Egypte - Amélioration du revenu et de la situation économique en ...

113

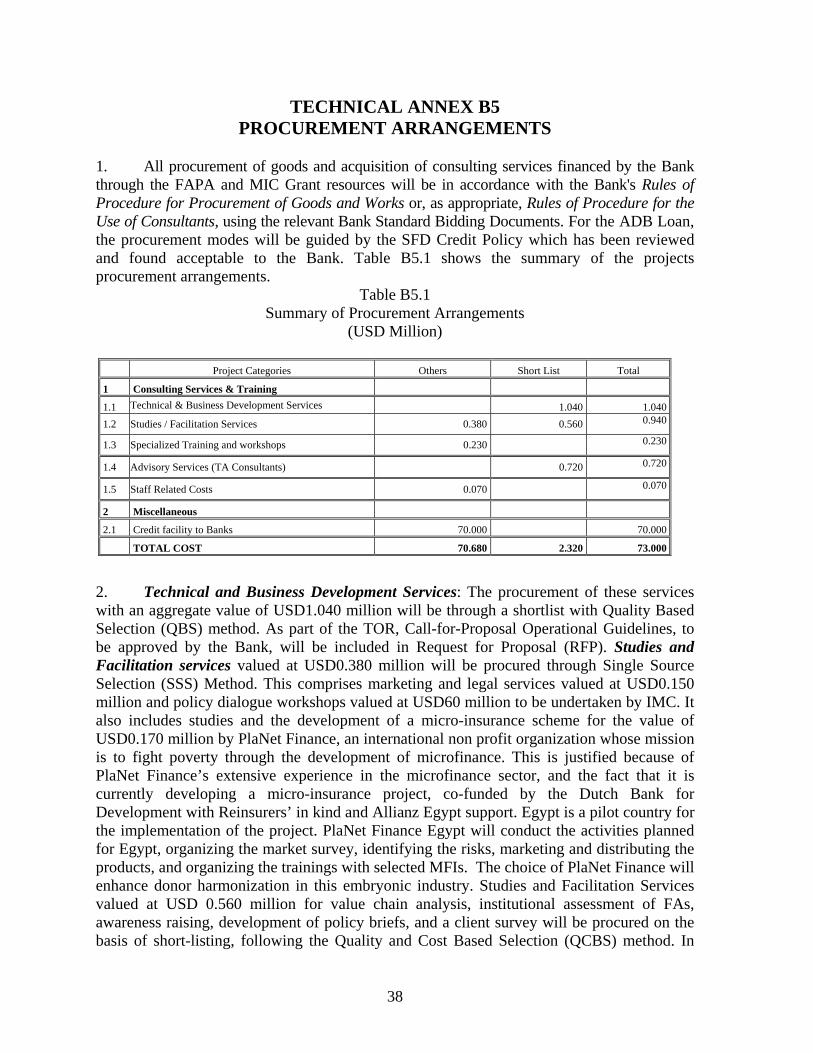

Langue : Français Original : Anglais PROJET : AMÉLIORATION DU REVENU ET DE LA SITUATION ÉCONOMIQUE EN MILIEU RURAL PAYS : ÉGYPTE RAPPORT D’ÉVALUATION DE PROJET Date : Octobre 2009 Équipe d’évaluation Chef d’équipe : Yero Baldeh, Socioéconomiste principal, OSHD.1 Membres de l’équipe : Gehane El Sokkary, Socioéconomiste, EGFO Leon Sanchez, Expert principal, Agroindustrie, OSAN.1 Robert Zegers, Chargé d’investissement supérieur, OPSM.4 Kisa Mfalila, Environnementaliste supérieure, OSAN.4 Chef de division sectoriel : Sunita Pitamber Directeur sectoriel : Tom Hurley Directeur régional : Jacob Kolster Revue par les pairs Ginnette Nzau-Muteta, Socioéconomiste en chef, OSHD.1 Moses Ayiemba, Chargé d’acquisitions supérieur, ORPF.1 Yasser Ahmad, Chargé de programme-pays principal, ORNA Ernest Tettey, Chargé d’investissement principal, OPSM.1 Ibrahim Amadou, Économiste principal, Agriculture, OSAN.1

Transcript of Egypte - Amélioration du revenu et de la situation économique en ...

