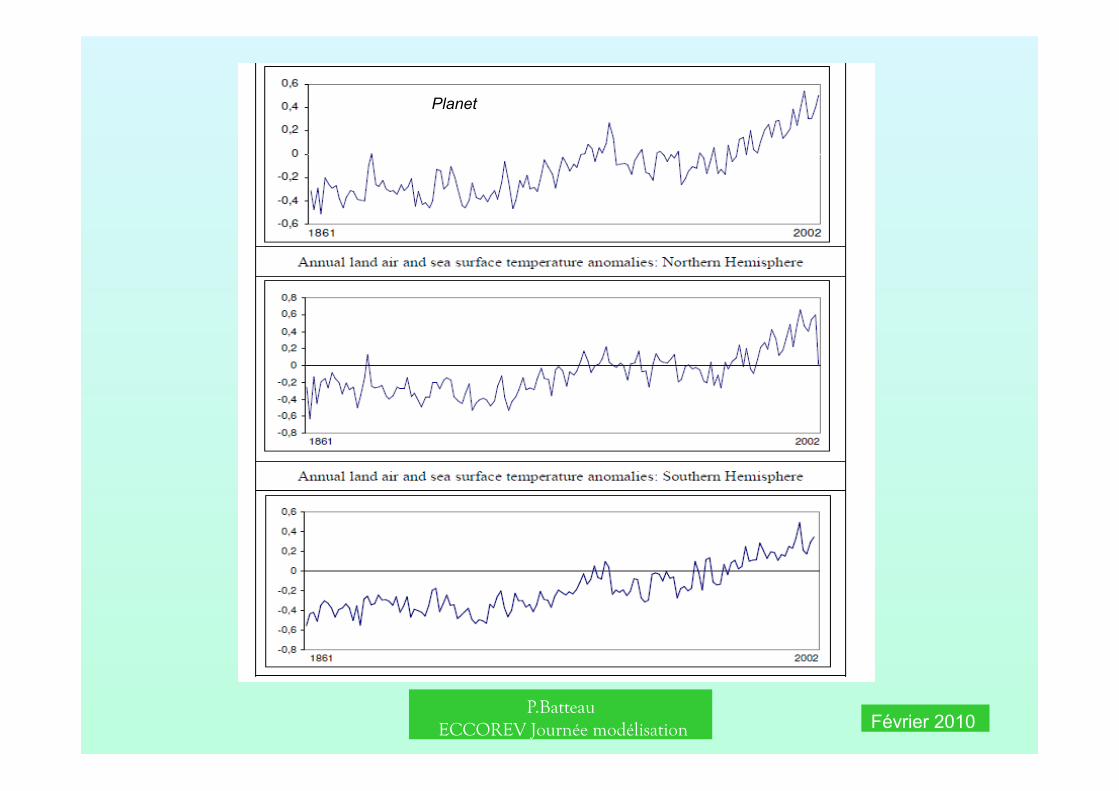

This paper deals with the modelling of the global and northern and southern hemispheric anomaly temperature time series using a novel technique based on segmented trends and fractional integration. We use a procedure that permits us to estimate linear time trends and orders of integration at various subsamples, where the periods for the changing trends are endogenously determined by the model. Moreover, we use a nonparametric approach (Bloomfield, 1973) for modelling the I(0) deviation term. The results show that the three series (global, northern and southern temperatures) can be well described in terms of fractional integration with the orders of integration around 0.5 in the three cases. The coefficients associated to the time trends are statistically significant in all subsamples for the three series, especially during the final part of the sample, giving then some support to the global warming theories.

!

P.Batteau ECCOREV Journée modélisation Février 2010

Planet

P.Batteau ECCOREV Journée modélisation Février 2010

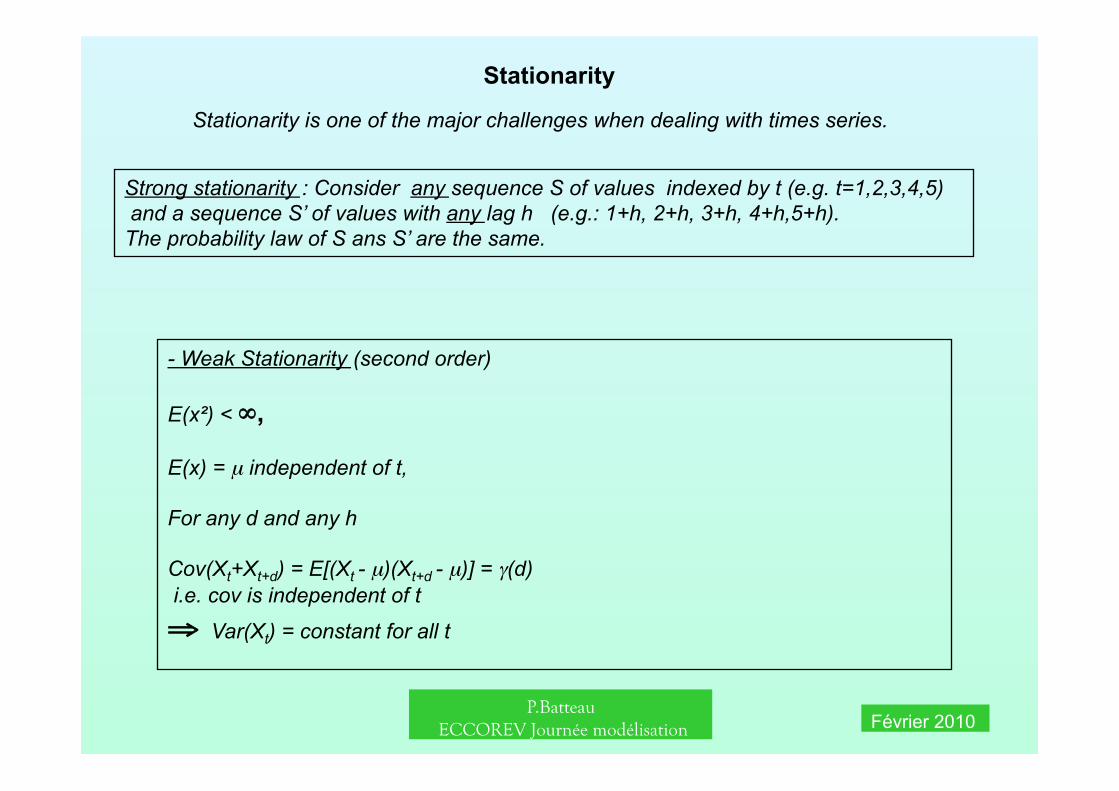

Strong stationarity : Consider any sequence S of values indexed by t (e.g. t=1,2,3,4,5) and a sequence S’ of values with any lag h (e.g.: 1+h, 2+h, 3+h, 4+h,5+h). The probability law of S ans S’ are the same.

Stationarity

- Weak Stationarity (second order)

E(x²) < ∞,

E(x) = µ independent of t,

For any d and any h

Cov(Xt+Xt+d) = E[(Xt - µ)(Xt+d - µ)] = γ(d) i.e. cov is independent of t

⇒ Var(Xt) = constant for all t

Stationarity is one of the major challenges when dealing with times series.

P.Batteau ECCOREV Journée modélisation Février 2010

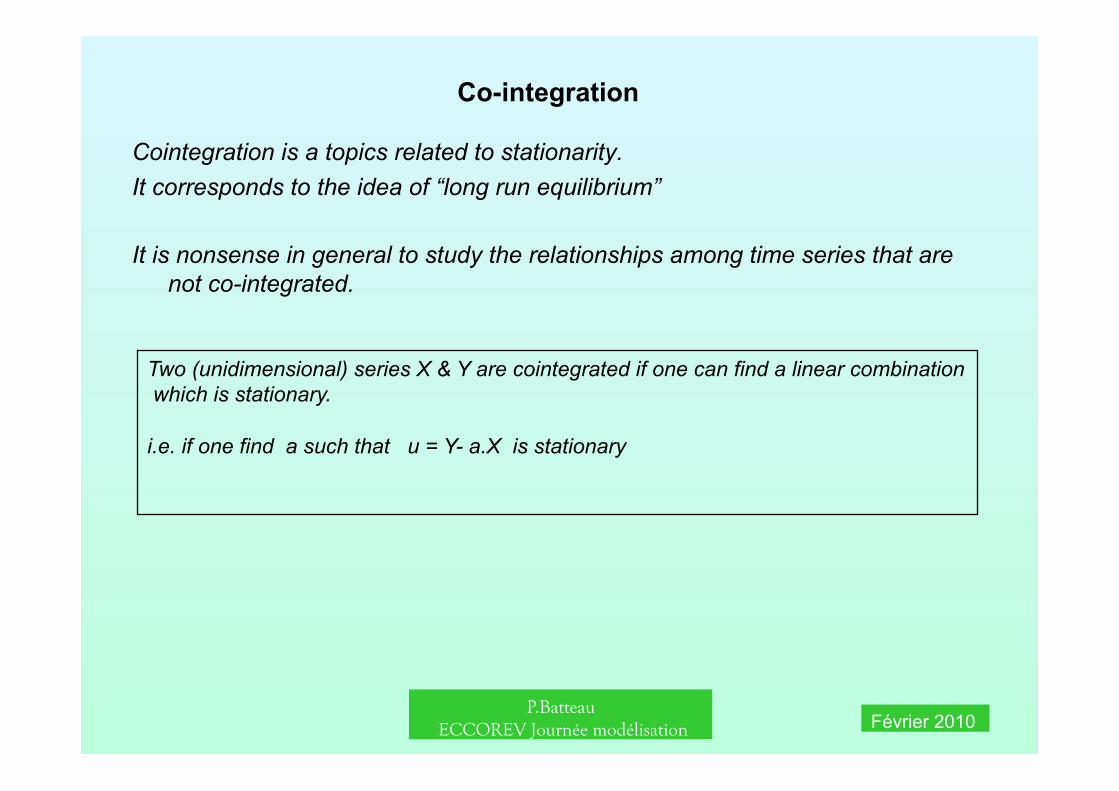

Co-integration

Cointegration is a topics related to stationarity. It corresponds to the idea of “long run equilibrium”

It is nonsense in general to study the relationships among time series that are not co-integrated.

