The impact of interactive use of time- driven activity ...

53

UNIVERSITEIT GENT FACULTEIT ECONOMIE EN BEDRIJFSKUNDE ACADEMIEJAAR 2008 – 2009 The impact of interactive use of time- driven activity based costing information on organizational capabilities Masterproef voorgedragen tot het bekomen van de graad van Master in de Toegepaste Economische Wetenschappen Mieke Putteman onder leiding van Prof. dr. W. Bruggeman

Transcript of The impact of interactive use of time- driven activity ...

UNIVERSITEIT GENT

FACULTEIT ECONOMIE EN BEDRIJFSKUNDE

ACADEMIEJAAR 2008 – 2009

The impact of interactive use of time-driven activity based costing information

on organizational capabilities

Masterproef voorgedragen tot het bekomen van de graad van

Master in de Toegepaste Economische Wetenschappen

Mieke Putteman

onder leiding van

Prof. dr. W. Bruggeman

UNIVERSITEIT GENT

FACULTEIT ECONOMIE EN BEDRIJFSKUNDE

ACADEMIEJAAR 2008 – 2009

The impact of interactive use of time-driven activity based costing information

on organizational capabilities

Masterproef voorgedragen tot het bekomen van de graad van

Master in de Toegepaste Economische Wetenschappen

Mieke Putteman

onder leiding van

Prof. dr. W. Bruggeman

PERMISSION

Ondergetekende verklaart dat de inhoud van deze masterproef mag geraadpleegd

en/of gereproduceerd worden, mits bronvermelding.

Mieke Putteman

i

PREFACE

This master thesis was not only my own achievement. There are some people who earn a word

of thanks.

First of all, I would like to thank my promoter Prof. Dr. Bruggeman, for his support, feedback and

recommendations.

Further thanks go to Peter Bruggeman, plant controller at PB Gelatins, who made an important

contribution to this thesis.

A special thanks to my parents and Wouter Vyverman for their support during these 4 years.

Without their faith, help and unconditional support, I wouldn‟t have been able to cover this

period.

Last but certainly not least, I would like to thank Natasja De Wit, who checked this paper for

spelling and grammar errors.

ii

TABLE OF CONTENTS

PREFACE………………………………………………………………………………………...i

TABLE OF CONTENTS………………………………………………………………………..ii

ABBREVIATIONS……………………………………………………………………………...iv

TABLES AND FIGURES………………………………………………………………………v

INTRODUCTION………………………………………………………………………………………….1

1.THEORETICAL CONTEXT…………………………………………………………………………...2

1.1 EVOLUTION OF COST SYTEMS……………………………………………………………...2

1.1.1 Traditional cost systems………………………………………………………………….2

1.1.2 Activity Based Costing…………………………………………………………………….3

1.1.3 Time-driven Activity Based Costing……………………………………………………..5

1.1.4 Time-driven Activity Based Costing: improvements…………………………………...7

1.2 ORGANIZATIONAL CAPABILITIES…………………………………………………………...9

1.3 INTERACTIVE USE OF MANAGEMENT CONTROL SYSTEMS………………………...12

1.3.1 Management Control Systems…………………………………………………………12

1.3.2 Diagnostic use……………………………………………………………………………12

1.3.3 Interactive use……………………………………………………………………………13

1.4 SYNTHESIS…………………………………………………………………………………….15

1.5 THEORETICAL MODEL………………………………………………………………………..17

2. METHODOLOGY…………………………………………………………………………………….19

2.1 CASE STUDY RESEARCH……………………………………………………………………19

2.1.1 Difficulties…………………………………………………………………………………19

2.1.2 High-quality case studies………………………………………………………………..20

2.1.3 Process steps…………………………………………………………………………….21

3. CASES AND RESULTS…………………………………………………………………………….23

3.1 WYMAR INTERNATIONAL…………………………………………………………………….23

3.1.1 Company introduction…………………………………………………………………...23

3.1.2 Time-driven Activity Based Costing project…………………………………………...24

3.1.3 Interactive use of time-driven ABC…………………………………………………….26

3.1.4 Organizational capabilities………………………………………………………………27

iii

3.2 PB GELATINS…………………………………………………………………………………...29

3.2.1 Company introduction…………………………………………………………………...29

3.2.2 Time-driven Activity Based Costing project…………………………………………...29

3.2.3 Interactive use of time-driven ABC…………………………………………………….33

3.2.4 Organizational capabilities………………………………………………………………33

3.3 CROSS – CASE ANALYSIS…………………………………………………………………..34

3.3.1 Interactive use……………………………………………………………………………34

3.3.2 Organizational capabilities………………………………………………………………34

3.4 CONCLUSIONS…………………………………………………………………………………36

4. DISCUSSION, LIMITATIONS AND RECOMMENDATIONS…………………………………...38

REFERENCES…………………………………………………………………………………………...vi

ANNEXES…………………………………………………………………………………………………x

iv

ABBREVIATIONS

ABC Activity-Based Costing

ERP Enterprise Resource Planning

MCS Management Control System

TD-ABC Time-Driven Activity Based Costing

P & L Profit and loss

KPI Key Performance Indicator

FTE Full Time Equivalent

ISO International Organization for

Standardization

v

TABLES AND FIGURES

Figure 1: Traditional Costing Systems

Figure 2: Activity based costing

Figure 3: Classifying capabilities

Figure 4: Theoretical model

Figure 5: Parameters commercial inside services Wymar International

Figure 6: P&L per client

Figure 7: Parameters PB Gelatins

Figure 8: Whale curve

Figure 9: Antecedent variables interactive use

Figure 10: Moderating and mediating variables

Table 1: Profit and loss per customer with the assigned blending costs

Table 2: Variances on indirect costs

Table 3: “Menu”

1

INTRODUCTION

In the complex and dynamic environment of today, it is very important for companies to know the exact

product costs and profitability of products, services and strategies. Cost systems must be able to quickly

adapt to changing circumstances. Ever increasing competition and globalisation result in high risks when

wrong decisions have been made based on wrong figures.

As a response to these circumstances, time-driven activity based costing (TD-ABC) was developed. This

system provides accurate cost and profitability information at a low cost manner.

The objective of this paper is to understand how and when the use of time-driven activity based costing

information impacts the following four organizational capabilities, namely innovativeness, market

orientation, organizational learning and entrepreneurship. These capabilities are considered to be the

primary capabilities of a company to create and sustain a competitive advantage.

More specifically, the impact of the interactive use of the TD-ABC information is covered. Interactive use

is characterized by communication across the organization, top management attention, meetings … The

information „flows‟ through the organization and can be used to identify critical points in the processes.

In Henri‟s paper (2006) “Management control systems and strategy: a resource-based perspective”, the

interactive use of management control systems had a positive impact on the organizational capabilities.

This paper refines the theory set out by Henri. Time-driven activity based costing can be seen as a

management control system. As a result, it can be expected that the interactive use of TD-ABC will also

have a positive impact on the organizational capabilities.

To test these hypotheses, a case study in two companies has been set out. These companies operate in

the chemical industry, a sector that is characterized by complexity. It is especially in such an environment

that TD-ABC will be an important added value.

In this paper chapter one covers the theoretical context of this paper. We begin with the evolution of cost

systems followed by a summary on the literature of organizational capabilities and interactive use of

management control systems. Furthermore this chapter gives the theoretical model used in this paper.

In chapter two, an overview of the methodology used and the companies examined is given. Chapter

three gives the actual results of the case study.

And finally, chapter four provides a discussion on the results, the limitations of the research and

recommendations for further research.

2

1. THEORETICAL CONTEXT

This first chapter covers the literature available on the subject. We start with the evolution of cost

systems. Next, we cover the organizational capabilities. Afterwards, the interactive use of management

control systems is treated. And finally, we synthesize the theoretical context to develop a theoretical

model.

1.1 EVOLUTION OF COST SYSTEMS

“The objective of cost systems is to make an accurate estimation of product costs of different cost objects

(customers, representatives, products …) in order to provide the management relevant information to

make decisions, to improve business processes and to manage departments” (Cooper & Kaplan, 1988).