Langue : Français Original : Anglais

PROJET :

AMÉLIORATION DU REVENU ET DE LA SITUATION ÉCONOMIQUE EN MILIEU RURAL

PAYS : ÉGYPTE

RAPPORT D’ÉVALUATION DE PROJET

Date : Octobre 2009

Équipe d’évaluation

Chef d’équipe : Yero Baldeh, Socioéconomiste principal, OSHD.1 Membres de l’équipe : Gehane El Sokkary, Socioéconomiste, EGFO Leon Sanchez, Expert principal, Agroindustrie, OSAN.1 Robert Zegers, Chargé d’investissement supérieur, OPSM.4 Kisa Mfalila, Environnementaliste supérieure, OSAN.4 Chef de division sectoriel : Sunita Pitamber Directeur sectoriel : Tom Hurley Directeur régional : Jacob Kolster

Revue par les pairs

Ginnette Nzau-Muteta, Socioéconomiste en chef, OSHD.1 Moses Ayiemba, Chargé d’acquisitions supérieur, ORPF.1 Yasser Ahmad, Chargé de programme-pays principal, ORNA Ernest Tettey, Chargé d’investissement principal, OPSM.1 Ibrahim Amadou, Économiste principal, Agriculture, OSAN.1

Table des matières ÉQUIVALENCES MONÉTAIRES i EXERCICE FINANCIER i POIDS ET MESURES i SIGLES ET ABRÉVIATIONS i FICHE D’INFORMATION SUR LE PRÊT iii RÉSUMÉ DU PROJET iv CADRE LOGIQUE AXÉ SUR LES RÉSULTATS vi CALENDRIER DU PROJET ix PARTIE I – DOMAINE STRATÉGIQUE ET JUSTIFICATION 1 1.1 Liens entre le projet et la stratégie et les objectifs du pays 1 1.2 Justification de la participation de la Banque 2 1.3 Coordination des donateurs 3 PARTIE II – DESCRIPTION DU PROJET 4 2.1 Objectifs en termes de développement et composantes du projet 4 2.2 Solution technique retenue et autres options explorées 5 2.3 Type de projet 5 2.4 Coût du projet et arrangements en matière de financement 6 2.5 Zone et populations cibles du projet 7 2.6 Processus participatif de conception et d’exécution du projet 7 2.7 Prise en compte, dans la conception du projet, de l’expérience acquise et des leçons apprises 8 2.7 Indicateurs de performance clés 9 PARTIE III – FAISABILITÉ DU PROJET 9 3.1 Performance économique et financière 9 3.2 Effets environnementaux et sociaux (effets environnementaux, changement climatique, genre, effets sociaux, réinstallation involontaire) 9 PARTIE IV - EXÉCUTION 12 4.1 Arrangements en matière d’exécution (arrangements institutionnels, passation de marchés, décaissement, gestion financière) 12 4.2 Suivi 14 4.3 Gouvernance 14 4.4 Viabilité 14 4.5 Gestion des risques 15 4.6 Renforcement du savoir 16 PARTIE V – INSTRUMENTS ET AUTORITÉ JURIDIQUES 17 5.1 Instruments juridiques 17 5.2 Conditions liées à l’intervention de la Banque 17 5.3 Conformité avec les politiques de la Banque 18 PARTIE VI – RECOMMANDATION 18 Appendices I. Égypte : Indicateurs socioéconomiques comparatifs 19 II. Tableau récapitulatif du portefeuille des opérations en cours de la Banque en Égypte 20 III. Égypte : Projets similaires financés par la Banque et les autres partenaires au développement 21 IV. Carte de l’Égypte montrant la zone du projet 22

Équivalences monétaires Au mois d’août 2009

1 UC = 8,66998 EGP 1 USD = 5,50 EGP 1 UC = 1,55333 USD

Exercice financier Du 1er janvier au 31 décembre

Poids et mesures 1 tonne métrique = 2204 livres 1 kilogramme (kg) = 2,200 livres 1 mètre (m) = 3,28 pieds 1 millimètre (mm) = 0,03937 pouce 1 kilomètre (km) = 0,62 mile 1 hectare (ha) = 2,471 acres

Sigles et abréviations ACDI - Agence canadienne de développement international

AERI - Projet relatif aux exportations agricoles et au revenu rural

AT - Assistance technique

BAD - Banque africaine de développement

BDS - Services de développement des entreprises

BM - Banque mondiale

CBE - Banque centrale d’Égypte

CIS - Société d’assurance de coopératives

DPG - Groupe des partenaires au développement

DSP - Document de stratégie-pays

EEAA - Agence égyptienne des affaires environnementales

EGFO - Bureau de la Banque en Égypte

FA - Association d’agriculteurs

FAD - Fonds africain de développement

FAPA - Fonds d’assistance au secteur privé africain

FISC - Coopération pour l’appui au secteur financier et à l’investissement

FSRP - Programme de réforme du secteur financier

GIRAFE - Gouvernance, information, risques, activités, financement et efficacité

GOE - Gouvernement de l’Égypte

IDH - Indice de développement humain

IFNB - Institution financière non bancaire

IFP - Intermédiaires financiers partenaires

IMC - Centre de modernisation industrielle

IMF - Institution de microfinance

JICA - Agence japonaise de développement international

ii

LDC - Ligne de crédit

MENA - Moyen-Orient et Afrique du Nord

MFCS - Secteur central de la microfinance

MPE - Micro et petite entreprise

OIT - Organisation internationale du travail

OMD - Objectif du Millénaire pour le développement

ONG - Organisation non gouvernementale

ONUDI - Organisation des Nations Unies pour le développement industriel

OSS - Guichet unique

PBDAC - Principal Bank for Development and Agricultural Credit

PIB - Produit intérieur brut

PME - Petite et moyenne entreprise

PMR - Pays membre régional

PNB - Produit national brut

PNUD - Programme des Nations Unies pour le développement

PRI - Pays à revenu intermédiaire

RAP - Rapport d’achèvement de projet

RIEE - Projet d’amélioration du revenu et de la situation économique en milieu rural

