Renée Chao-Béroff, PAMIGA

19

1 Impact Investing: how it really works? the case of pamiga finance s.a. (PFSA) September 2015 – Presentation at WAME Milan PFSA debt & equity impact investments for underserved rural Africa access to water & energy through microfinance

-

Upload

wame -

Category

Presentations & Public Speaking

-

view

258 -

download

0

Transcript of Renée Chao-Béroff, PAMIGA

1

Impact Investing: how it really works?

the case of pamiga finance s.a. (PFSA)

September 2015 – Presentation at WAME Milan

PFSA debt & equity impact investments

for underserved rural Africa

access to water & energy

through microfinance

2

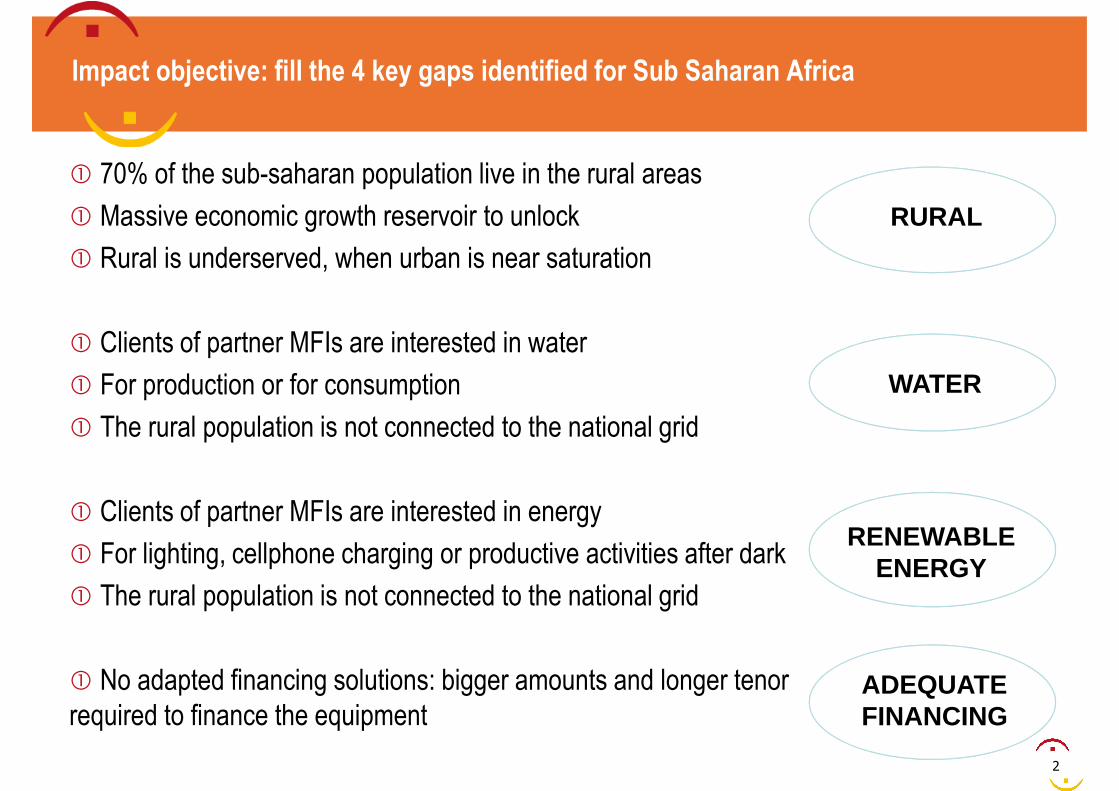

� 70% of the sub-saharan population live in the rural areas

� Massive economic growth reservoir to unlock

� Rural is underserved, when urban is near saturation

� Clients of partner MFIs are interested in water

� For production or for consumption

� The rural population is not connected to the national grid

� Clients of partner MFIs are interested in energy

� For lighting, cellphone charging or productive activities after dark

� The rural population is not connected to the national grid

� No adapted financing solutions: bigger amounts and longer tenor

required to finance the equipment

Impact objective: fill the 4 key gaps identified for Sub Saharan Africa

RURAL

WATER

RENEWABLEENERGY