In this section, an overview of different cost systems is given.

1.1.1 Traditional cost systems

Traditional cost systems are based on the distinction between direct and indirect or overhead costs.

Direct costs have a clear, quantifiable relationship with a specific activity or product. Examples are direct

salaries, components of a product …

Indirect costs have no such relationship. They are often more general costs, the registration of the

specific cost per product or activity is not possible or this registration is simply not done in the company

(Bruggeman, Hoozée, Moreels & Bruyneel, 2007). Electricity, water, rent … are all examples of indirect

costs. These indirect costs are first aggregated in a cost pool and then assigned to the different products

on basis of a driver, very often direct labour hours or machine hours. High volume products require many

labour and machine hours, so they are assigned more indirect costs.

To calculate the total cost of a product, the direct costs are raised with the surcharge for the indirect

costs.

INDIRECT COSTS

PRODUCTS

Direct labour hours Machine-hours

Direct material Direct labour

Figure 1: Traditional Costing Systems (Source: Kaplan and Cooper, 1998)

3

This system, however, has some important shortcomings.

Firstly, errors appear because the indirect costs in a cost pool are not homogeneous. This means that the

causal link between the costs and the cost objects is not the same for all costs. The aggregated costs

can‟t be allocated to the different cost objects via the same driver. For example, the costs of the purchase

department can be allocated by use of material. However, parts of these costs, such as personnel costs,

do not have a causal relationship with the use of material. Thus, the costs aggregated at the purchase

department are not homogeneous.

Secondly, many companies use the wrong drivers to allocate the indirect costs. It is often assumed that

the indirect costs have a causal relationship with direct labour hours, where in fact there isn‟t such a

relationship.

Thirdly, the information provided by the traditional cost systems has a limited usability when it comes to

the support of management decisions and the control of cost processes. Traditional systems don‟t give a

clear understanding on the origin of costs and provide insufficient support for continuous improvement.

Finally, the emergence of new technologies, diversity in product offers, production on order … makes the

traditional system inadequate. Volume-based drivers like direct labour hours are no longer of use in this

environment.

As a reaction to these distortions, Kaplan and Cooper developed a new type of cost system: Activity

Based Costing (ABC).

1.1.2 Activity Based Costing

Activity Based Costing gives a more accurate view on reality. ABC recognizes that some costs do not

vary with a volume measure but with some other measures (Dickinson and Lere, 2003). It‟s a more

sophisticated approach to attributing indirect costs (resources …), first to activities and then to cost

objects which create demand for these indirect costs. As a result, better decisions are made. The system

is able to provide more accurate information on costs so that management can focus its attention on

products and processes accounting for more profit (Cooper and Kaplan, 1988).

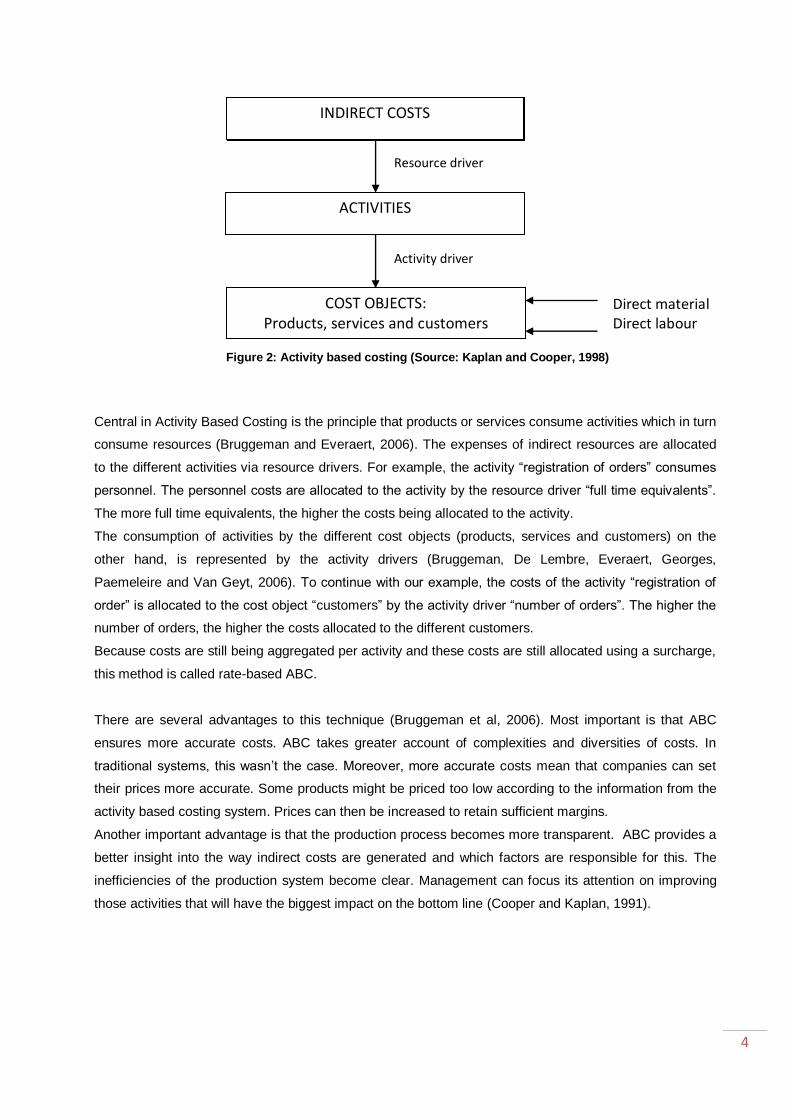

An ABC-system contains the following stages (Bruggeman and Everaert, 2006):

1) Identify activities

2) Determine the costs of the activities

3) Determine the cost drivers of the activities

4) Determine the volume of cost drivers

5) Determine unit cost per cost driver for each activity

6) Calculate the unit cost per product or service

4

Central in Activity Based Costing is the principle that products or services consume activities which in turn

consume resources (Bruggeman and Everaert, 2006). The expenses of indirect resources are allocated

to the different activities via resource drivers. For example, the activity “registration of orders” consumes

personnel. The personnel costs are allocated to the activity by the resource driver “full time equivalents”.

The more full time equivalents, the higher the costs being allocated to the activity.

The consumption of activities by the different cost objects (products, services and customers) on the

other hand, is represented by the activity drivers (Bruggeman, De Lembre, Everaert, Georges,

Paemeleire and Van Geyt, 2006). To continue with our example, the costs of the activity “registration of

order” is allocated to the cost object “customers” by the activity driver “number of orders”. The higher the

number of orders, the higher the costs allocated to the different customers.

Because costs are still being aggregated per activity and these costs are still allocated using a surcharge,

this method is called rate-based ABC.

There are several advantages to this technique (Bruggeman et al, 2006). Most important is that ABC

ensures more accurate costs. ABC takes greater account of complexities and diversities of costs. In

traditional systems, this wasn‟t the case. Moreover, more accurate costs mean that companies can set

their prices more accurate. Some products might be priced too low according to the information from the

activity based costing system. Prices can then be increased to retain sufficient margins.

Another important advantage is that the production process becomes more transparent. ABC provides a

better insight into the way indirect costs are generated and which factors are responsible for this. The

inefficiencies of the production system become clear. Management can focus its attention on improving

those activities that will have the biggest impact on the bottom line (Cooper and Kaplan, 1991).

Figure 2: Activity based costing (Source: Kaplan and Cooper, 1998)

Direct material Direct labour

INDIRECT COSTS

COST OBJECTS: Products, services and customers

ACTIVITIES

Resource driver

Activity driver

5

Despite these advantages, there are some important shortcomings (Bruggeman and Everaert, 2007):

1) The ABC model is not accurate:

ABC is used to reduce specification (wrong activity driver) and aggregation errors (costs are

aggregated in heterogeneous activities). Unfortunately, this leads to an increased number of

measurement errors. Information on the exact cost and the nature of the use of resources is more

difficult to obtain in case of disaggregated resource groups. Suppose that the activity “order

processing” contains two sub activities “insert data” and “control of credit worthiness”. People will

be more able to estimate the time they spend on the activity “order processing” as a whole rather

on the two sub activities. To compensate for these increased errors, companies use less detailed

ABC-systems. By doing so, costs become less accurate.