SEDO - Organisation pour le développement des petites entreprises

S&E - Suivi et évaluation

SFD - Fonds social pour le développement

SIG - Système d’information de gestion

TRE - Taux de rentabilité économique

TRF - Taux de rentabilité financière

UE - Union européenne

USAID - Agence des États-Unis pour le développement international

USD - Dollar des États-Unis

iii

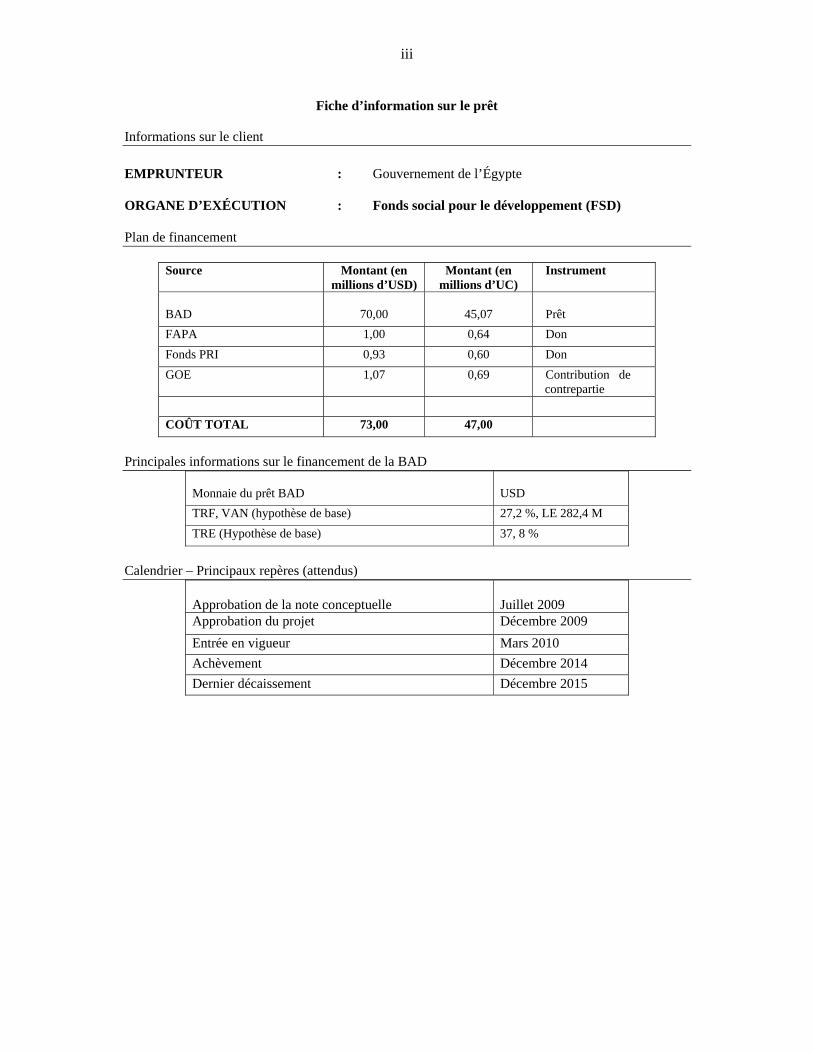

Fiche d’information sur le prêt

Informations sur le client EMPRUNTEUR : Gouvernement de l’Égypte ORGANE D’EXÉCUTION : Fonds social pour le développement (FSD) Plan de financement

Source Montant (en millions d’USD)

Montant (en millions d’UC)

Instrument

BAD

70,00

45,07

Prêt

FAPA 1,00 0,64 Don Fonds PRI 0,93 0,60 Don GOE 1,07 0,69 Contribution de

contrepartie COÛT TOTAL 73,00 47,00

Principales informations sur le financement de la BAD

Monnaie du prêt BAD

USD

TRF, VAN (hypothèse de base) 27,2 %, LE 282,4 M TRE (Hypothèse de base) 37, 8 %

Calendrier – Principaux repères (attendus)