Two (unidimensional) series X & Y are cointegrated if one can find a linear combination which is stationary.

i.e. if one find a such that u = Y- a.X is stationary

P.Batteau ECCOREV Journée modélisation Février 2010

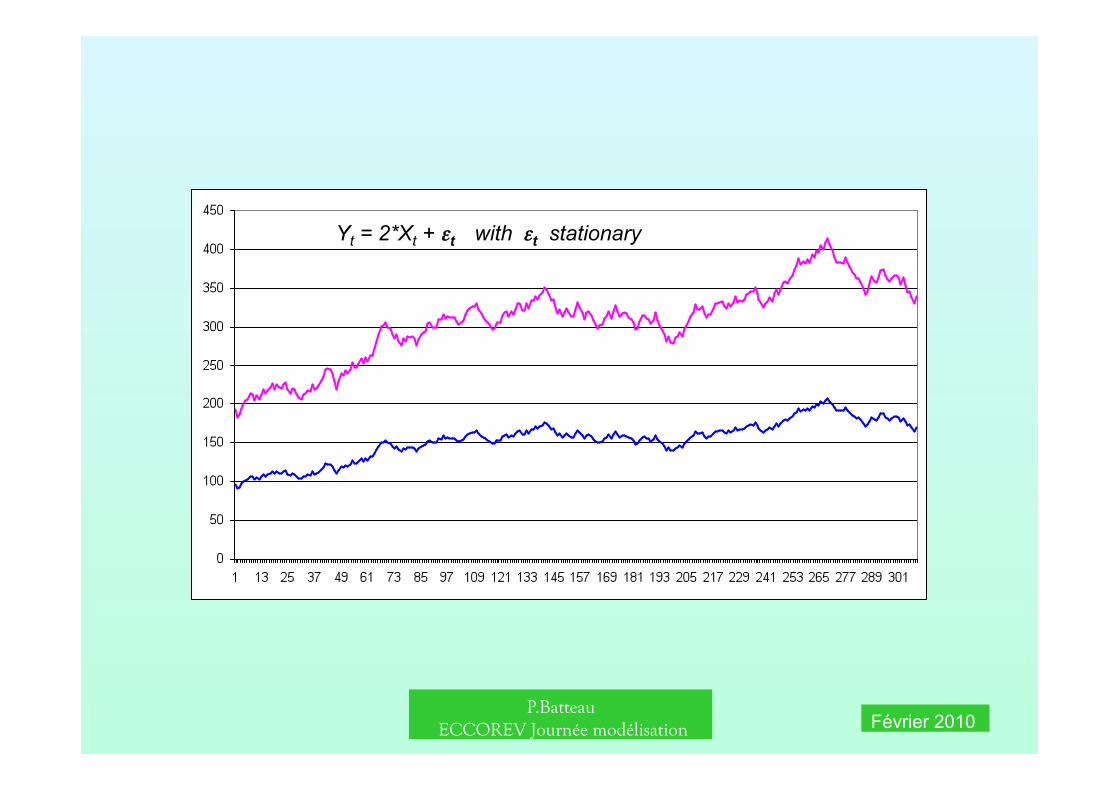

Yt = 2*Xt + εt with εt stationary

P.Batteau ECCOREV Journée modélisation Février 2010

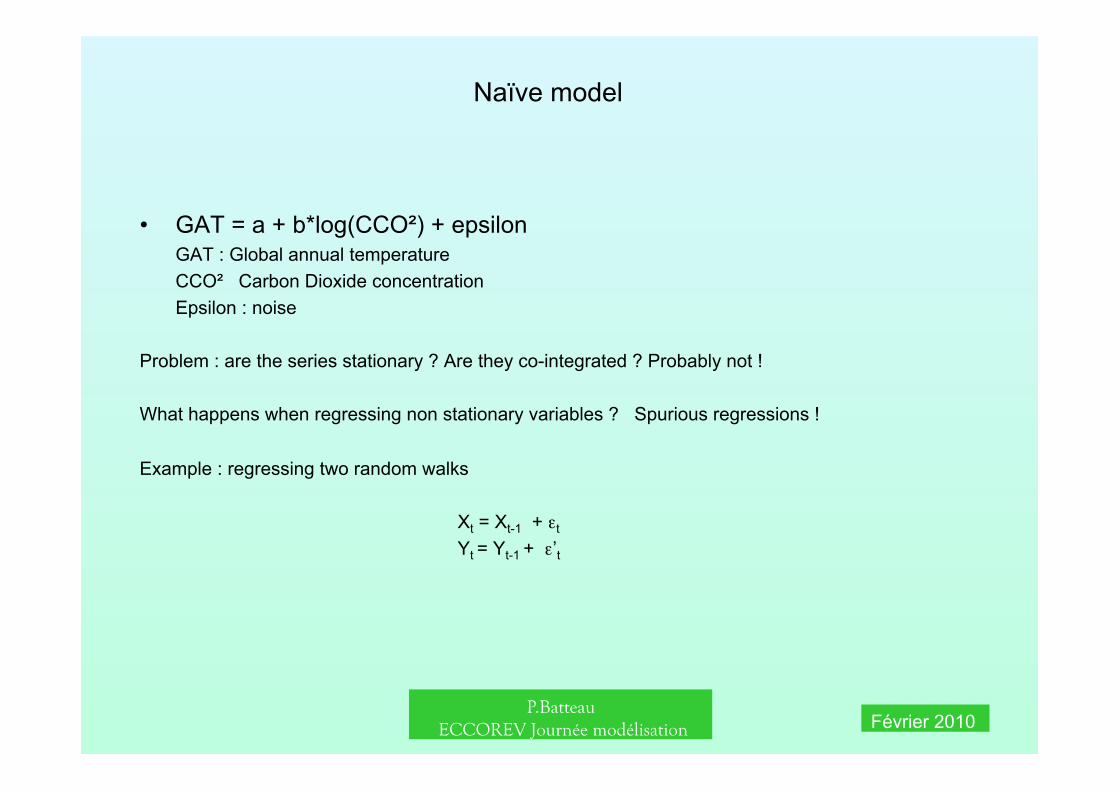

Naïve model

• GAT = a + b*log(CCO²) + epsilon GAT : Global annual temperature CCO² Carbon Dioxide concentration Epsilon : noise

Problem : are the series stationary ? Are they co-integrated ? Probably not !

What happens when regressing non stationary variables ? Spurious regressions !