2) The ABC-model is too complex:

When operations become more complex, activities need to be added, activity drivers need to be

identified, volume for each driver needs to be determined … The ABC-model will become more

complex and high demands will be placed on computer systems.

3) The development of a complex ABC-system requires a lot of time:

interviews, definitions of activities, determination of cost drivers …

4) Difficult to keep up-to-date:

When the system needs to be reviewed, people need to be interviewed again, employees have to

make new estimates … That is why companies only review the system once or twice a year

which results in costs being

5) ABC starts from full capacity:

The interviewees give percentages equalling 100. Few people indicate that part of their time is

unused. Therefore, the unit cost per cost driver is usually too high because it contains the cost of

the unused capacity.

To respond to these shortcomings, a new concept was developed by Kaplan and Anderson: Time-driven

Activity Based Costing (TD-ABC).

1.1.3 Time-driven Activity Based Costing

“A time-driven ABC model identifies the capacity of each department or process and assigns the cost of

this capacity to the volume and mix of work performed. If, through continuous improvement or

rationalization of product lines, orders and customers, the company reduces the demand for work in these

different departments and processes, the time-driven ABC model estimates the quantity of resources no

longer needed so that managers can take steps to redeploy these resources or manage them out of the

company” (Kaplan, 2006).

In this system, the time needed to fulfil an activity plays a crucial role. Time-driven ABC divides the costs

of resource groups over the cost object based on the time required to perform an activity.

Only 2 parameters need to be determined for each activity, namely the unit cost of the used resources

and the time required to perform the activity.

6

The time-driven approach consists of six steps (Bruggeman et al., 2007):

1. Identify resource groups and the activities for which they are used

2. Determine the costs of each group

3. Estimate the practical capacity of each group

4. Calculate the cost per time unit

5. Determine the required time units for each activity

6. Calculate the cost per transaction

The execution of an activity doesn‟t always require the same time. An activity can require more or less

time depending on its characteristics. Companies can generally predict the characteristics that cause the

complexity of an activity (Kaplan and Anderson, 2007). For example, the activity “packaging” might

require more time when new packaging material is necessary, when the goods need to be placed in a

special box…

To capture these complexities, TD-ABC uses time equations. Such an equation expresses the time which

is consumed by a certain event of an activity in function of different characteristics, the so-called time

drivers. The need for new material and the need for a special box are both examples of time drivers.

This equation is generally represented as follows (Bruggeman et al., 2007):

tj,k = ß0 + ß1.X1 + ß2.X2 + … + ßp.Xp

With tj,k = time required for event k of activity j

ß0 = constant amount of time for activity j, independent of the

characteristics of event k

ßi = consumption of time for 1 unit of time driver i (i = 1 … p)

Xi = time driver i (i = 1 … p)

p = number of time drivers which determine the time required

to perform activity j

These time equations ensure that the time required and the costs of the activities are being allocated to

the cost objects, taking into account the characteristics of each cost object.

The time equations show which activities demand more time and thus result to higher costs (Pernot,

Roodhooft, Van den Abbeele, 2007).

For example, some customers require more time from a representative than others do. Thus, these

customers will be assigned more costs than others.

Time-driven ABC visualizes which activities consume the largest amount of time and are thus most

suitable for improvement, in order to reduce the total cost (Pernot et al., 2007).

Time-driven activity based costing has made some important improvements to management accounting,

which are treated in the following section.

7

1.1.4 Time-driven Activity Based Costing: improvements

Time-driven ABC has made some important improvements to rate-based ABC (Bruggeman et al., 2007):

1. Time-driven ABC leads to more accurate product costs

When employees need to estimate the time to perform an activity, this estimate will be more

accurate than when they have to divide percentages over a list of activities. When linked to the

ERP-system, actual transaction data can be inserted into the time equation, making it more

accurate.

Moreover, possible errors are automatically discovered when the model is tested. Big differences

in actual processing times and estimates are indications of mistakes in the time equations.

2. Time-driven ABC can be implemented faster

The resources no longer need to be allocated to individual activities. The costs are aggregated

per department.

Furthermore, time-driven ABC models can easily be applied and modified for other plants and

companies in the same industry, because the processes they use are similar.

3. Time-driven ABC model can be easily altered

The model can be updated and aligned with changed circumstances in a simple way. When new

activities emerge within the company, it‟s sufficient to define the activity and to capture the time

equations. Time equations can also easily be altered to changes in existing activities.

4. Time-driven ABC makes overcapacity visible

Time-driven ABC works with practical capacity. In this way the percentage of this capacity that is

actually used, can easily be checked. The costs of unused capacity are not included in the

calculation of costs.

5. Time-driven ABC provides information on the efficiency of business processes

The time equations demonstrate which characteristics of an activity require a lot of time. Hence,

time-driven ABC becomes a tool for improving of the efficiency of business processes.

6. Time-driven ABC makes simulations possible

For instance, “what-if” analysis can indicate what the impact is of e.g. more efficient processes

(less time needed), other characteristics of the activity …

7. Time-driven ABC has predictive value

When circumstances change, time equations enable a more accurate estimate of the impact it

can have on an organization in terms of both cost and time. Management can easily predict what

the impact of certain decisions on the committed capacity will be. Moreover, they have the ability

to predict which amount of their unused capacity can be used for new initiatives.

8. Time-driven ABC allows enterprise-wide systems

Time-driven ABC can easily be integrated and linked in the monthly, enterprise-wide profitability

reports and the ERP-system.

8

9. Time-driven ABC provides a faster understanding in profitability

By linking time-driven ABC to the ERP-system, profitability reports on customers, products … can

be generated directly after the closure of the period.

10. Time-driven ABC creates information to negotiate with trading partners

Time-driven ABC provides understanding in the actual costs and profitability of processes and

cost objects. Complex processes can easily be identified and reported. Hence, negotiations with

customers and suppliers can be based on more sustainable grounds.

Time-driven ABC is an answer to the shortcomings of the traditional ABC system. To summarize, time-

driven ABC offers a lot of possibilities in the analysis of profitability and reporting of capacity utilization in

complex and dynamic environments. The system provides more accurate costs, which leads to better

decision-making by the management.

9

1.2 ORGANIZATIONAL CAPABILITIES

“Capabilities are action-based resources which are developed by groups and teams when the skills of

individuals are coordinated in repeatable patterns of action in the use of assets”. This means that groups

or teams of individuals are able to coordinate their skills in carrying out a process of importance to an

organization‟s overall value-creating activities. For example, a team of production workers who can

consistently manufacture high-quality products (Sanchez and Heene, 2004).

“Capabilities are the organizational processes by which firms synthesize and acquire knowledge and

resources, and generate new applications from those resources” (Kogut and Zander, 1992). “They are

complex bundles of skills and collective learning, exercised through organizational processes, which

ensure superior coordination of functional activities (Day, 1994). Thus, capabilities and organizational

processes are closely entwined, because it is the capability that enables the activities in a business

process to be carried out”. Moreover, when capabilities of the various groups and teams of people in the

organization can be coordinated to work together in a way that enables the organization to achieve its

goals, organizational competences can arise (Sanchez and Heene, 2004).

Every business acquires many capabilities that enable the business to carry out the activities necessary

to move its products or services through the value chain. Some capabilities must be superior if the

business wants to outperform its competitors. These capabilities are called „distinctive capabilities‟ (Day,

1994). Distinctive capabilities are hard to imitate by competitors. They are robust and can be used to

adapt to environmental change.

Capabilities can be sorted into three categories (Day, 1994). Figure 3 presents a scheme of this

classification.