Approbation de la note conceptuelle

Juillet 2009

Approbation du projet Décembre 2009 Entrée en vigueur Mars 2010 Achèvement Décembre 2014 Dernier décaissement Décembre 2015

iv

Résumé du projet Aperçu général du projet : Le projet a pour objectif d’améliorer la situation socioéconomique des petits exploitants agricoles ruraux pratiquant des activités économiques telles que la production, la transformation et la commercialisation de produits agricoles sélectionnés. Il ciblera essentiellement les personnes pauvres, mais économiquement actives. Au titre de ce projet, dont le coût total est de 73 millions d’USD et la durée de cinq ans, des financements seront fournis au moins à 4 800 petites entreprises agroindustrielles et à 20 000 microentreprises, ce qui permettra de créer plus de 60 500 emplois au cours de la période de cinq ans couverte par le projet. À cette fin, le projet mettra à disposition une ligne de crédit de 70 millions d’USD et complètera celle-ci par un programme d’assistance technique d’une valeur de 3 millions d’USD pour le financement des éléments suivants : i) l’analyse participative des chaînes de valeurs de l’horticulture et de la laiterie ; ii) l’établissement de relations d’affaires entre les associations d’agriculteurs et les entreprises agro-industrielles du secteur privé dans la chaîne de valeur, grâce à l’amélioration de l’information concernant les possibilités offertes sur le marché, la valeur ajoutée (transformation), le perfectionnement des compétences entrepreneuriales et opérationnelles, et la promotion de relations commerciales fiables ; et iii) le renforcement des capacités des intermédiaires financiers dans la mise au point et l’adoption d’instruments nouveaux et innovants pour le financement des entreprises agro-industrielles. Participation des bénéficiaires : Le projet adoptera une approche centrée sur le secteur privé pour la prestation de services, afin de faciliter la formation d’alliances opérationnelles productives entre les petits exploitants agricoles et les opérateurs des exploitations agricoles commerciales et les acteurs du secteur privé. La cartographie et l’analyse de la chaîne de valeur se feront d’une manière participative pour s’assurer que tous les acteurs de la chaîne de valeur contribuent à l’indentification des contraintes à surmonter et des possibilités à saisir, ainsi qu’à la préparation des plans d’activités. Justification et nécessité du projet : Le Plan national de développement de l’Égypte pour la période 2007-2012 prévoit la création de quelque 750 000 nouveaux emplois chaque année pour faire face aux nouvelles arrivées sur le marché de l’emploi ; réduire le taux de chômage actuel qui est d’environ 8,4 %, pour le ramener à 5,5 % ; et réduire le taux de pauvreté pour qu’il tombe de 20 % à 15 % d’ici 2012. Il prévoit également : i) la promotion de l’investissement dans l’agriculture, comme moyen de stimuler le développement du secteur privé dans les économies rurales ; ii) l’amélioration du revenu des citoyens démunis ; et iii) l’amélioration du niveau de vie des citoyens, et notamment des populations vivant dans la région de la Haute-Égypte. Ces objectifs sont conformes à la stratégie à moyen terme globale de la Banque, qui préconise le développement de l’agro-industrie dans les pays membres régionaux (PMR), ainsi qu’au document de stratégie-pays (2007-2011) de la Banque pour l’Égypte, qui est axé sur : i) le développement du secteur privé ; et ii) l’appui au développement social et à la protection sociale. Le projet contribuera à la réalisation de ces objectifs, par la promotion du développement des entreprises dans la chaîne de valeur agricole et l’intégration des stratégies de réduction de la pauvreté et des inégalités dans la conception des projets. Valeur ajoutée apportée par la Banque : Le projet contribuera à combler un déficit sur le marché des services financiers, en fournissant des financements à long terme non disponibles auprès de sources commerciales à des conditions compétitives. Par ailleurs, tel que cela a été le cas pour le Projet d’appui aux micro et petites entreprises et le

v

Programme d’appui au secteur du franchisage, qui sont en cours, la Banque jouera un rôle de chef de file dans le développement du portefeuille des agro-industries du Fonds social pour le développement (SFD), en vue de stimuler la mobilisation de ressources additionnelles auprès d’autres donateurs du SFD. Gestion du savoir : Le projet visera expressément à appuyer la production du savoir et la documentation des meilleures pratiques, afin de faciliter l’apprentissage organisationnel et le partage du savoir.