ADEQUATEFINANCING

3

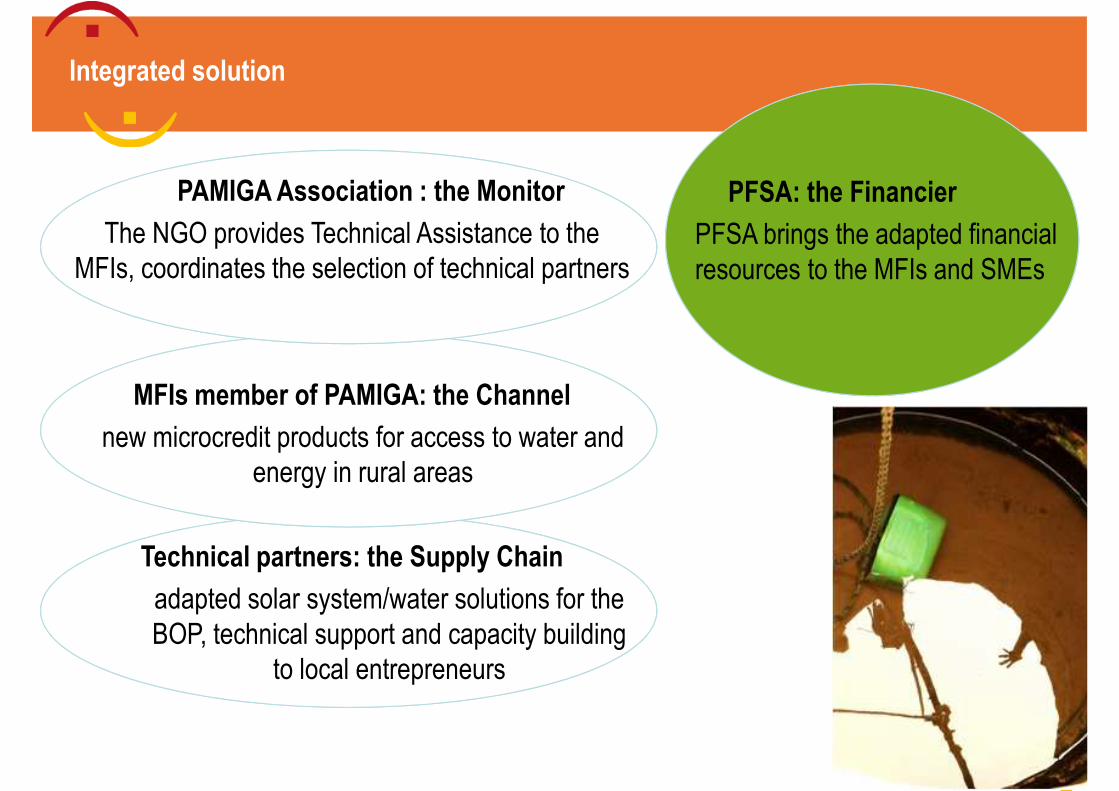

PAMIGA Association : the Monitor

The NGO provides Technical Assistance to the

MFIs, coordinates the selection of technical partners

MFIs member of PAMIGA: the Channel

new microcredit products for access to water and

energy in rural areas

Technical partners: the Supply Chain

adapted solar system/water solutions for the

BOP, technical support and capacity building

to local entrepreneurs

Integrated solution

PFSA: the Financier

PFSA brings the adapted financial

resources to the MFIs and SMEs

4

Solutions for Water

� Adduction to national grid

� Water tanks

� Motorpumps

� Wells

5

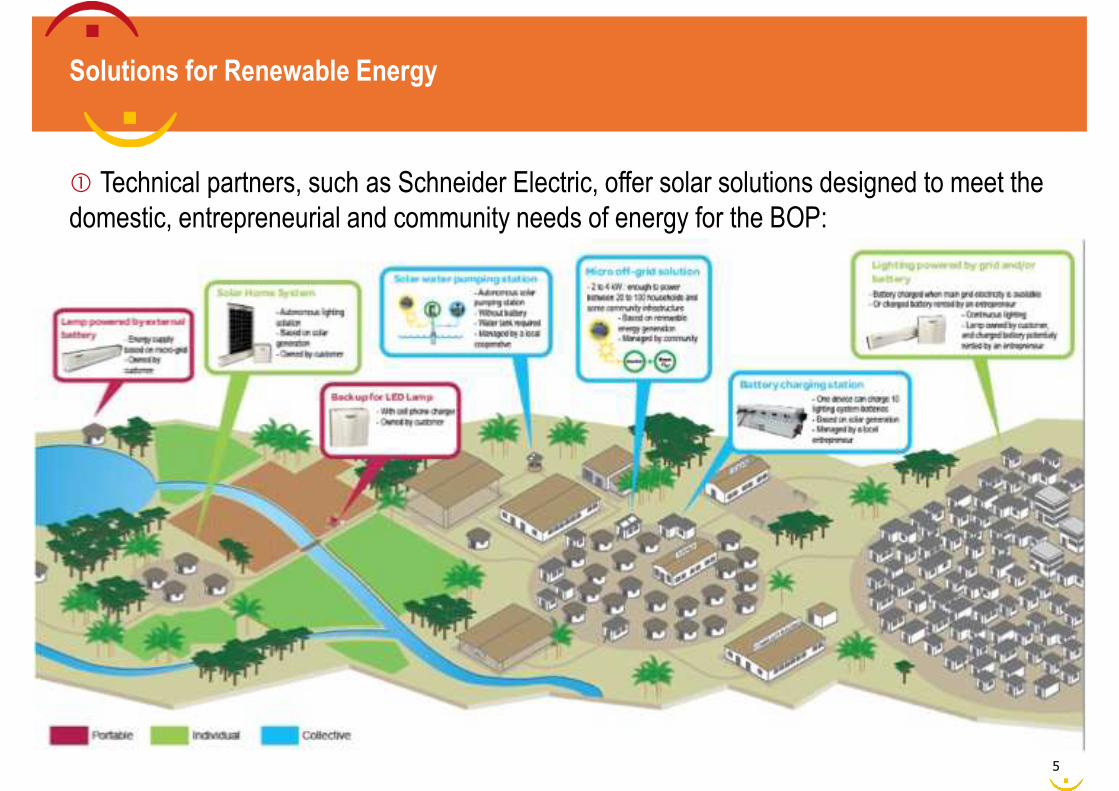

Solutions for Renewable Energy

� Technical partners, such as Schneider Electric, offer solar solutions designed to meet the

domestic, entrepreneurial and community needs of energy for the BOP:

6

PAMIGA Association (NGO)

� NGO based in Paris, Nairobi and Dakar, supporting the 16 MFI members of its network

� Technical Assistance in : Governance, Risk Management & Institutional Strengthening,

Digital Finance & MIS, New Product Development, Social performance

PAMIGA Network of MFIs

� 16 tier-2 MFIs in 10 Sub-Saharan African countries, representing more than 1.3Mio clients

� All active in the rural areas, and duly authorized and monitored by the Central banks

� Sharing values of integrity, environmental and social performance, and financial inclusion

� Strong mutual knowledge and trust based on years of close field work and co-development

Pamiga Finance S.A. (PFSA)

� The investment vehicle based in Luxembourg, controlled and owned by PAMIGA NGO

� Various compartments of investment providing long-term capital to MFIs, financial

intermediaries and SMEs

The 3 pillars of PAMIGA action

7

The financing pillar

� Pamiga Finance s.a. created 2 investment compartments for rural Africa:

� PFSA B, dedicated to rural outreach, digital finance and capital strengthening of FIs

� PFSA C, dedicated to access to water and renewable energy.

� Total funding amounts to near 20M€ in equity, subordinated and senior debt

8

Pamiga Finance S.A. investments

� Accompany the growth of partner FIs by providing them with financial resources:

▪ - mid to long term (3 to 6 years),

▪ - in local currency,

▪ - at competitive conditions

▪ - adapted to seasonality and end-beneficiaries’ constraints

� Complement their external resources and create the conditions to attract them : equity,

quasi-equity, co-financing, support for negotiation.

� Support their innovative and transformational initiatives, with high added value, for the FIs

and for their customers: new product development, project financing for MSMEs, capex

investments (digital finance, new branches,…).