On the one hand, there are the inside-out capabilities. They are activated by market requirements,

competitive challenges and external opportunities. Examples are financial management, cost control

technology development …

On the other hand, there are the outside-in capabilities whose focal point is almost exclusively outside the

organization. The purpose of these capabilities is to connect the processes defining the other

organizational capabilities to the external environment and enable the business to compete by

anticipating market requirements ahead of competitors and creating durable relationships with customers,

channel members and suppliers. Examples are market sensing processes, customer linking processes,

channel bonding …

Finally, spanning capabilities are needed to integrate the inside-out and outside-in capabilities. Examples

are pricing, purchasing, customer service delivery …

10

A firm‟s capabilities are the source of any sustainable competitive advantage a firm achieves in its

markets (Grant, 1991). Grant refers to organizational capabilities as the “ability to

perform repeatedly a productive task which relates either directly or indirectly to a firm‟s capacity for

creating value through effecting the transformation of inputs into outputs”. Resources serve as the input

or source of the capabilities of a firm.

This paper treats four organizational capabilities: innovativeness, organizational learning, market

orientation and entrepreneurship. These capabilities are considered to be primary capabilities to reach

competitive advantage, to match and create market change. Many studies have shown the positive

impact of these capabilities on the performance of a company (e.g. Hult and Ketchen, 2001; Henri, 2006).

“Each of these four capabilities is adequate to offer strengths, but is not sufficient to develop sustained

advantages. Only collectively can they help a firm to be uniquely competitive” (Henri, 2006). “These

capabilities are not expected to cause advantages, but rather they are predicted to be elements that

collectively contribute to the development of a positional advantage” (Hult and Ketchen, 2001). These

capabilities are defined as follows.

Firstly, according to Hurley and Hult (1998) innovativeness refers to the notion of openness to new ideas,

products and processes, and its orientation towards innovation. Innovation is seen as one of the most

important components of a firm‟s strategy (Ireland, Hitt, Camp and Sexton, 2001). It is a necessary

element to be able to compete effectively and it is an important part of the strategy of a company (Henri,

2006). “Firms that have a greater capacity to innovate are able to develop a competitive advantage and

achieve higher levels of performance” (Hurley and Hult, 1998). An organization that pursues new

opportunities but is not innovative in meeting the desires of the market is unlikely to enjoy long-term

success.

Figure 3: Classifying capabilities (Source: Day, 1994)

11

Secondly, “organizational learning refers to the development of insights, knowledge and associations

among past actions, the effectiveness of these actions, and future actions” (Fiol and Lyles, 1985). Basic

values of the company include learning as a key to improvement. Employee learning is an investment, not

an expense (Henri, 2006).

An organization can extract lessons from both successes and failures in order to be more competitive in

the future. “It is considered to be an important facilitator of competitive advantage by improving a firm‟s

information processing activities at a faster rate than rivals do” (Baker and Sinkula, 1999). Organizational

learning happens by information acquisition, information dissemination, and shared interpretation (Ireland

et al., 2001).

Thirdly, “market orientation refers to the organizational emphasis on customers‟ expressed needs and on

the development of long-term thinking based on customers‟ latent needs” (Slater and Narver, 1999).

Communication about customer experience, understanding of customer needs, measurement of

customer satisfaction, after-sales service … are all important items relating to market orientation.

“The distinguishing characteristic of market orientation is system-wide attention to markets (customers,

competitors and other entities in the environment) throughout the organization” (Hult and Ketchen, 2001).

It mainly consists of three components, namely customer orientation, competitor orientation and inter-

functional coordination. As an example, important items of these three components are respectively

measurement of customer satisfaction, discussion about competitors‟ strengths and strategies as well as

communicating information about customer experience. “Market orientation creates the necessary

behaviours for the development of superior value for customers and thus continuous performance for the

business” (Narver and Slater, 1990).

Finally, “entrepreneurship refers to the ability of the firm to continually renew, innovate and take

constructive risks in its markets and areas of operation” (Naman and Slevin, 1993). “It refers to the pursuit

of new market opportunities and the renewal of existing areas of operation. It‟s a critical organizational

process that contributes to the survival and performance of the firm”. Examples of entrepreneurial actions

are creating new resources or combining existing resources in new ways to develop and commercialize

new products, move into new markets, and service new customers (Ireland et al., 2001).

12

1.3 INTERACTIVE USE OF MANAGEMENT CONTROL SYSTEMS

1.3.1 Management Control Systems

According to Simons (1987), “Management control systems (MCS) are formalized procedures and

systems that use information to maintain or alter patterns in an organizational activity”. “It refers to the set

of procedures and processes that managers and other organizational participants use in order to help

ensure the achievement of their goals and the goals of their organization” (Otley and Berry, 1994).

“Management control systems include all the devices and systems managers use to ensure that the

behaviours and decisions of their employees are consistent with the organization‟s objectives and

strategies, but exclude pure decision-support systems” (Malmi and Brown, 2008).

Examples are planning systems, reporting systems, budgeting systems, cost systems and monitoring

systems that are based on the use of information. As such, Time-driven ABC is a specific example of a

management control system. In management control, accounting information is used as a measure

whereby operational activities can be monitored and controlled (Otley and Berry, 1994).

The MCS must be aligned with capabilities to be effective and to be consistent with the strategy of the

organization.

“The essence of MCS is to manage the inherent organizational tension between creative innovation and

predictable goal achievement. More specifically, three kinds of inherent tension must be aligned to allow

the effective control of business strategy: unlimited opportunity versus limited attention, intended versus

emergent strategy and self-interest and desire to contribute.

Managers use MCS as positive and negative forces to create dynamic tension that contributes to manage

inherent organizational tension” (Henri, 2006).

These positive and negative forces are represented respectively by the interactive use and the diagnostic

use.

1.3.2 Diagnostic use

The diagnostic use of MCS represents the traditional feedback role. MCS are then used on an exception

basis to monitor and reward the achievement of pre-established goals. Goals are set in advance,

outcomes are compared with preset objectives and significant variances are reported to managers for

remedial action and follow-up (Anthony, Dearden and Bedford, 1989). Through the diagnostic use, critical

success factors are communicated and monitored (Tuomela, 2005). MCS will focus on and correct

deviations from preset standards of performance. It provides motivation and direction to achieve the goals

of the organization. The diagnostic use monitors and coordinates the implementation of the intended

strategies. “These strategies are approved by top managers, plans are communicated downward through

the organization, and formal systems are used to inform top managers if actions or outcomes are not in

accordance with intended plans” (Simons, 1991).

13

The diagnostic use of MCS represents a negative force mostly because it focuses on mistakes and

negative variances. It creates constraints and ensures compliance with standards. In this way, it

encourages conservatism and a „playing it safe‟ attitude. Specifically, it limits the role of MCS to a

measurement tool.

Moreover, diagnostic use may not represent an adequate means to foster the organizational capabilities

used in this paper. The diagnostic use represents a mechanistic control used to track, review and support

the achievement of predictable goals. A mechanistic control contains two important features: tight control

of operations and strategies, and highly structured channels of communication and restricted flows of

information.

Firstly, due to the tight control, there is no attention paid to changing circumstances and the need for

innovation. Hence, the diagnostic use limits the deployment of the capabilities by providing boundaries

and by restricting risk-taking. Secondly, the deployment of the capabilities requires free flow of

information and open channels of communication. However, the diagnostic use reinforces the existing

lines of authority and responsibility. At best, the diagnostic use leads to corrective action but this is not

sufficient to sustain the capabilities. A diagnostic use tends to negatively influence the organizational

capabilities (Henri, 2006).

1.3.3 Interactive use

In certain circumstances, top management uses MCS more actively on a day-to-day basis to intervene in

organizational decision-making. Top management uses the system to personally and regularly involve

themselves in the decisions of subordinates.