Example : regressing two random walks

Xt = Xt-1 + εt

Yt = Yt-1 + ε’t

P.Batteau ECCOREV Journée modélisation Février 2010

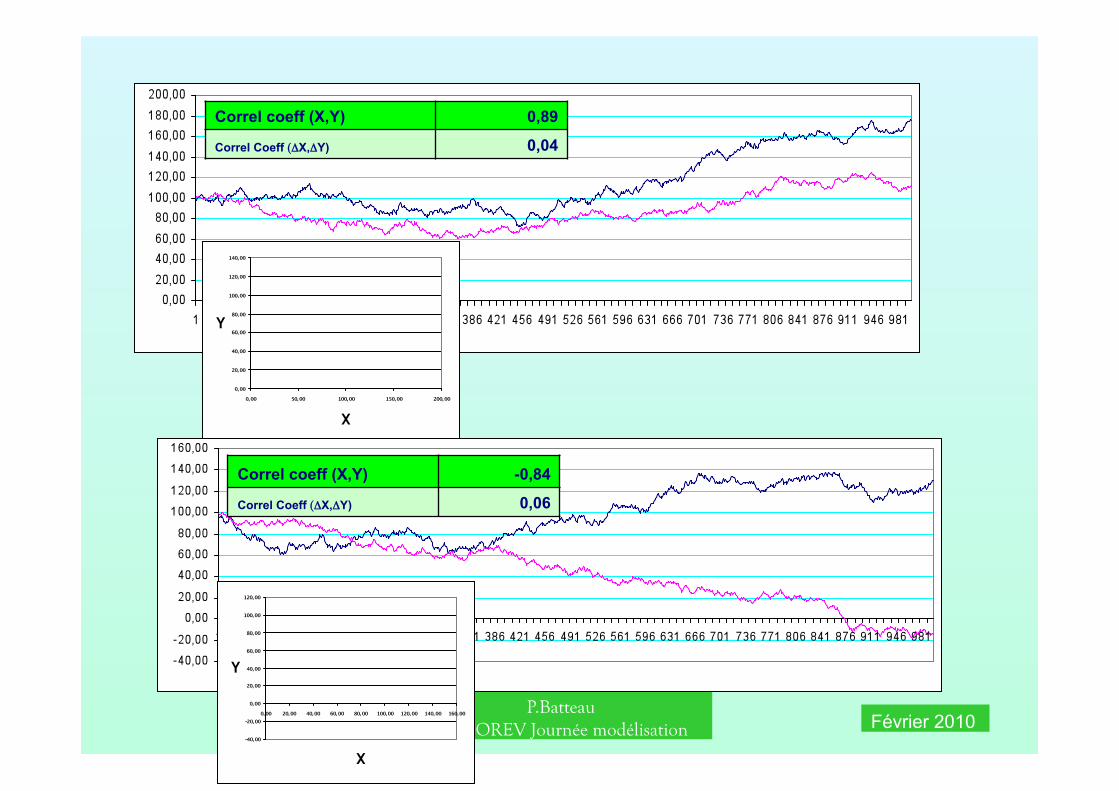

Correl coeff (X,Y) 0,89

Correl Coeff (ΔX,ΔY) 0,04

Correl coeff (X,Y) -0,84

Correl Coeff (ΔX,ΔY) 0,06

P.Batteau ECCOREV Journée modélisation Février 2010

Extrem risks

A story of fat tails

P.Batteau ECCOREV Journée modélisation Février 2010

P.Batteau ECCOREV Journée modélisation Février 2010

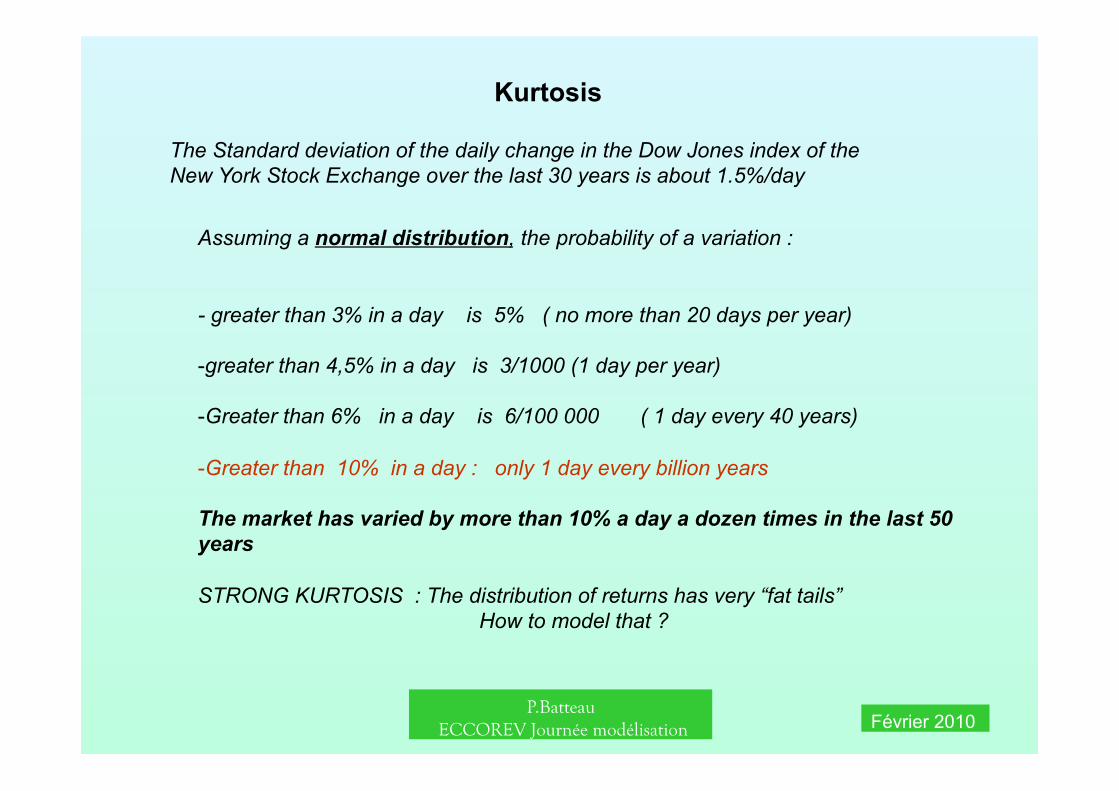

Kurtosis

The Standard deviation of the daily change in the Dow Jones index of the New York Stock Exchange over the last 30 years is about 1.5%/day

Assuming a normal distribution, the probability of a variation :

- greater than 3% in a day is 5% ( no more than 20 days per year)

- greater than 4,5% in a day is 3/1000 (1 day per year)

- Greater than 6% in a day is 6/100 000 ( 1 day every 40 years)

- Greater than 10% in a day : only 1 day every billion years

The market has varied by more than 10% a day a dozen times in the last 50 years

STRONG KURTOSIS : The distribution of returns has very “fat tails” How to model that ?

P.Batteau ECCOREV Journée modélisation Février 2010

Unstable volatility

Volatility is assumed constant over the time horizon in many applications in finance as well as other fields. Early versions of the models for valuing The financial instruments called “derivatives”, were based on the assumption of constant volatility. There are many reasons however to believe that volatility is unstable. Which models are suitable for that ?

1 - At each t volatility is explained by a set of exogenous variables

2 - ARCH, GARCH models

3 - Stochastic volatility models

P.Batteau ECCOREV Journée modélisation Février 2010

P.Batteau ECCOREV Journée modélisation Février 2010

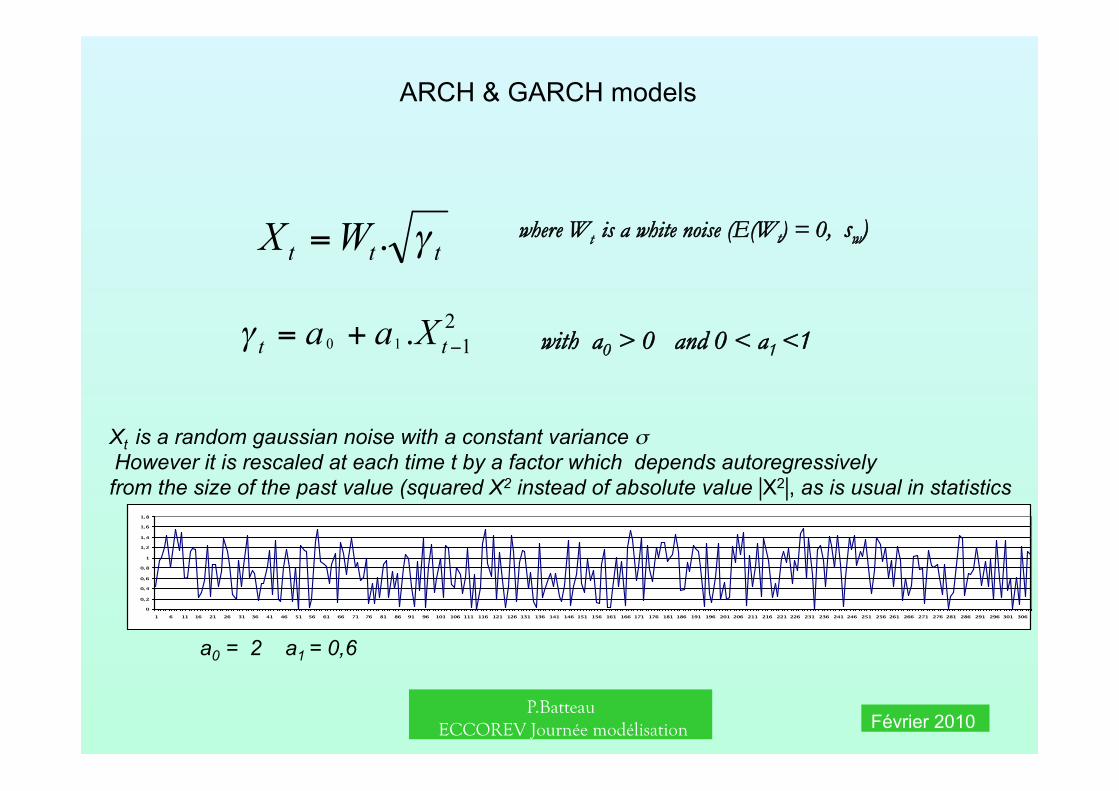

ARCH & GARCH models

where Wt is a white noise (E(Wt) = 0, sw)

with a0 > 0 and 0 < a1 <1

Xt is a random gaussian noise with a constant variance σ However it is rescaled at each time t by a factor which depends autoregressively from the size of the past value (squared X2 instead of absolute value |X2|, as is usual in statistics

a0 = 2 a1 = 0,6

P.Batteau ECCOREV Journée modélisation Février 2010

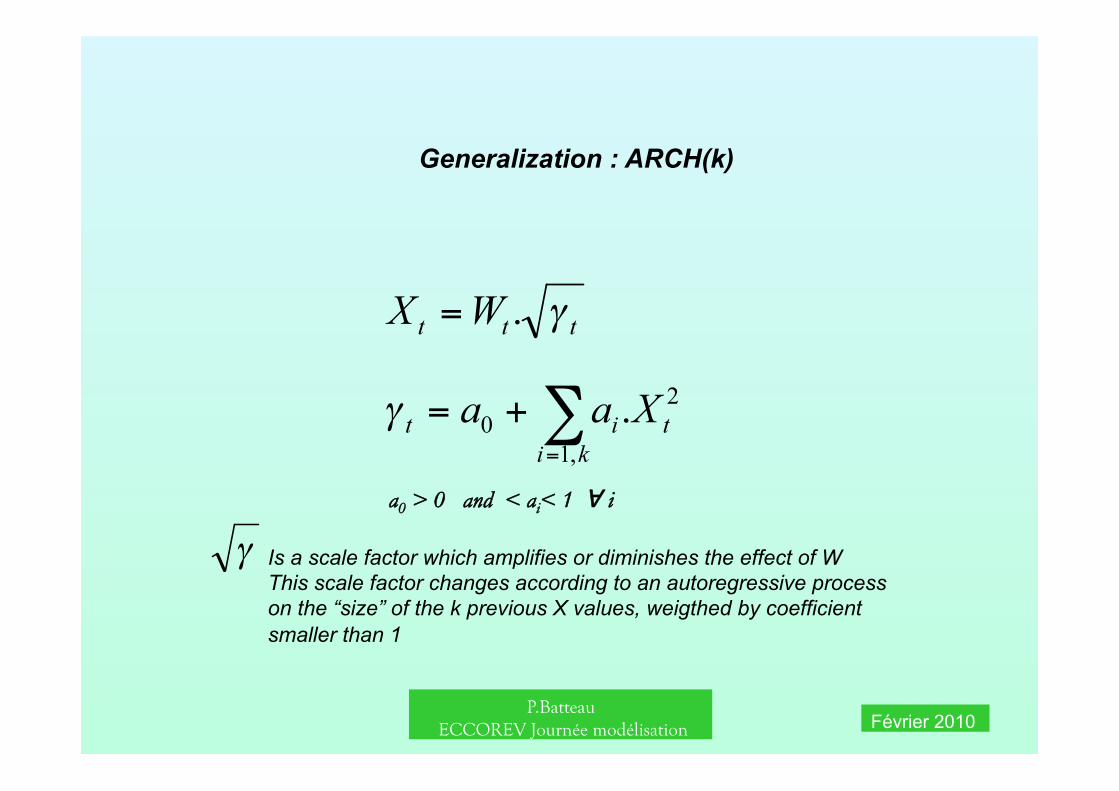

Generalization : ARCH(k)