vi

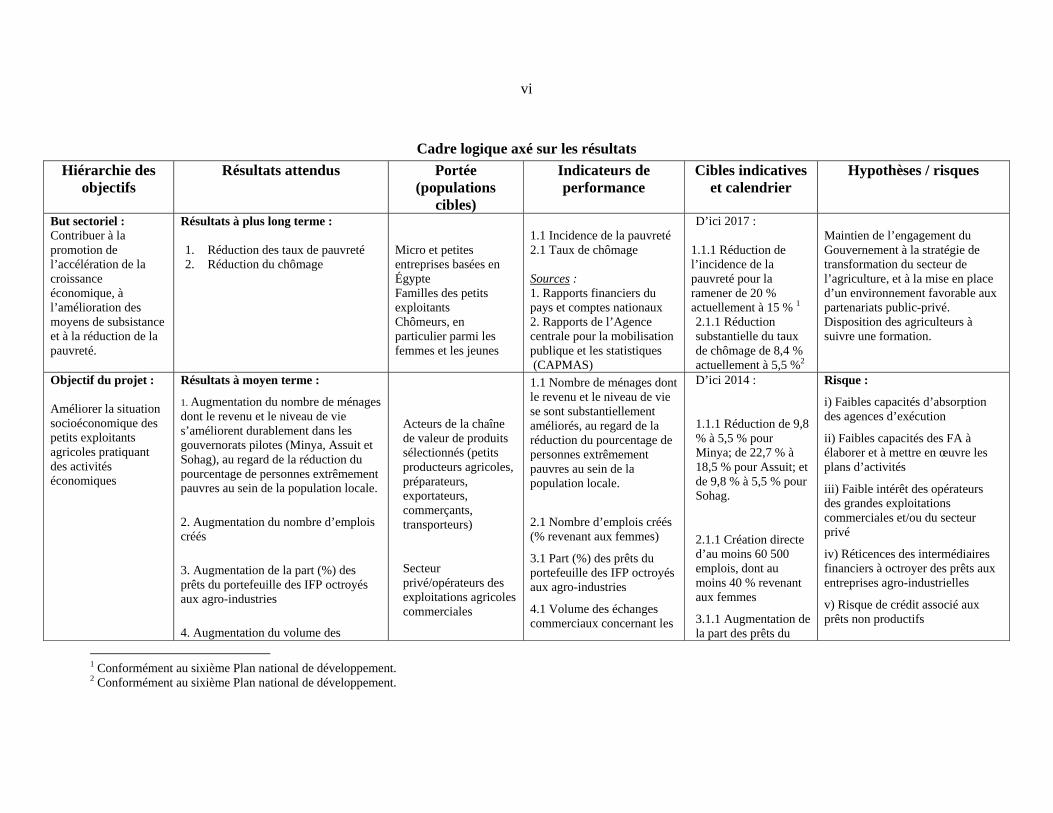

Cadre logique axé sur les résultats Hiérarchie des

objectifs Résultats attendus Portée

(populations cibles)

Indicateurs de performance

Cibles indicatives et calendrier

Hypothèses / risques

But sectoriel : Contribuer à la promotion de l’accélération de la croissance économique, à l’amélioration des moyens de subsistance et à la réduction de la pauvreté.

Résultats à plus long terme : 1. Réduction des taux de pauvreté 2. Réduction du chômage

Micro et petites entreprises basées en Égypte Familles des petits exploitants Chômeurs, en particulier parmi les femmes et les jeunes

1.1 Incidence de la pauvreté 2.1 Taux de chômage Sources : 1. Rapports financiers du pays et comptes nationaux 2. Rapports de l’Agence centrale pour la mobilisation publique et les statistiques (CAPMAS)

D’ici 2017 :

1.1.1 Réduction de l’incidence de la pauvreté pour la ramener de 20 % actuellement à 15 % 1 2.1.1 Réduction substantielle du taux de chômage de 8,4 % actuellement à 5,5 %2

Maintien de l’engagement du Gouvernement à la stratégie de transformation du secteur de l’agriculture, et à la mise en place d’un environnement favorable aux partenariats public-privé. Disposition des agriculteurs à suivre une formation.

Objectif du projet : Améliorer la situation socioéconomique des petits exploitants agricoles pratiquant des activités économiques

Résultats à moyen terme :

1. Augmentation du nombre de ménages dont le revenu et le niveau de vie s’améliorent durablement dans les gouvernorats pilotes (Minya, Assuit et Sohag), au regard de la réduction du pourcentage de personnes extrêmement pauvres au sein de la population locale. 2. Augmentation du nombre d’emplois créés 3. Augmentation de la part (%) des prêts du portefeuille des IFP octroyés aux agro-industries 4. Augmentation du volume des

Acteurs de la chaîne de valeur de produits sélectionnés (petits producteurs agricoles, préparateurs, exportateurs, commerçants, transporteurs)

Secteur privé/opérateurs des exploitations agricoles commerciales

1.1 Nombre de ménages dont le revenu et le niveau de vie se sont substantiellement améliorés, au regard de la réduction du pourcentage de personnes extrêmement pauvres au sein de la population locale.

2.1 Nombre d’emplois créés (% revenant aux femmes)

3.1 Part (%) des prêts du portefeuille des IFP octroyés aux agro-industries

4.1 Volume des échanges commerciaux concernant les

D’ici 2014 :

1.1.1 Réduction de 9,8 % à 5,5 % pour Minya; de 22,7 % à 18,5 % pour Assuit; et de 9,8 % à 5,5 % pour Sohag.

2.1.1 Création directe d’au moins 60 500 emplois, dont au moins 40 % revenant aux femmes

3.1.1 Augmentation de la part des prêts du

Risque :

i) Faibles capacités d’absorption des agences d’exécution

ii) Faibles capacités des FA à élaborer et à mettre en œuvre les plans d’activités

iii) Faible intérêt des opérateurs des grandes exploitations commerciales et/ou du secteur privé

iv) Réticences des intermédiaires financiers à octroyer des prêts aux entreprises agro-industrielles

v) Risque de crédit associé aux prêts non productifs

1 Conformément au sixième Plan national de développement. 2 Conformément au sixième Plan national de développement.

vii

Hiérarchie des objectifs

Résultats attendus Portée (populations

cibles)

Indicateurs de performance

Cibles indicatives et calendrier

Hypothèses / risques

échanges commerciaux concernant les produits prioritaires (produits horticoles et laitiers)

5. Réduction des pertes après récolte (déchets)

produits prioritaires (produits horticoles et laitiers)

5.1 Pourcentage de réduction des pertes après récolte

Sources :

a) Étude de référence

b) États financiers du SFD et rapports SIG

c) Comptes et rapports nationaux de la CBE

d) Comptes annuels du SFD

e) Rapport d’achèvement de projet

portefeuille des IFP octroyés aux agro-industries de 4,2 % à 6 %.