According to Simons (1991), this interactive use encompasses four conditions:

1. Info generated by MCS is an important and recurring agenda addressed by the highest levels

of management

2. The process demands frequent and regular attention from operation managers at all levels of

the organization

3. Data are interpreted and discussed in face-to-face meetings of superiors, subordinates and

peers

4. The process relies on the continual challenge and debate of underlying data, assumptions and

action plans

The interactive use of MCS focuses attention and forces dialogue throughout the organization. MCS are

then used to expand opportunity-seeking and learning throughout the company. Interactive use allows top

management to send signals throughout the organization which stimulate attention toward top

management preferences, strategic uncertainties and organizational goals and objectives. As a result,

“interactive control systems place pressure on operating managers at all levels of the organization, and

motivate information gathering, face-to-face dialogue and debate. As participants throughout the

14

organization respond to the perceived opportunities and threats, organizational learning is stimulated,

new ideas flow and strategies emerge” (Bisbe and Otley, 2004).

Interactive control systems are used to discuss strategic uncertainties and to learn how to cope with a

changing environment (Tuomela, 2005). More specifically, “it stimulates the development of new ideas

and initiatives and guides the bottom-up emergence of strategies by focusing on strategic uncertainties”

(Henri, 2006). The interactive use supports double-loop learning. This means that next to detecting and

correcting mistakes, the company will question its existing procedures and policies1.

The interactive use of MCS is an organic control system supporting the emergence of communication

processes and the mutual adjustment of organizational actors. In organic control systems two features

are important. On the one hand, loose and informal control reflecting norms of cooperation,

communication and emphasis on getting things done. On the other hand, open channels of

communication and free flow of information throughout the organization.

Interactive use contributes to the expansion of the organization‟s information processing capacity and

fosters interaction among organizational actors. Consequently, it represents an adequate means to foster

market orientation, entrepreneurship, innovativeness and organizational learning (Henri, 2006).

1 Argyris, C. and D. Schön, 1978, Organisatorisch leren, URL:

< http://www.12manage.com/methods_organizational_learning_nl.html>

15

1.4 SYNTHESIS

Time-driven Activity Based costing is a breakthrough in management accounting. This cost system

provides more accurate product costs, can be implemented faster and is easier adaptable than traditional

cost systems. Moreover, excess capacity becomes visible, it provides information on the efficiency of

business processes and gives a clear insight into the profitability of cost objects.

The time-driven ABC system can be seen as a management control system. Its objective is to control and

monitor operational activities by using accounting information. The information obtained from the time-

driven ABC system can for example show which activities demand a huge amount of time and thus a lot

of costs. Consequently, these activities can be made more efficient in order to reduce costs.

Management control systems can be used in an interactive way. The interactive use forces dialogue

throughout the organization and stimulates attention toward top management preferences, strategic

uncertainties and organizational goals and objectives. It ensures information gathering and face-to-face

dialogue together with debate at all levels of the organization.

In the case of time-driven ABC, the interactive use of this system means that its information can be used

throughout the organization and is interpreted and discussed in meetings of superiors, subordinates and

peers. Moreover, its parameters are continually challenged and debated. Top management uses the

time-driven ABC model on a day-to-day basis to intervene in organizational decision-making. In this way,

it represents an adequate means to foster organizational capabilities (Henri, 2006).

Capabilities are action-based resources developed by groups and teams. They arise when “the skills of

individuals are coordinated in repeatable patterns of action in the use of assets” (Sanchez and Heene,

2004). Individuals coordinate their skills to carry out an important value-creating activity for the

organization.

Some capabilities must be superior to those of the competitor if the organization wants to outperform the

competitor. Four organizational capabilities are extremely important in obtaining and retaining this

competitive advantage (Henri, 2006). These capabilities are innovativeness, organizational learning,

market orientation and entrepreneurship.

Innovativeness refers to the openness to new ideas, products and processes. Firms that have a larger

capacity to innovate are able to achieve higher levels of performance.

Organizational learning refers to “the development of insights, knowledge and associations among past

actions and the effectiveness of these actions” (Fiol and Lyles, 1985). An organization can learn from

both successes and failures of the past in order to be more competitive in the future.

Market orientation consists of three components: customer orientation, competitor orientation and inter-

functional coordination. It refers to the emphasis on the expressed and latent needs of customers.

Moreover, attention to competitors and suppliers is important. Market orientation creates the necessary

behaviours for the continuous performance of the business.

16

Finally, entrepreneurship refers to “the ability of the firm to continually renew, innovate and take

constructive risks in its markets and areas of operation” (Naman and Slevin, 1993). New market

opportunities are pursuit and the existing markets are renewed. Entrepreneurship is critical to the survival

and performance of the firm.

The management control system, in this case the time-driven activity based costing system, must be

aligned with capabilities to be effective and to be consistent with the strategy of the organization.

Henri (2006) investigated the impact of the interactive use of Management control systems on the four

organizational capabilities. The results showed that the interactive use had a positive impact on these

capabilities.

Consequently, we suggest that the interactive use of Time-driven ABC will also have a positive influence

on innovativeness, organizational learning, market orientation and entrepreneurship.

In the next section, we develop a theoretical model based on the literature described above.

17

1.5 THEORETICAL MODEL

The objective of this paper is to investigate whether the interactive use of time-driven activity based

costing has an impact on innovativeness, market orientation, organizational learning and

entrepreneurship. We expect a positive impact based on the paper of Henri (2006).

This relation might be influenced by one or more moderating and mediating variables. Mediating variables

will decide whether or not there is an impact between the interactive use and the organizational

capabilities.

Moderating variables, on the other hand, will have an influence on the strength and/or direction of the

relation between the interactive use of TD-ABC information and the four capabilities.

Furthermore, it is important to understand which variables might influence the interactive use.

More specifically we can ask the following question: which variables lead to the interactive use of time-

driven ABC? These variables are called “antecedent variables”.

Figure 4 gives an overview of the theoretical model used in this paper.

Figure 4: Theoretical model (own work)

18

In sum, we can state the following general research question:

“Is there an impact of the interactive use of TD-ABC information on market orientation, organizational

learning, entrepreneurship and innovativeness?”

Next, we translate this general research question into the following specific research questions:

1) What is meant by the interactive use of TD-ABC information?

2) Which variables lead to the interactive use of TD-ABC information?

3) What is meant by market orientation, organizational learning, entrepreneurship and

innovativeness?

4) Which variables ensure an impact of the interactive use of TD-ABC information on the four

organizational capabilities?

5) Which variables have an influence on the strength and/or direction of the impact of interactive use

of TD-ABC information on organizational capabilities?

To get an answer to these questions, we investigate the case of TD-ABC in two companies, Wymar

International and PB Gelatins. The following section provides more information on case studies as a

research method and on the two companies examined.

19

2. METHODOLOGY

In chapter two, we cover the methodology used in this paper. We start with an introduction on case study

research, the method used in this paper.

Afterwards, we give a brief overview of the two companies examined.

2.1 CASE STUDY RESEARCH

The research method used in this paper is the case study. “The case study is a research strategy which

focuses on understanding the dynamics presented within single settings. Case studies can be used to

accomplish various aims: to provide description, test theory or generate theory” (Eisenhardt, 1989).

The case study is an exploratory research method used to scout out the terrain. In case studies, one

problem is treated in depth by means of different sources of evidence. The reality is described as precise

as possible, which gives the method a great internal validity (De Pelsmacker and Van Kenhove, 2006).

According to Yin (2008), case studies can be defined as follows:

i. “A case study is an empirical inquiry that

investigates a contemporary phenomenon in depth and within its real-life context,

especially when

the boundaries between phenomenon and context are not clearly evident

ii. The case study inquiry

copes with the technically distinctive situation in which there will be many more variables

of interest than data points, and as one result

relies on multiple sources of evidence, with data needing to converge in a triangulating

fashion, and as another result

benefits from the prior development of theoretical propositions to guide data collection

and analysis”.

Case studies are the preferred strategy when “how” and “why” questions are being posed, in examining

contemporary events and when the relevant behaviours cannot be manipulated. The case study‟s unique

strength is the ability to deal with a variety of evidence such as documents, archival records, interviews,

physical artefacts and observations. This evidence might be qualitative (e.g. words), quantitative (e.g.

numbers) or both.

2.1.1 Difficulties

A lot of prejudices against the case study research exists (Yin, 2008).