Is a scale factor which amplifies or diminishes the effect of W This scale factor changes according to an autoregressive process on the “size” of the k previous X values, weigthed by coefficient smaller than 1

a0 > 0 and < ai< 1 ∀ i

P.Batteau ECCOREV Journée modélisation Février 2010

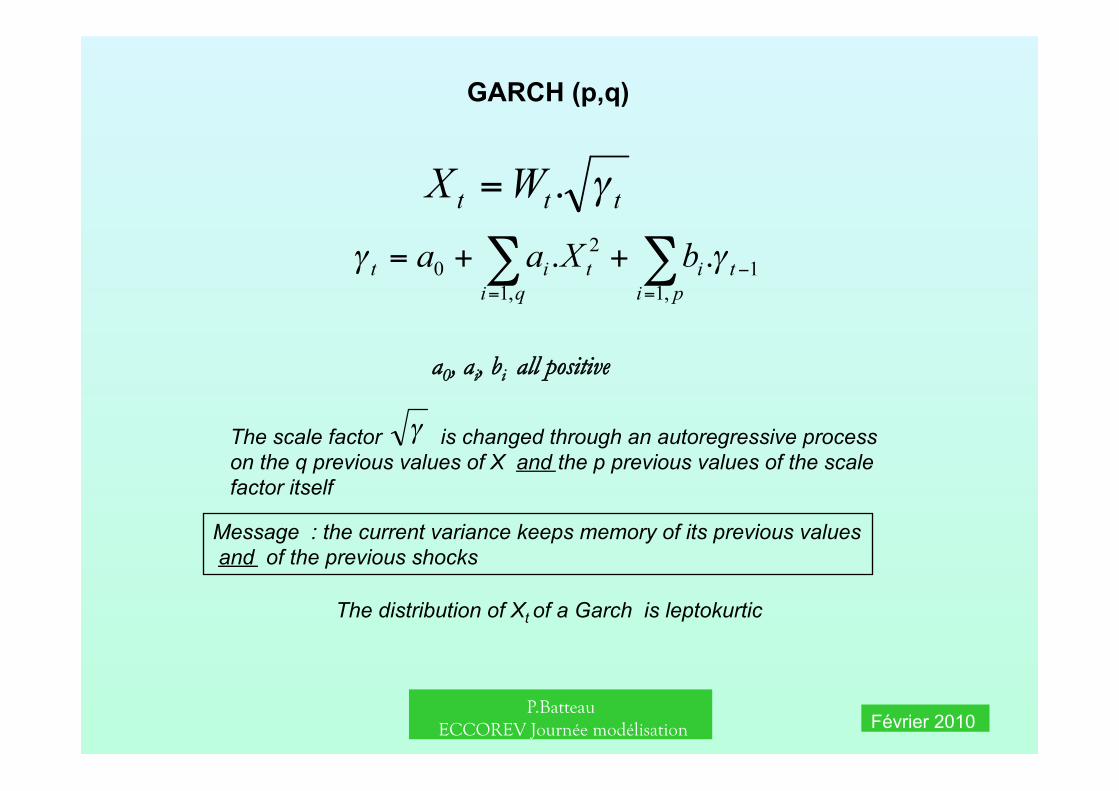

GARCH (p,q)

a0, ai, bi all positive

The scale factor is changed through an autoregressive process on the q previous values of X and the p previous values of the scale factor itself

Message : the current variance keeps memory of its previous values and of the previous shocks

The distribution of Xt of a Garch is leptokurtic

P.Batteau ECCOREV Journée modélisation Février 2010

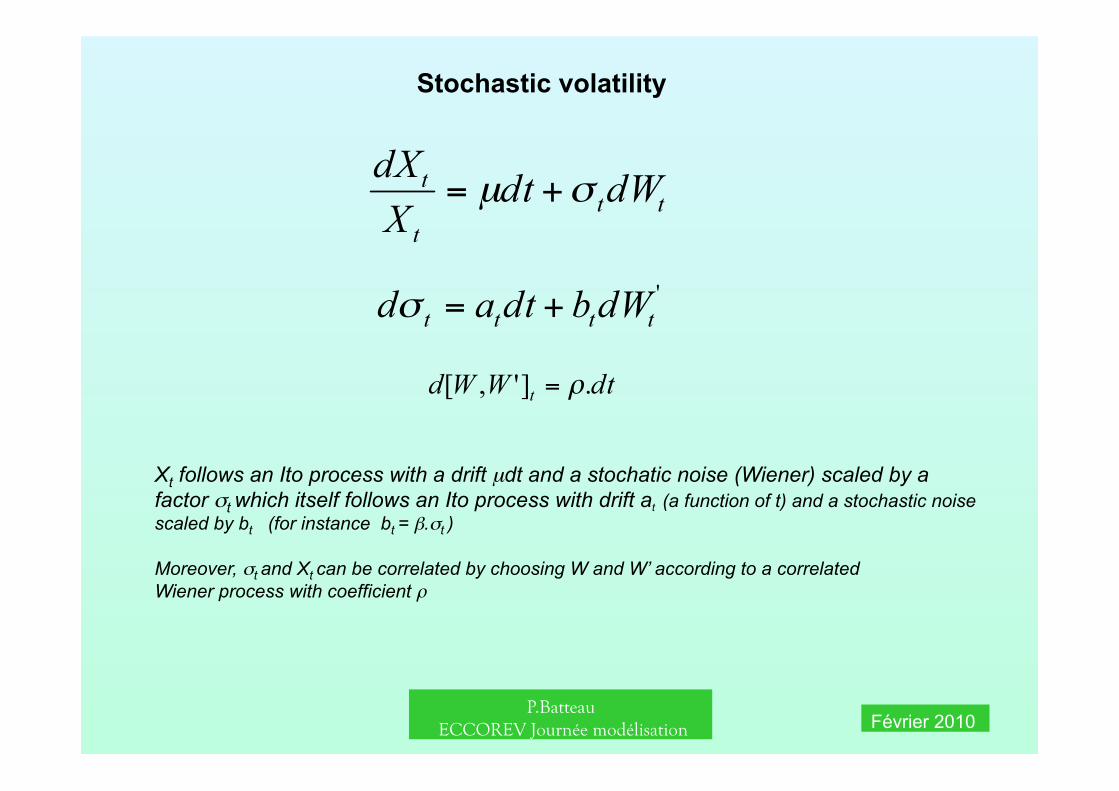

Stochastic volatility

Xt follows an Ito process with a drift µdt and a stochatic noise (Wiener) scaled by a factor σt which itself follows an Ito process with drift at (a function of t) and a stochastic noise scaled by bt (for instance bt = β.σt )

Moreover, σt and Xt can be correlated by choosing W and W’ according to a correlated Wiener process with coefficient ρ