9

Rural x (Water+Energy) x Adapted Finance = Impact

I m pact of the W ater & Renew able I n it iat ive

Microloans f inanced over 7 years ( M€ )nb o f

m icroloansNb in d iv

/ loanNb in d iv

im pactedof w h ic h ,

w om en

Drinking water for households 6,57 32 859 4,0 131 438 50%

Productive Water for agriculture 9,10 6 067 4,0 24 268 50%

Energy for households 8,01 53 425 4,0 213 700 50%

Energy for MSMES 4,05 1 350 1,5 2 025 10%

Energy for Villages/Communities 4,60 230 800 184 000 50%

Access to finance 21,50 107 500 4 430 000 50%

Total 5 3 ,8 4 2 0 1 4 3 1 9 8 5 4 3 1 4 9 ,9 %

Roll- over of fundsAverage outstanding amount of the Facility (M€) 9,92

Estimated amount of underwritten microloans (M€) 53,84

Corresponding roll-over multiple of average outstanding funds 5 ,4 x

10

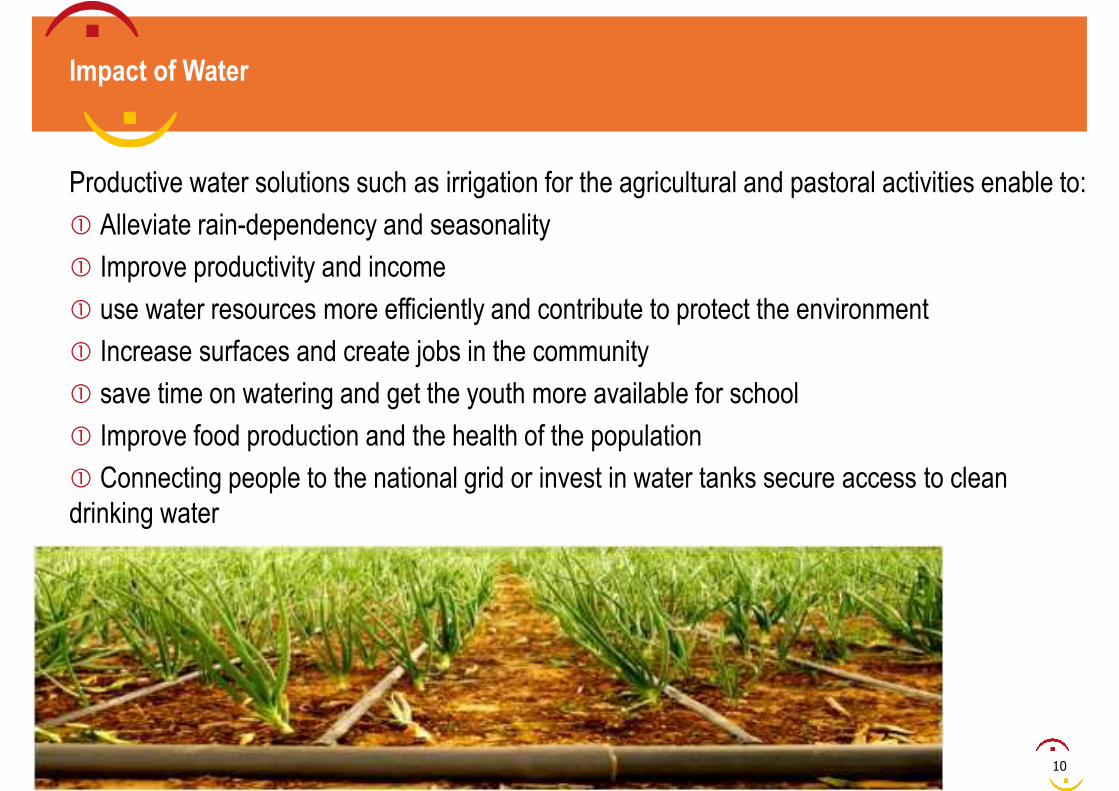

Productive water solutions such as irrigation for the agricultural and pastoral activities enable to:

� Alleviate rain-dependency and seasonality

� Improve productivity and income

� use water resources more efficiently and contribute to protect the environment

� Increase surfaces and create jobs in the community

� save time on watering and get the youth more available for school

� Improve food production and the health of the population

� Connecting people to the national grid or invest in water tanks secure access to clean