4.1.1 Augmentation de la valeur de la production horticole :

de 1,086 milliard d’EGP à 1,518 milliard d’EGP;

Augmentation de la valeur de la production laitière :

de 652 millions d’EGP à 1,019 milliard d’EGP.

5.1.1 Réduction des pertes après récolte de 4 % par rapport à leur niveau de référence

vi) Risque de change lié au fait que le prêt au SFD sera libellé en USD, pour rétrocession aux IFP en EGP.

Mesures d’atténuation :

i) Engager l’IMC et fournir un appui aux prestataires de services pour le renforcement des capacités

ii) Faire appel aux FA ayant le potentiel voulu et leur dispenser une formation ciblée

iii) Engager activement les opérateurs des exploitations agricoles commerciales et le secteur privé pendant toute la durée du cycle du projet (approche participative)

iv) Adopter des instruments de prêts et des arrangements de garantie innovants et attrayants (par exemple la micro-assurance)

v) Adopter des arrangements de garantie adéquats et appliquer des procédures prudentes pour les critères d’évaluation et d’éligibilité.

vi) Faire mettre en place, par le Département de la trésorerie, des procédures efficaces de gestion de la liquidité et des devises (par exemple la couverture à court terme)

viii

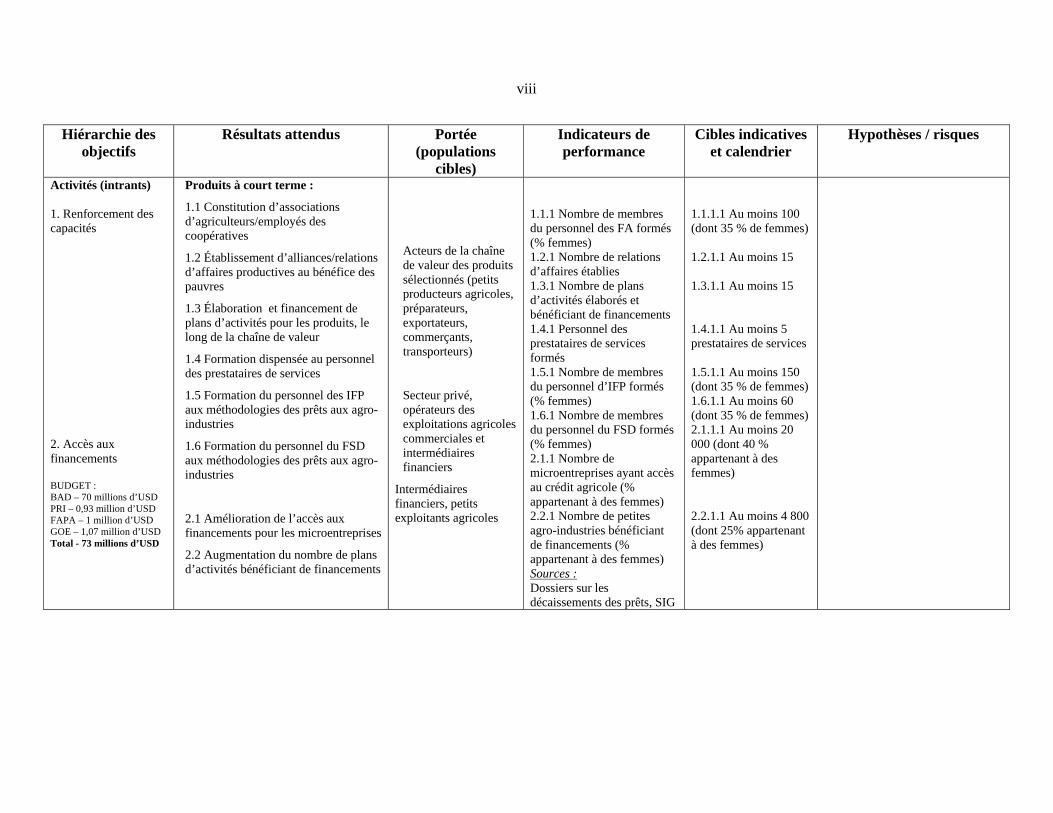

Hiérarchie des objectifs

Résultats attendus Portée (populations

cibles)