P.Batteau ECCOREV Journée modélisation Février 2010

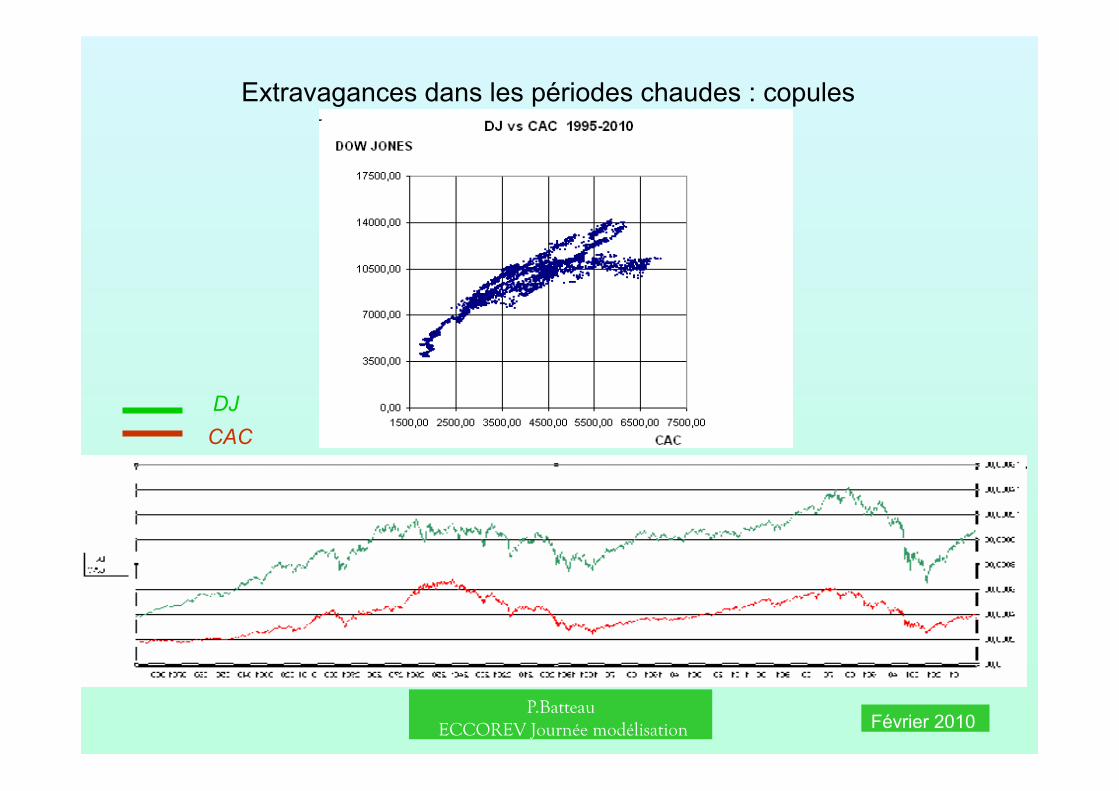

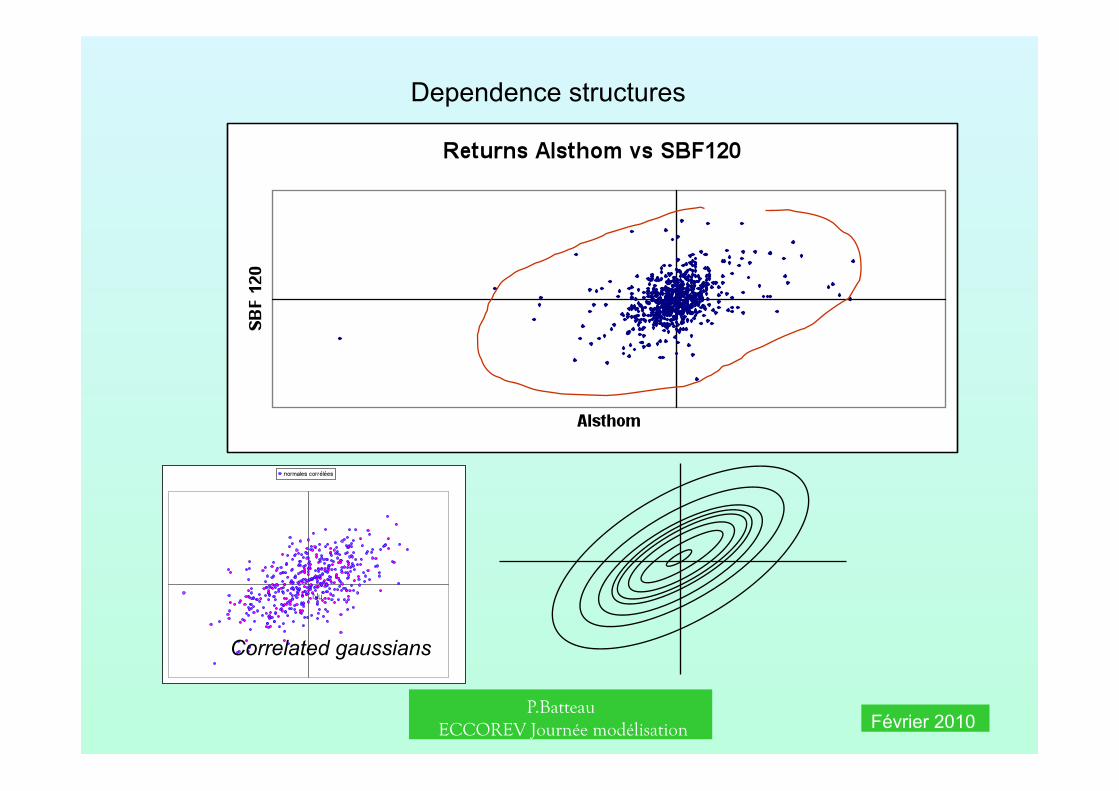

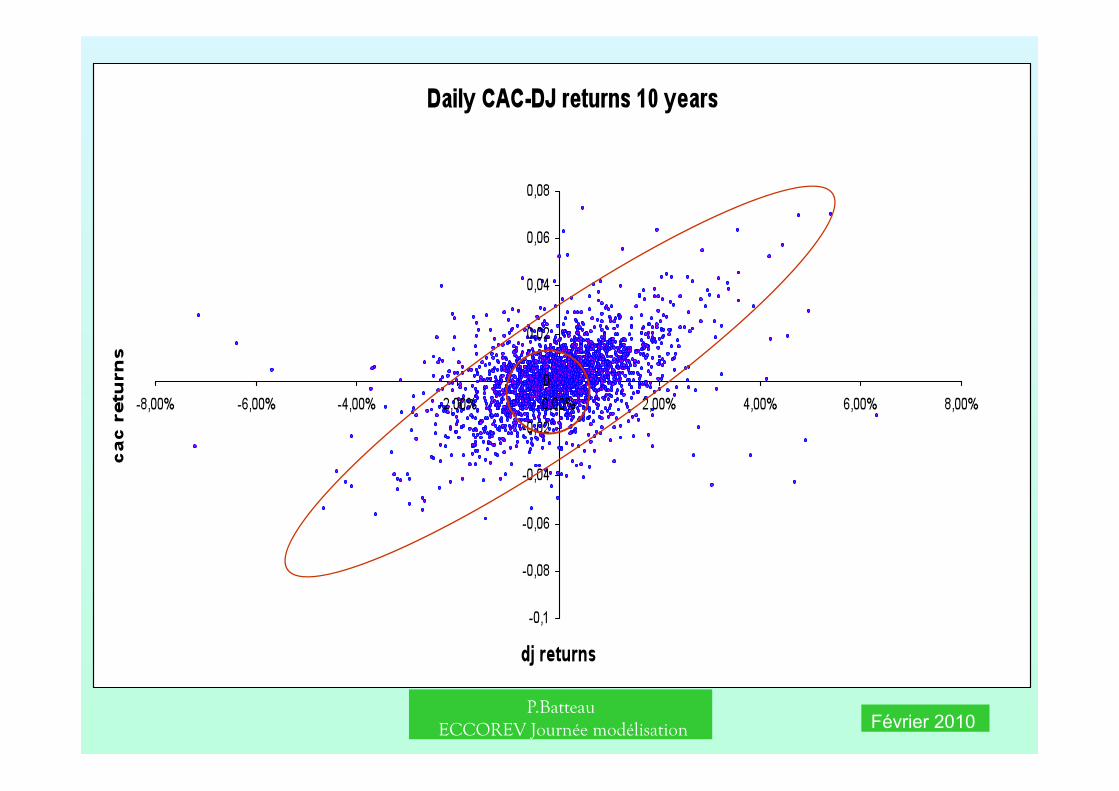

Extravagances dans les périodes chaudes : copules

DJ CAC

P.Batteau ECCOREV Journée modélisation Février 2010

Dependence structures

Correlated gaussians

P.Batteau ECCOREV Journée modélisation Février 2010

P.Batteau ECCOREV Journée modélisation Février 2010

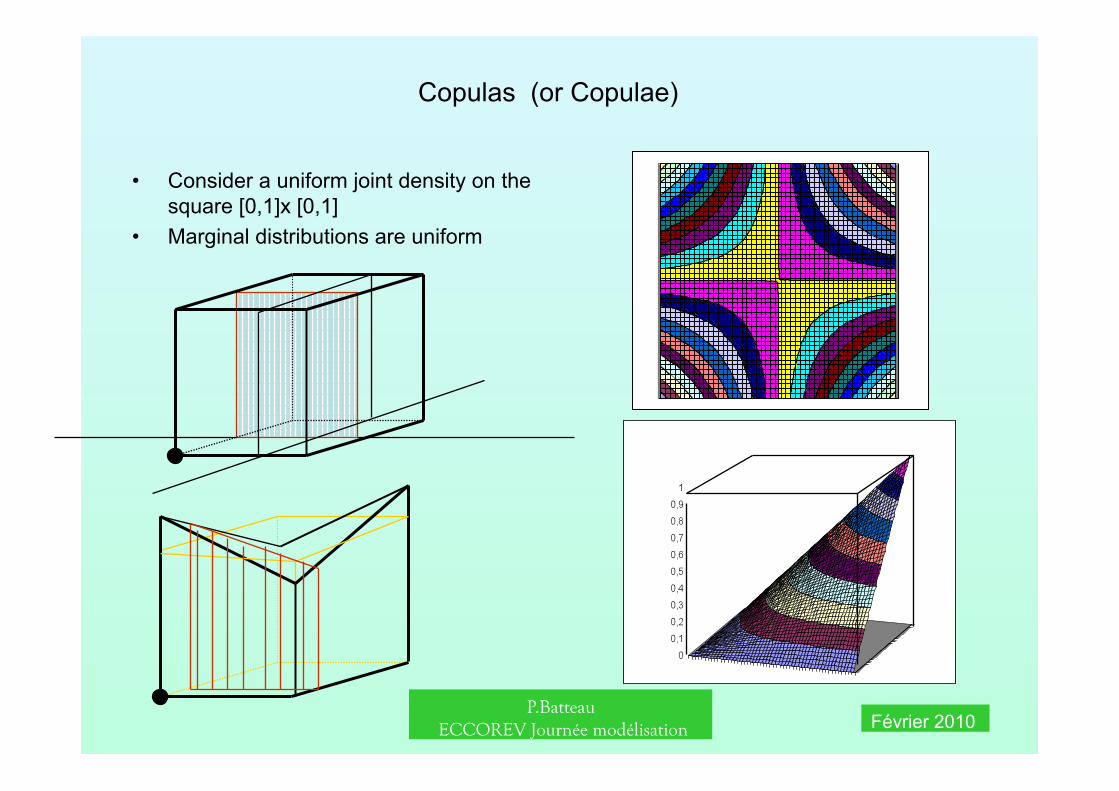

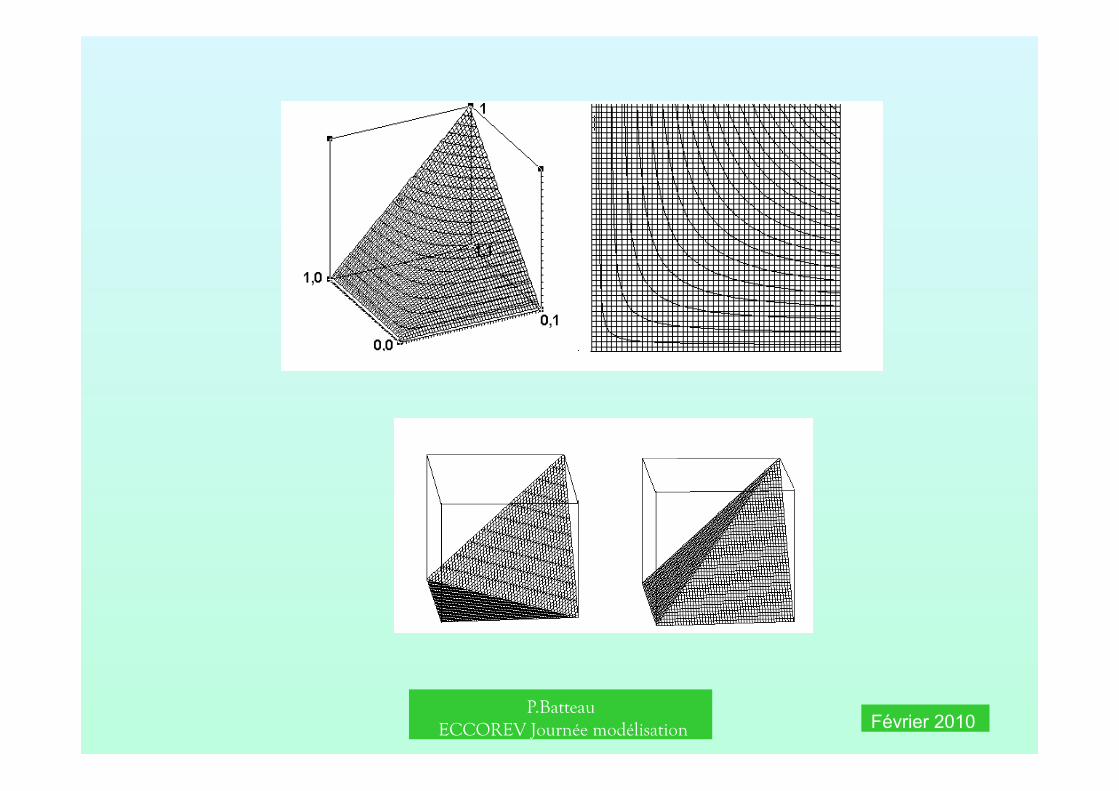

Copulas (or Copulae)