drinking water

Impact of Water

11

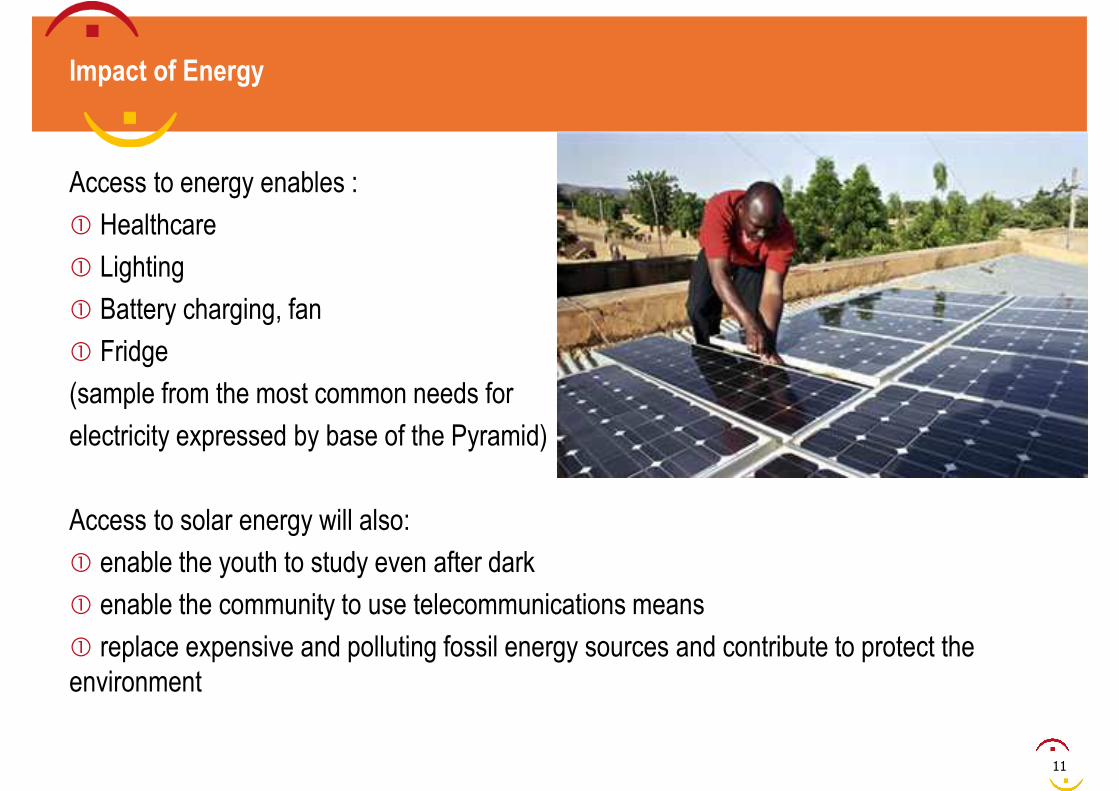

Access to energy enables :

� Healthcare

� Lighting

� Battery charging, fan

� Fridge

(sample from the most common needs for

electricity expressed by base of the Pyramid)

Access to solar energy will also:

� enable the youth to study even after dark

� enable the community to use telecommunications means

� replace expensive and polluting fossil energy sources and contribute to protect the

environment

Impact of Energy

12

� Credit conditions are fixed on a case by case basis, between each FI and PFSA.

� Amount, tenor, installments, guarantees, interest rates.

� On the basis of the demand appraisal, of the local needs, of the FI’s capacity of

absorption, of the management ambition, and of Due Diligence works led by PFSA

with the FI (economic, financial, accounting, HR, MIS, portfolio performance and

external resources)

The way PFSA works

13

Our Partners

14

Structuring of Pamiga Finance S.A.

a compartmented vehicle for impact investment

15

� Pamiga Finance S.A. is registered in Luxemburg, under Securitization Law of March, 22,

2004.

� Luxemburg is the first market place for Microfinance investment vehicles in Microfinance

and provides a privileged access to investors and to skilled and competitive service

providers.

� The Securitization Law enables the vehicle to raise capital operation per operation, under

separate compartments, with different share categories, and segregate an investment from

another.

Features of Pamiga Finance S.A. by-laws

16

� Each compartment may lend or invest independently from another compartment’s activity

� The vehicle may emit new titles at any time, without having to consult existing investors in

existing compartments, by creating a new compartment

� Each compartment has its own accounting and reporting

� Separate compartments enable to isolate risks

� There is no solidarity between compartments

Features of the compartmented structure

17

Risk mitigation

� PFSA aims at mitigating the geographical risks for each compartment

� Exchange risk may be covered by an insurance or supported by the investor, depending on

its appetite

� Financings are structured so as to match consumers’ needs and resources on a given

project, in terms of amount, tenor and seasonality in order to limit the risks

� FIs staff benefit from PAMIGA Technical Assistance to market the new products

� Disbursements are conditioned by the presentation of a corresponding authorized loan

portfolio by the FI

18

Contacts

� www.pamiga.org

� Renée Chao-Beroff, General Manager, PAMIGA

� +33 1 42 01 60 16

� Mathieu Merceret, Investment Director, Member of PFSA Board

� +33 1 42 01 60 14

� 7, rue Taylor, 75010 Paris - France

� 26-28 Rives de Clausen L-2165 Luxembourg - Grand-Duchy of Luxembourg

19

Thank you