Indicateurs de performance

Cibles indicatives et calendrier

Hypothèses / risques

Activités (intrants) 1. Renforcement des capacités 2. Accès aux financements BUDGET : BAD – 70 millions d’USD PRI – 0,93 million d’USD FAPA – 1 million d’USD GOE – 1,07 million d’USD Total - 73 millions d’USD

Produits à court terme :

1.1 Constitution d’associations d’agriculteurs/employés des coopératives

1.2 Établissement d’alliances/relations d’affaires productives au bénéfice des pauvres

1.3 Élaboration et financement de plans d’activités pour les produits, le long de la chaîne de valeur

1.4 Formation dispensée au personnel des prestataires de services

1.5 Formation du personnel des IFP aux méthodologies des prêts aux agro-industries

1.6 Formation du personnel du FSD aux méthodologies des prêts aux agro-industries

2.1 Amélioration de l’accès aux financements pour les microentreprises

2.2 Augmentation du nombre de plans d’activités bénéficiant de financements

Acteurs de la chaîne de valeur des produits sélectionnés (petits producteurs agricoles, préparateurs, exportateurs, commerçants, transporteurs)

Secteur privé, opérateurs des exploitations agricoles commerciales et intermédiaires financiers

Intermédiaires financiers, petits exploitants agricoles

1.1.1 Nombre de membres du personnel des FA formés (% femmes) 1.2.1 Nombre de relations d’affaires établies 1.3.1 Nombre de plans d’activités élaborés et bénéficiant de financements 1.4.1 Personnel des prestataires de services formés 1.5.1 Nombre de membres du personnel d’IFP formés (% femmes) 1.6.1 Nombre de membres du personnel du FSD formés (% femmes) 2.1.1 Nombre de microentreprises ayant accès au crédit agricole (% appartenant à des femmes) 2.2.1 Nombre de petites agro-industries bénéficiant de financements (% appartenant à des femmes) Sources : Dossiers sur les décaissements des prêts, SIG

1.1.1.1 Au moins 100 (dont 35 % de femmes) 1.2.1.1 Au moins 15 1.3.1.1 Au moins 15 1.4.1.1 Au moins 5 prestataires de services 1.5.1.1 Au moins 150 (dont 35 % de femmes) 1.6.1.1 Au moins 60 (dont 35 % de femmes) 2.1.1.1 Au moins 20 000 (dont 40 % appartenant à des femmes) 2.2.1.1 Au moins 4 800 (dont 25% appartenant à des femmes)