• Consider a uniform joint density on the square [0,1]x [0,1]

• Marginal distributions are uniform

P.Batteau ECCOREV Journée modélisation Février 2010

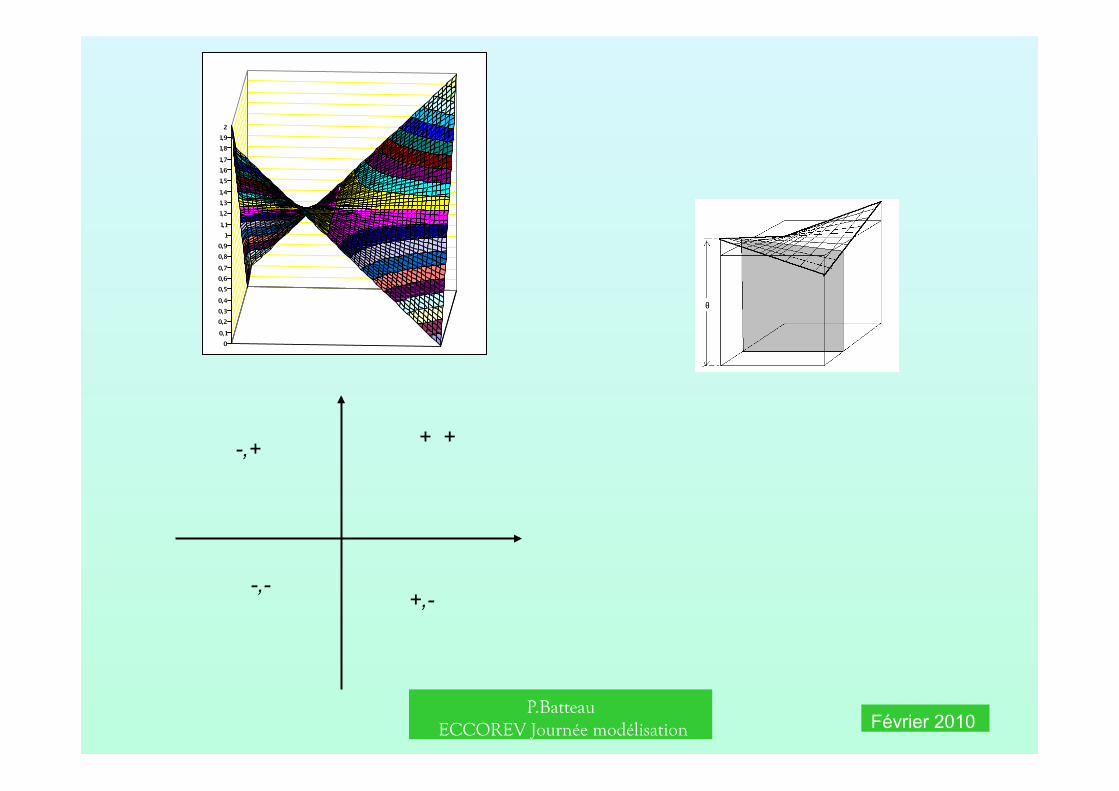

+ + -,+

+,- -,-

P.Batteau ECCOREV Journée modélisation Février 2010

P.Batteau ECCOREV Journée modélisation Février 2010

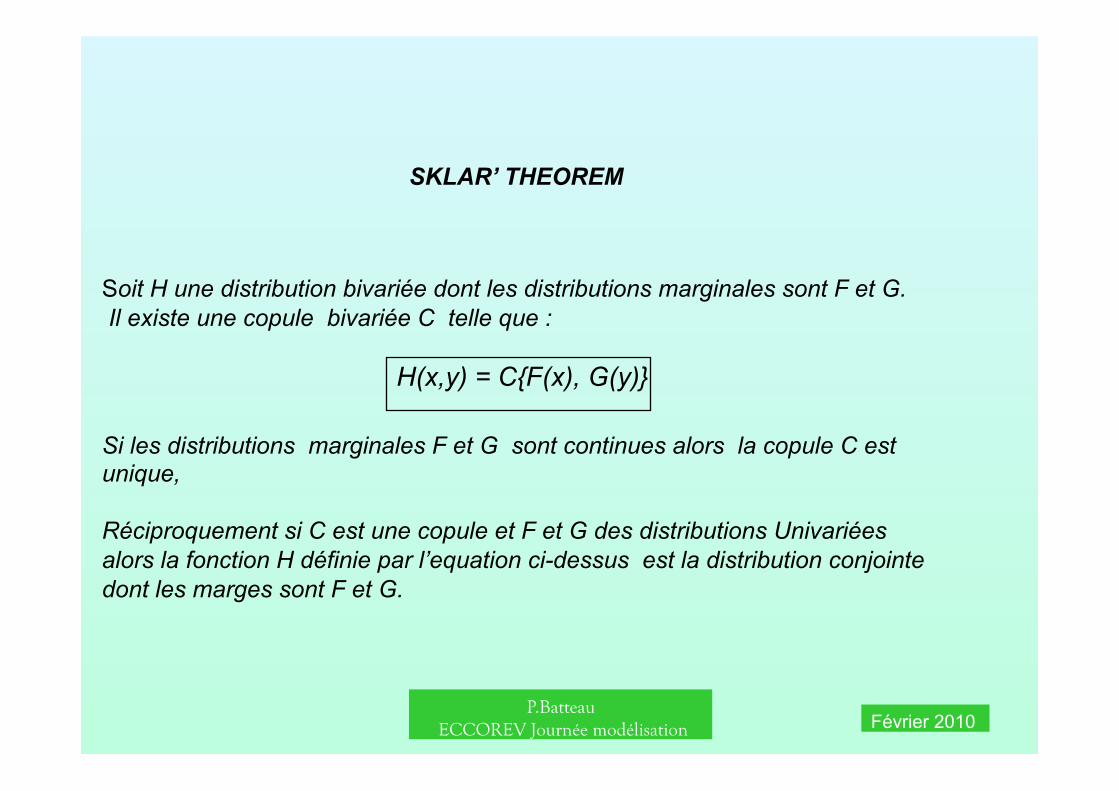

Soit H une distribution bivariée dont les distributions marginales sont F et G. Il existe une copule bivariée C telle que :

H(x,y) = C{F(x), G(y)}

Si les distributions marginales F et G sont continues alors la copule C est unique,

Réciproquement si C est une copule et F et G des distributions Univariées alors la fonction H définie par l’equation ci-dessus est la distribution conjointe dont les marges sont F et G.

SKLAR’ THEOREM

P.Batteau ECCOREV Journée modélisation Février 2010

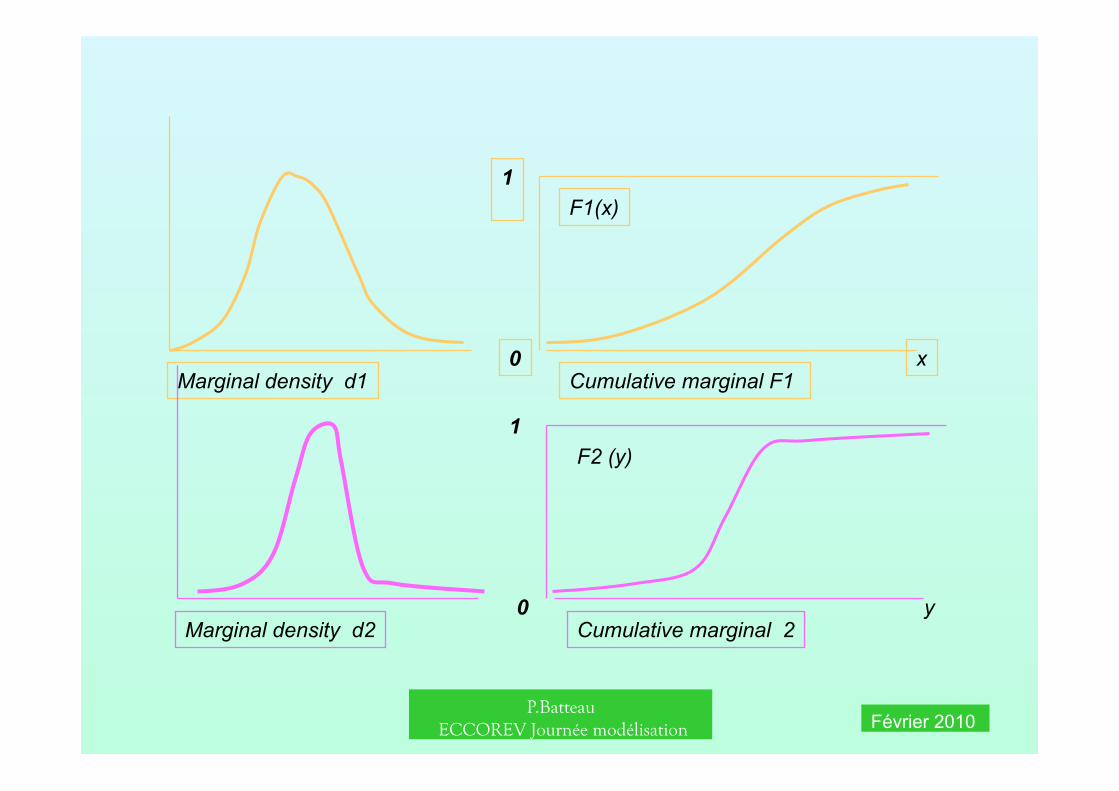

Marginal density d1 Cumulative marginal F1

F1(x)

x 0

1

Marginal density d2 Cumulative marginal 2

F2 (y)