The first concern is the lack of rigor. Too many times, the investigator did not follow systematic

procedures, allowed equivocal evidence or biased views to influence the direction of the findings and

20

conclusions. Yin provides ways in order to achieve a more systematic design and unbiased conclusions.

Moreover, in this paper the steps proposed by Scapens (1990) are followed. In this way, the case study

follows more systematic procedures.

A second concern is that case studies provide little basis for scientific generalization. The question is

asked whether you can generalize from a single case. The answer is that case studies are generalizable

to theoretical propositions and not to populations or universes. The case study does not present a

“sample”. The goal will be to expand and generalize theories so that they explain the observations made

(analytical generalization) and not to enumerate frequencies (statistical generalization). The researcher

will look for patterns in the case which explain the particular situation (Scapens, 1990). It is not the

objective of this paper to generalize the findings to other cases. The objective is to explain the findings of

two specific cases in order to get more insight into the subject. This is called “theory refinement”. It seeks

to refine and operationalize a theory, in this case Henri‟s (2006). It „takes the theory into the field‟ to

assess whether the theory captures the complexity of the phenomenon.

A third concern is that case studies take too long and result in massive, unreadable documents. This

concern might be appropriate, but the book from Yin (2008) provides alternative ways of doing case

studies to oppose this concern. This paper only contains the documents necessary to understand the

cases.

2.1.2 High-quality case studies

3.1.1

In order to obtain high-quality case studies, three principles are extremely important (Yin, 2008):

a) use multiple, not just single, sources of evidence

b) create a case study database

c) maintain a chain of evidence

First of all, a major strength of case study data collection is the opportunity to use many different sources

of evidence. It allows an investigator to address a broader range of historical and behavioural issues. The

most important advantage, however, is the development of converging lines of inquiry, a process of

triangulation and corroboration. A case study based on several different sources of information is likely to

be more convincing and accurate. In this paper, we use interviews and documentation obtained at the

companies.

The second principle has to do with the way of organizing and documenting the data collected for case

studies. “Too often, the case study data are synonymous with the narrative presented in the case study

report and a critical reader has no recourse if he or she wants to inspect the raw data that led to the case

study‟s conclusions” (Yin, 2008).

21

A case study database should consist of four components (Yin, 2008):

a) case study notes: these notes take a variety of forms (result of interviews, observations,

handwritten, typed …). These notes must be stored in such a way that other persons can retrieve

them efficiently at some later date

b) case study documents: information gathered from the research site …

c) tabular materials: surveys, quantitative data …

d) narratives: may be considered a part of the database and not part of the final case study report.

These narratives include the open-ended answers to questions asked.

All the documentation obtained for this paper, is organized by company.

The third principle increases the reliability of the information in a case study. “The principle is to allow an

external observer to follow the derivation of any evidence from initial research questions to ultimate case

study conclusions. This observer should be able to trace the steps in either direction (from conclusions to

research questions or from questions to conclusions)” (Yin, 2008).

All data obtained at the companies was organized and is available for further reading.

Case studies are being increasingly being used as a research method for studying management

accounting practice. The case study research can be used to provide greater understanding of how

management accounting actually functions in organizations (Keating, 1995). “Case studies offer the

possibility of understanding the nature of management accounting in practice, both in terms of

techniques, procedures, systems … which are used and the way in which they are used” (Scapens,

1990). This method may be seen as a “response to the call to develop a greater understanding of how

management accounting actually functions in organizations and society” (Keating, 1995).

As for this paper, the case of TD-ABC is covered in two companies of the Tessenderlo Group, namely

Wymar International and PB Gelatins.

The objective is to understand how the interactive use of this management accounting technique can

affect the four organizational capabilities which are necessary to develop competitive advantage.

2.1.3 Process steps

Scapens sets out the main steps in a case study, which are followed in this paper.

Preparation is the first step. The researcher should review the available theories which may be relevant to

the case and if necessary, develop a checklist of things to look for in the study. Additional theory may be

introduced as the case proceeds and new theories are developed. Henry (2006) found out that the

interactive use of MCS has a positive impact on market orientation, organizational learning,

entrepreneurship and innovativeness. The objective of this study is to refine this theory to the case of TD-

ABC information.

The second step is collecting evidence. The researcher should be constantly alert for evidence relevant in

explaining the case and should allow issues and theories to emerge out of the case, rather than being

22

imposed on it. To collect evidence, an interview has been set up with Mr. Peter Bruggeman, former

controller of Wymar International and current controller at PB Gelatins. He was actively involved in the

implementation of TD-ABC at both companies. A semi-structured questionnaire was followed in order to

obtain the right data. Furthermore, we received documentation, presentations … on-site.

Assessing evidence is the next step. Case study researchers need to assess the validity of their evidence

in the context of the particular case, i.e. „contextual validity‟ and the validity of their own interpretations of

that evidence. In this case contextual validity means collecting other evidence from that source. We

received further information from Peter Bruggeman next to the answers from the interview. To assess the

validity of our own interpretation, we gave our results for control to Peter Bruggeman.

The fourth step in case study research is identifying and explaining patterns. Various themes and

patterns can emerge during the case study. It can be helpful to prepare models such as diagrams, flow

charts … In this way, the patterns suggested by these models could describe and explain the case. For

this paper, we developed a model in order to get a full view on the subject.

The next step is theory development. If existing theories conflict with the patterns observed in the case, it

will be necessary to collect evidence in order to give explanations for these conflicts. Theories can then

be extended to meet the new circumstances. It might be possible that certain “third variables” will have an

influence on the impact of TD-ABC on the four organizational capabilities. These variables will be treated

as they emerge during the case.

Finally, it is necessary to write a report which will make the case and the explanations clear to the

readers. The results of the case study will be treated in a separate section.

In the following chapter, the cases examined and the results obtained are covered

23

3. CASES AND RESULTS

TD-ABC is a system which is not yet implemented in many companies, especially not in Belgium.

However, there are some companies who in fact have implemented TD-ABC and who have seen great

results from this method. Peter Bruggeman, current plant controller at PB Gelatins, is very familiar with

the TD-ABC approach.

He has implemented the TD-ABC system successfully in Wymar International. Here, the system is used

in an interactive way. Nowadays, Peter Bruggeman is implementing the system in PB Gelatins, a

company that belongs to the same group as Wymar International.

The data which can be found in the following sections are obtained via interviews with Peter Bruggeman

and additional on-site information.

This chapter is structured as follows. We start with a within-case analysis of Wymar International and PB

Gelatins. First of all, we give a short introduction of the company. Next, we give more information on the

interactive use of TD-ABC. Finally, we discuss the impact of the interactive use on the organizational

capabilities.

3.1 WYMAR INTERNATIONAL

3.1.1 Company introduction

Wymar International was founded by Carlos Wybo in 1952. The company is active in the development,

production and commercialisation of PVC-profiles for windows and doors.

In 1995, Wymar International was acquired by Tessenderlo Group, an international chemical group with

over 100 establishments in 21 countries.

The Tessenderlo group consists of three business groups: chemicals, specialities and plastics converting.

Wymar International was added to the plastics converting group.

This division is further divided into compounds, profiles and plastic pipe systems. Wymar is part of the

profiles unit.

This acquisition of Wymar International by Tessenderlo Group has been very successful as fast growth

and high profitability emerged in this division. In the Benelux and France, Wymar International is one of

the leading companies in the sector.

In spite of increasing complexity and geographical dispersion of the company, Wymar International has

been able to maintain the turnover per FTE (Full Time Equivalent) at a high level due to focussed

automation and continuous improvements (Kaizen).

24

3.1.2 Time-driven activity based costing project2

The calculation of costs has become a complex matter. It‟s not sufficient to know the cost and profitability

of the different products. The cost system must be able to calculate the costs of the goods produced, but

also the costs of customers and other cost objects. Many companies now use the costing module from

the ERP-system.

In 2002, SAP was implemented in Wymar International. They used the costing module of SAP to

calculate costs. Initially, only the basic functionalities were used. As a result the added value of the

system was rather low. Moreover, there wasn‟t any experience with SAP to bring the system to a higher

level.

Mid 2002 they decided to change the configuration drastically and to use the offered functionalities and

added values optimally. The whole flow was reviewed and the cycles were completed by the introduction

of product costs, the monitoring of production based on standard costs with corresponding variances

reporting and a complete analytical preparation.

For direct production costs, standards were set for the Bill of Material (on basis of standard consumption)

and for the routing components (on basis of practical capacity). Indirect costs were assigned to the

different cost objects via a surcharge per machine hour, direct labour hour or a percentage.

The deviations between actual and standard costs, which are called variances, were reported monthly by

means of a variance analysis for all cost components.

The cost module generated a contribution per product and per customer but the costs of logistics were

not assigned to the customers. Thus, it was not possible to make a variance analysis for these costs and

to make the link with order behaviour and the resulting costs.

To assign these indirect costs to the customers and to understand the use of capacity, TD-ABC was

implemented in 2005 in the logistics department by way of supplement to the existing cost system.

Moreover, Wymar International was challenged with decreasing margins and a great diversity among

customers. Its customers diversified in size, geographically and in way of payment. As said in chapter

one, it‟s in this environment that TD-ABC can bring excellent improvements.

Two things were important when the TD-ABC model was implemented.

1) At the level of departments: generation of maximum added value with a limited controlling

function: focus, scope, realisation and replication with limited resources

2) At the level of business: accurate allocation of the logistic overhead costs to the cost centres in

order to get a better follow-up of the profitability of customers and the indirect costs that these

customers generate

The objective of Wymar was not to set up an extensive controlling function, but to create maximum added

value starting from an overhead function. The focus was on the essential processes where they tried to

work pareto-optimal. This means a continuous evaluation and trade-off between “need to have” and “nice

to have” and the consequences of these choices.

2 See: “Financial management team of the year award: candidature Wymar International”, 2006 (See annexes)

25

It was expected that time-driven ABC would permit the calculation of customer profitability, not only based

on the products that customers purchased but also taking into account the characteristics of the orders.

Next to it, time-driven ABC needed to allow an efficiency evaluation for the logistics department (i.e.

warehouse and inside commercial service). Before, this was only possible for the direct production costs.

Moreover, over or under capacity needed to be managed by means of a variance analysis. As a result,

the framework itself could be evaluated and they could get insight into the customer profitability and the

optimization of the internal processes.

The results were in line with these expectations. Wymar International was able to calculate the profitability

per customer taking into account the cost to serve. The cost of small orders, modifications, E-business

driven orders, registration, order picking … can be determined per customer or group of customers.

Wymar International is now able to predict what the impact is from the type of customer and his behaviour

(small orders, many orders …). Customers can be classified into A, B and C-customers, this is from most

profitable to less profitable customers. The company must give more attention to A-customers than to B

and C customers, in order to maximize profits.

TD-ABC has met the expectations by providing the data as was presumed for this project. Wymar

International obtained clarity on customer profitability, the impact of order behaviour of customers and the

optimisation of internal processes.

TD-ABC is now implemented across the supply chain, meaning the commercial inside service, detail

picking and bulk picking. However, due to the global financial crisis, the project is put on hold.

In figure 5, you can find the different parameters of the commercial inside services department with an

example for the time required for a specific activity.

Figure 5: Parameters inside commercial services Wymar International (Source: presentation Wymar International)

26

In figure 6, we give a P&L statement of a specific client with assigned logistic costs. This is a shining

example of how TD-ABC can provide information.

Figure 6: P&L per client (Source: presentation Wymar International)

3.1.3 Interactive use of time-driven ABC

The management was immediately convinced of the advantages TD-ABC. One of the circumstances in

which the TD-ABC system can flourish is when the system is used in an interactive way.

The management of Wymar International has supported the idea of an interactive use right from the start.

The information obtained from the TD-ABC system can be data for negotiations with suppliers and

customers, information on the variances and data for planning and budgeting.

This interactive use contains the following aspects for this case.

First of all, variances between actual and budgeted data are discussed in meetings. These meetings

between the controller and the management discuss the results from the TD-ABC system. Decisions can

then be based on these results. In those meetings, workers are not involved. This has to do with the

strategy of the company, namely “Operational excellence”. Decisions are taken at higher hierarchical

level. A controller may not talk to the workers.

Secondly, the sales department is supported. “Before, the sales department didn‟t know the exact costs

of the product. They just set the prices at a level that seemed acceptable to them”. Nowadays, the sales

department obtains more accurate costs which they can use in negotiations with customers. “When a

customer asks one or more specific products, the sales department can set more accurate prices for

these orders based on the accurate costs obtained from the TD-ABC system. They can convince

customers to pay a higher price for their order because of higher costs. Moreover, sales can ask

customers to pay quicker, they can then obtain a discount based on the time equations”.

Thirdly, in the mould department lists with the productivity of the workers are hung up. Workers can see

what work they actually achieve. If necessary, their direct superiors can intervene. This will motivate

workers to perform better.

ID 729

Benelux 0 = 1 Benelux, 0 DE

rate comm. Binnendienst 0,59

rate credit control 0,98

rate laden containers 0,56

rate chef magazijn bufferstock 0,57

ID 729

Naam klant abc

Land xyz

SalesOffice WY1

Percent Comp. avg

Omzet 864.839,46 5.000.000,00

Creditnota's -13.506,46 -200.000,00

Netto Omzet 851.333,00 100,00% 100,00% 4.800.000,00

Kostprijs -571.452,00 -67,12% -89,58% -4.300.000,00

Bruto Marge 279.881,00 32,88% 10,42% 500.000,00

Transportkost -32.989,00 -3,87% -1,04% -50.000,00

Bruto Marge na transportkost 246.892,00 29,00% 9,38% 450.000,00

Totaal activiteitskosten LOG & WAR -11.249,73 -1,32% -4,25% -204.041,77

Marge na logistieke activiteitskosten 235.642,27 27,68% 5,12% 245.958,23

27

However, the most important part of the interactive use is that the organization talks about the costs.

There are discussions, meetings … held which cover the costs of the organization. Costs are interpreted

and analyzed. If necessary, the underlying assumptions (like the parameters in the time equations) are

adapted. Moreover, for the first time ever, workers are involved. In fact, they start up the system. Workers

need to be interviewed in order to get the parameters for the model. Peter Bruggeman said that workers

really enjoy the attention from their superiors.

Due to the interactive use, the organization knows what the different divisions are actually doing. Before,

nobody knew what the results, productivity … of the different divisions were. Nowadays, people

throughout the organization talk to each other and exchange ideas and data.

Interactive use demands the frequent and regular attention from management at all levels of the

organization. The system needs thus the approval of the management. The commitment of the

management can be seen as an antecedent variable to the interactive use of TD-ABC.

Furthermore, the system needs to be approved by lower-level management and other members of the

organization. They need to feel involved so that they can support the idea of interactive use.

The TD-ABC system needs to be supported by the entire organization and especially by the central

management because they have the absolute decision power and influence. Only under these

circumstances, the TD-ABC model can be used in an interactive way. In the case of Wymar, the top

manager was progressive and keen on management control tools. He gave his full support.

3.1.4 Organizational capabilities

In this section we discuss whether there is an impact of the interactive use of TD-ABC information on

innovativeness, organizational learning, market orientation and entrepreneurship.

Moreover, we look for variables that make this impact possible. These variables are called mediator

variables. There might also be variables that have influence on the direction and/or strength of this

impact. These variables are called moderating variables.

“The interactive use of TD-ABC information reveals the times of the different processes. Everyone in the

organization can see which processes require a lot of time. The interactive use of this information leads to

communication among people in the organization. They start talking about where the problems are and

they might think of solutions to improve these time-consuming processes”. The previous quote from Peter

Bruggeman refers to process innovation. Its objective is to improve the processes in order to make the

product or service cheaper, to increase the speed of processes or to meet the preferences of the

customers. The interactive use has a positive impact on this capability because it reveals the problems

and difficulties of the processes to all people in the organization. In this way, people start thinking about

possible improvements and innovations to the processes.