y 0

1

P.Batteau ECCOREV Journée modélisation Février 2010

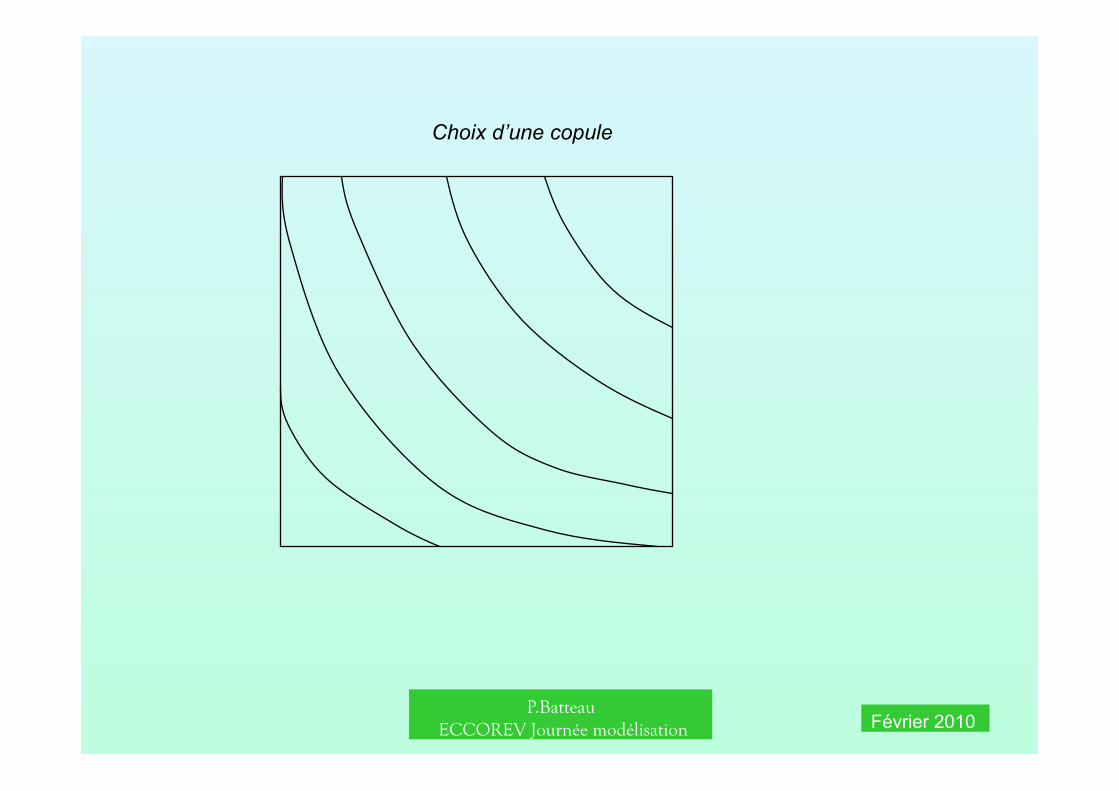

Choix d’une copule

P.Batteau ECCOREV Journée modélisation Février 2010

Cumulative of r1

Cumulative of r2 Joint density isolines

Copula isolines

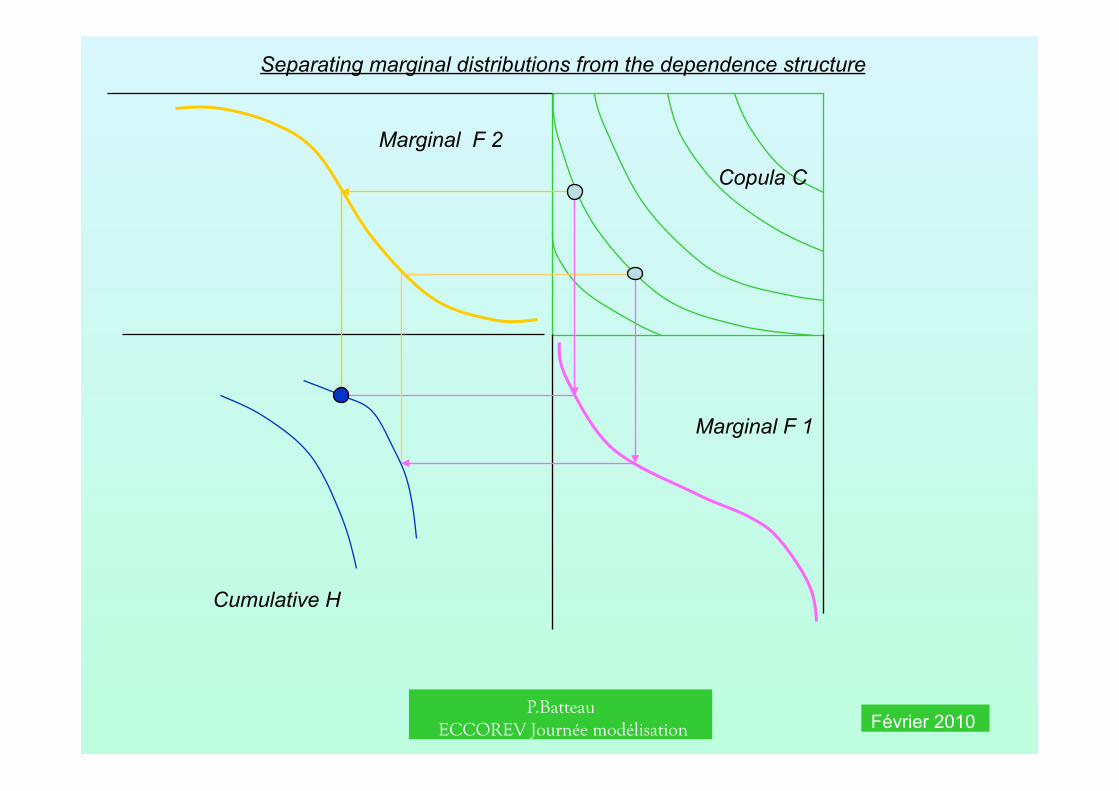

Separating marginal distributions from the dependence structure

P.Batteau ECCOREV Journée modélisation Février 2010

Copula C

Marginal F 1

Marginal F 2

Cumulative H

Separating marginal distributions from the dependence structure

P.Batteau ECCOREV Journée modélisation Février 2010

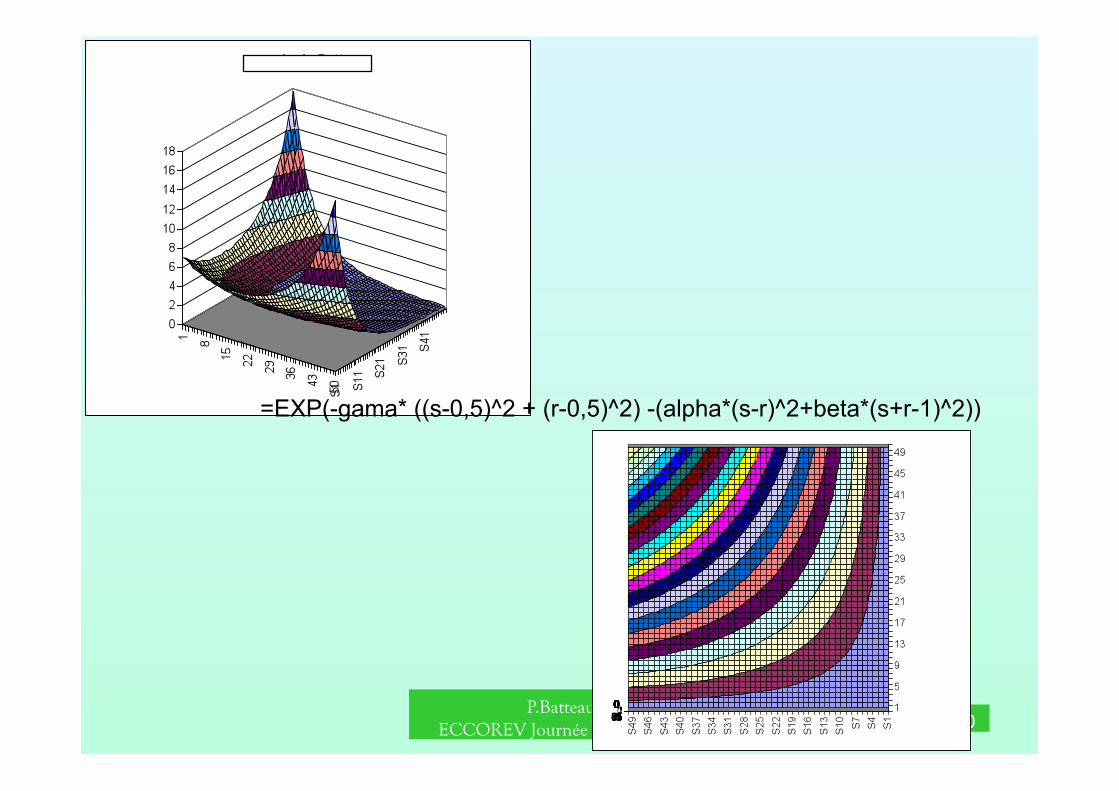

=EXP(-gama* ((s-0,5)^2 + (r-0,5)^2) -(alpha*(s-r)^2+beta*(s+r-1)^2))