28

On the other hand there is product innovation. This means changing the product itself. The following

quote from Peter Bruggeman gives an example. “Customers all have different preferences when it comes

to products. They can order different products in different packages … The time-driven ABC model gives

the right costs for these products. When these costs of the preferred goods are too high, the organization

can either reject the order or either try to change the products in order to produce at a lower cost”.

“Moreover, the products can be linked to the different customer segments (A, B or C customers). When

the costs of a product are too high, the organization can still decide to produce the product when it is an

order from an A-customer”. These customers are very important to the organization so it might be

appropriate to give these customers what they want. If the organization decides not to meet the demands

of these A-customers, they might lose these customers.

According to Peter Bruggeman, the interactive use of TD-ABC information has also an important impact

on organizational learning. “Time-driven activity based costing information enables the company to see

errors in de production processes. For instance, when tests prove that a sample is not ok, this is an

indication that there is something wrong in the production process. As a result, a lot of time is spoiled.

Improvements need to be made in order not to make the same mistakes again in the future.” Moreover,

the TD-ABC information can show where the company has spent too little time on. Processes, customers

… that should get more attention can be identified.

The interactive use of TD-ABC information has also an impact on the capability market orientation. “It‟s

not only about cost cutting, but also about being more friendly, making longer calls …

As an example, Peter Bruggeman stated the following. ”Thanks to the information obtained from the TD-

ABC system, Wymar International is able to talk about customer profitability for the first time. TD-ABC

makes it possible to segment customers into A-, B- and C- clients. Wymar will mostly target A-clients,

because these clients give them the most profit”. The TD-ABC information can show which customers

deserve more attention.

Peter Bruggeman further stated that market orientation is very important to them. “It‟s important to be

ahead of the competitors.”

Due to the interactive use of TD-ABC information, entrepreneurship is supported. “When people

throughout the organization find certain opportunities, the TD-ABC information will help to evaluate these

opportunities. The organization can see whether these opportunities are profitable or not. Moreover, they

can find out whether these opportunities contribute to the strategy of the organization”.

According to Peter Bruggeman, the development of the organizational capabilities mentioned above will

be stimulated by the attention of the management and involvement from all members of the organization.

Top management needs to direct attention to the capabilities, otherwise there cannot be an impact from

the interactive use on the organizational capabilities. Furthermore, when everyone feels involved, they will

start thinking about solutions to certain problems, they‟ll come up with some new ideas, experiences will

be exchanged, they will be more motivated …

29

Moreover, Peter Bruggeman said that when the economy is doing bad the development of the capabilities

will be supported more. Especially then, it is important to keep ahead of competitors and find

opportunities, improve processes and products …

In sum we can state that “top management attention”, “employee involvement” and “external

environment” are both mediating and moderating variables. They will decide whether there is an impact

from the interactive use on the organizational capabilities or not and they will affect the size of the impact.

The more top management attention and employee involvement, the more organizational capabilities will

be stimulated. In times of crisis, organizational capabilities will earn more attention and thus will develop

more.

3.2 PB GELATINS

3.2.1 Company introduction

PB Gelatins is a well established gelatine producer. Like Wymar International, PB Gelatins is a division of

Tessenderlo Group. It belongs to the specialties business group.

PB Gelatins produces a complete range of high quality gelatines. This gelatine can be found in candy,

make-up, yoghurt, gelatine sheets, pharmacy products … Operating from ISO (International Organization

for Standardization) certified factories, PB Gelatins produces gelatines which comply with the national

and international regulations.

PB Gelatins has a capacity of approximately 44 000 tonnes per year, split between 6 factories across the

globe, making them the world‟s third largest gelatine producer.

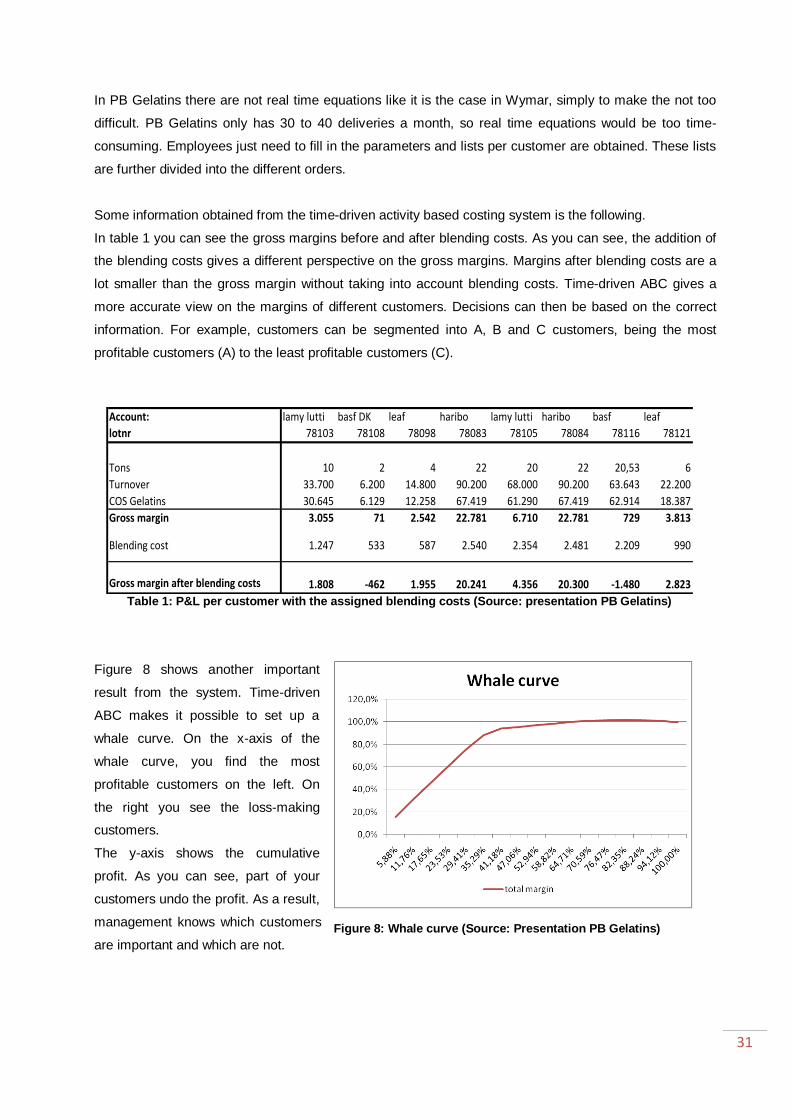

3.2.2 Time-driven activity based costing project

To understand the costs of production, PB Gelatins first used the costing module in the SAP-system like it

was the case at Wymar International.

Indirect costs were assigned to products and customers based on a volume driver. However, when they

looked at the profit and loss statement, they saw that there was no influence of volume on blending costs,

meaning that there wasn‟t an explanation for the fluctuations of these costs. At the same time competition

increased, orders became more complex and margins were decreasing. In this complex environment, PB

Gelatins wanted to get a grip on the profitability of customers, logistic processes and critical performance

indicators.

PB Gelatins implemented the TD-ABC model to understand the fluctuations in blending costs and to cope

with the increasing complexity of orders and the decreasing profit margins.

30

Moreover3, they wanted a supplement to the existing SAP-system, identify the main drivers of the

blending and the internal sales department, react quickly to changes in the market and find

supplementary indicators within the financial perspective of the balanced scorecard.

A model has been made for the blending department and the Sales department. However, this model is

not yet implemented as a daily working tool. It is used in a diagnostic manner.

In January 2009, a pilot of the time-driven ABC model was implemented. The implementation of this pilot

case took the following steps:

1) Employees of the blending department and the internal sales department were interviewed. More

specifically, the key persons per activity were interviewed for approximately 1h30 per interview.

2) Information was analysed: data were processed. Moreover, they looked at the availability of data

in the SAP-system.

3) Development of a model: parameters were set and time equations were built.

The following parameters were used for the time equations:

4

Figure 7: Parameters PB Gelatins (Source: presentation PB Gelatins)