P.Batteau ECCOREV Journée modélisation Février 2010

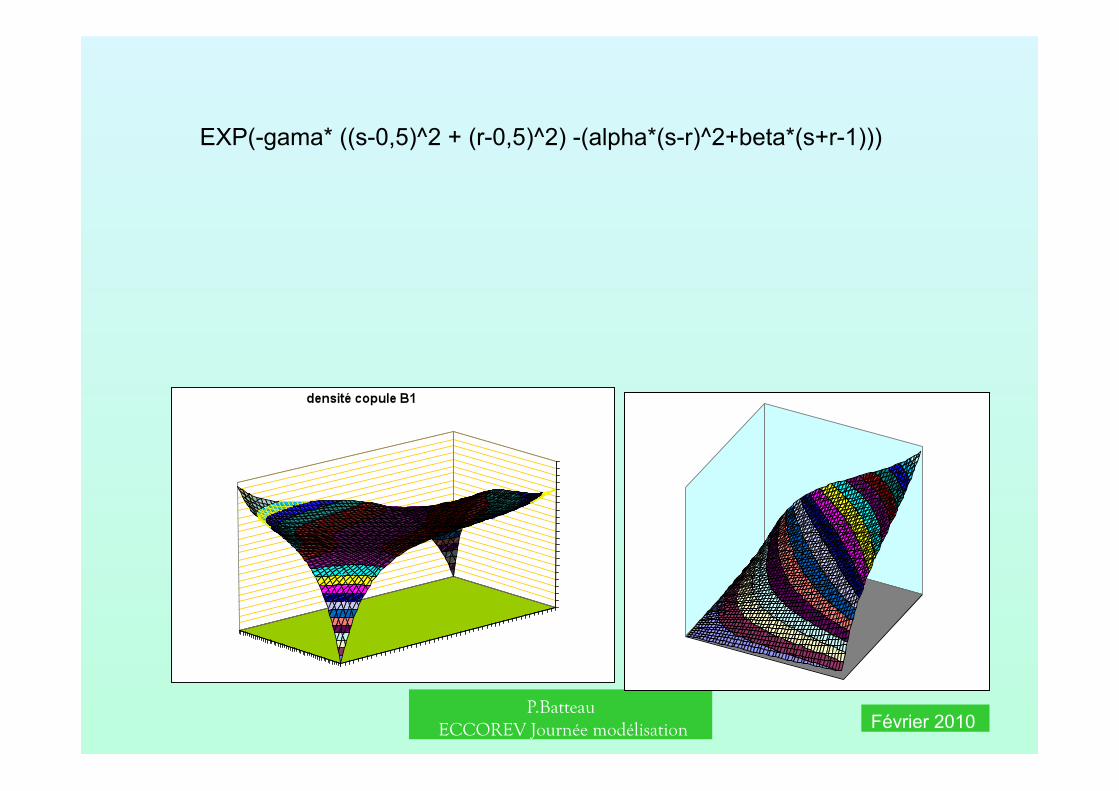

EXP(-gama* ((s-0,5)^2 + (r-0,5)^2) -(alpha*(s-r)^2+beta*(s+r-1)))

P.Batteau ECCOREV Journée modélisation Février 2010

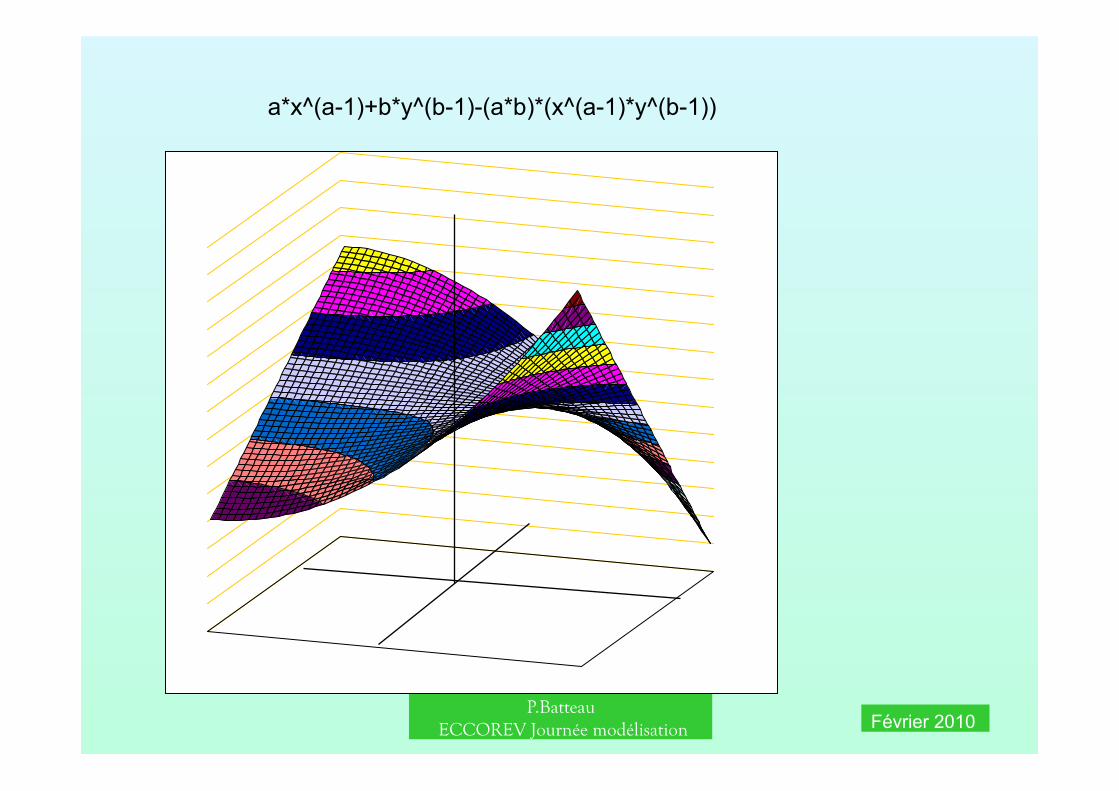

a*x^(a-1)+b*y^(b-1)-(a*b)*(x^(a-1)*y^(b-1))

P.Batteau ECCOREV Journée modélisation Février 2010

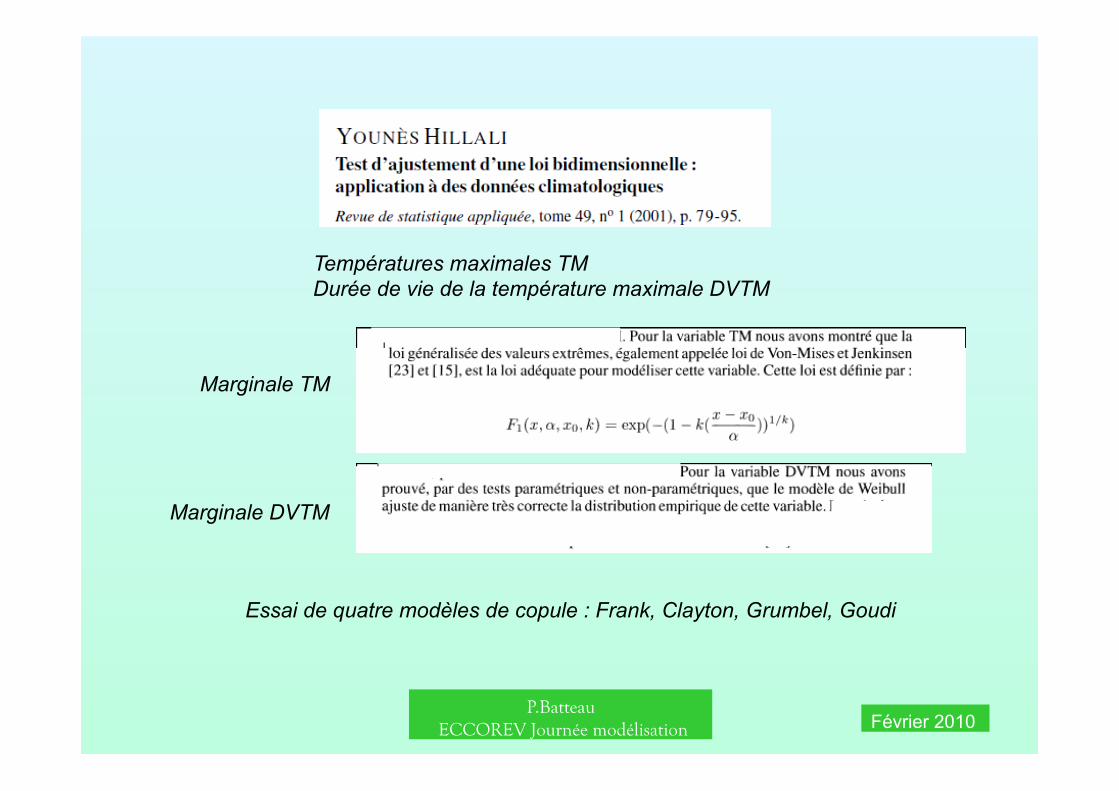

Températures maximales TM Durée de vie de la température maximale DVTM

Marginale DVTM

Marginale TM

Essai de quatre modèles de copule : Frank, Clayton, Grumbel, Goudi

P.Batteau ECCOREV Journée modélisation Février 2010

Modélisation multivariée des précipitations max-annuelles par copules pour l’étude de stationnarité des pluies méditerranéennes françaises. Nicolas PUJOL(1), Luc NEPPEL(1), Robert SABATIER(2) (1) Université Montpellier 2 – Maison des Sciences de l’Eau – UMR 5569 Hydrosciences – UM2 / CNRS / IRD [email protected], [email protected] (2) Laboratoire de physique industrielle et traitement de l’information – UFR Pharmacie, UM1 et EA 2415

Résumé : cet article étudie la modélisation multivariée des précipitations extrêmes via les copules gaussienne, de Student, et de Gumbel, et examine quelles sont les conséquences du choix de la modélisation sur l’étude régionale de stationnarité. Les illustrations montrent que ces trois modélisations engendrent des résultats très différents, tant au niveau du calcul des quantiles, en raison de l’estimation du paramètre de forme de la loi marginale GEV (Generalized Extreme Value), qu’aux niveaux du test de stationnarité et de l’ampleur des tendances qui varient du simple au double suivant la copule choisie.

P.Batteau ECCOREV Journée modélisation Février 2010

Le monde antique concevait l’incertitude comme relevant de l’action de trois femmes (les Parques) et les haruspices s’efforçaient de percer leur humeur. François 1er aussi voyait l’incertitude au féminin (“souvent femme varie et bien fol est qui s’y fie”) Nous attribuons aujourd’hui le risque aux caprices d’une Dame Nature et nos modèles s’efforcent de les prévoir.

Si le hasard est effectivement une invention conçue par une Grande Prêtresse, alors admirons sa subtilité, sa malice et sa profondeur, qualités que nous prêtons à la sensibilité féminine et reconnaissons humblement l’étendue de notre ignorance de son jeu, malgré la sophistication de nos modèles.

P.Batteau ECCOREV Journée modélisation Février 2010

P.Batteau ECCOREV Journée modélisation Février 2010