ix

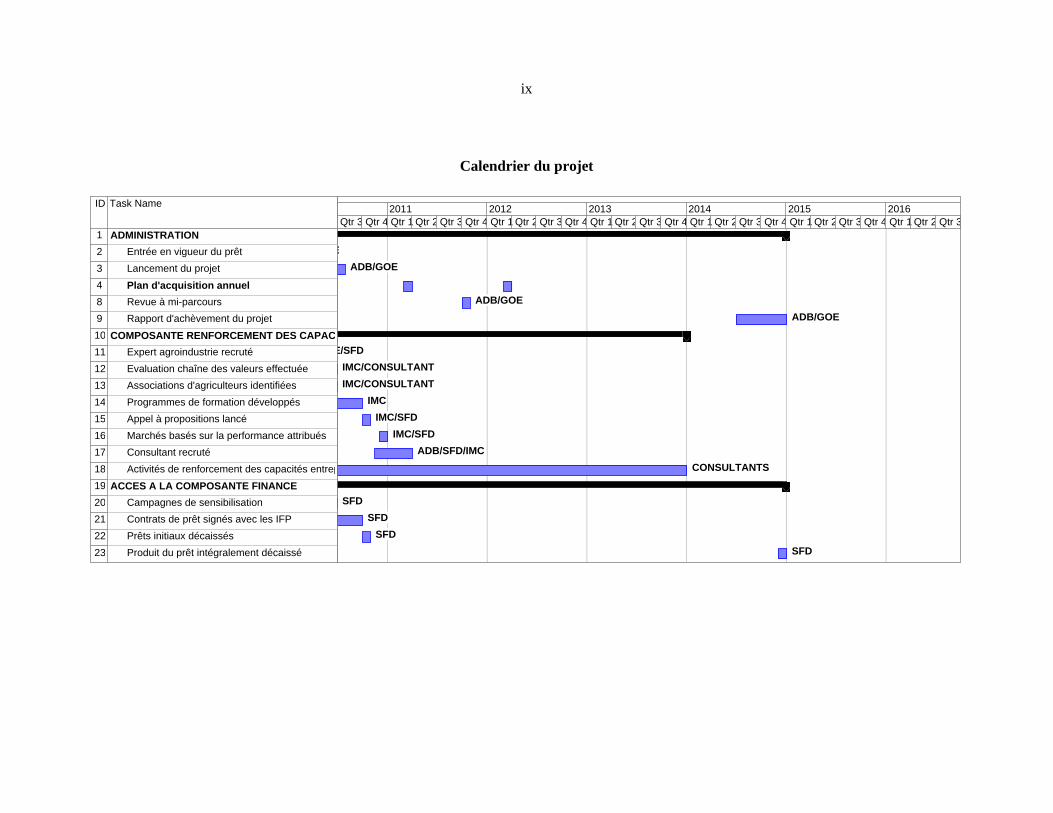

Calendrier du projet

ID Task Name

1 ADMINISTRATION2 Entrée en vigueur du prêt3 Lancement du projet 4 Plan d'acquisition annuel8 Revue à mi-parcours9 Rapport d'achèvement du projet10 COMPOSANTE RENFORCEMENT DES CAPAC11 Expert agroindustrie recruté12 Evaluation chaîne des valeurs effectuée 13 Associations d'agriculteurs identifiées14 Programmes de formation développés15 Appel à propositions lancé16 Marchés basés sur la performance attribués17 Consultant recruté18 Activités de renforcement des capacités entrep19 ACCES A LA COMPOSANTE FINANCE20 Campagnes de sensibilisation21 Contrats de prêt signés avec les IFP22 Prêts initiaux décaissés23 Produit du prêt intégralement décaissé

EADB/GOE

ADB/GOEADB/GOE

E/SFDIMC/CONSULTANTIMC/CONSULTANT

IMCIMC/SFD

IMC/SFDADB/SFD/IMC

CONSULTANTS

SFDSFD

SFDSFD

Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 32011 2012 2013 2014 2015 2016

RAPPORT ET RECOMMANDATION DU PRÉSIDENT DU GROUPE DE LA BAD AU CONSEIL D’ADMINISTRATION SUR LA PROPOSITION D’OCTROYER UN PRÊT

BAD ET D’UN DON PRI À L’ÉGYPTE POUR LE FINANCEMENT DU PROJET D’AMÉLIORATION DU REVENU ET DE LA SITUATION ÉCONOMIQUE EN MILIEU

RURAL La Direction soumet le rapport et la recommandation ci-après sur la proposition d’octroyer un prêt BAD de 70 millions d’USD et un don du Fonds fiduciaire en faveur des PRI de 930 000 USD pour le financement du Projet d’amélioration du revenu et de la situation économique en milieu rural en Égypte. I. DOMAINE STRATÉGIQUE ET JUSTIFICATION 1.1 Liens entre le projet et la stratégie et les objectifs du pays 1.1.1 Le projet est aligné sur le Plan national de développement (PND) de l’Égypte pour la période 2007-2012, qui prévoit la création de quelque 750 000 nouveaux emplois chaque année pour faire face aux nouvelles arrivées sur le marché de l’emploi et réduire le taux de chômage qui est actuellement de 8,4 % en vue de le ramener à 5,5 % d’ici la fin de la période couverte par le plan. Le développement des micro- et petites entreprises (MPE) est une stratégie cruciale pour la création d’emplois. Au regard de la stratégie nationale de développement des MPE (2009-2013), sur le nombre total de nouveaux emplois à créer chaque année, jusqu’à 450 000 devraient concerner les MPE, dont au moins 280 000 devraient résulter de l’appui du FSD. Le projet visera à contribuer à la réalisation de cet objectif stratégique en créant environ 60 500 emplois. En outre, la conception du projet a été guidée et éclairée par la Stratégie nationale pour le développement durable de l’agriculture (à l’horizon 2030), la Stratégie de transformation du secteur de l’agriculture, le Plan d’investissement dans l’agro-industrie, et l’Initiative pour la sécurité alimentaire, élaborée par le Ministère de l’Agriculture et de la Récupération des Terres, conjointement avec le Ministère du Commerce et de l’Industrie, et le Centre de modernisation industrielle (IMC). 1.1.2 Le projet est également aligné sur tous les deux piliers du document de stratégie-pays (2007-2011) de la Banque pour l’Égypte, qui sont axés sur : i) le développement du secteur privé ; et ii) l’appui au développement social et à la protection sociale. Un appui sera fourni au titre du premier pilier, par le biais de la promotion du développement de l’esprit d’entreprise dans les chaînes de valeur agricoles, tandis que le deuxième pilier bénéficiera de concours par le biais des composantes du projet relatives à la réduction de la pauvreté et des inégalités, et à la création d’emplois. Le projet est aligné sur la Stratégie du secteur privé pour l’Égypte, approuvée en 2005, qui reconnaît l’important rôle du SFD dans le développement des MPE, ainsi que la nécessité d’un appui supplémentaire de la Banque dans le domaine de la microfinance. Le projet est également conforme à la politique et à la stratégie de la Banque pour la microfinance. La conformité et l’alignement ont été garantis grâce à : i) l’application des taux d’intérêt pratiqués sur le marché ; ii) l’utilisation de mécanismes tirés par la demande ; iii) la priorité accrue accordée aux femmes ; iv) la mise en place d’un programme d’assistance technique (AT) qui est autonome, mais complémentaire au programme de crédit central ; et v) la promotion de l’établissement d’un système financier sans exclusive en Égypte, en faisant appel aussi bien aux banques qu’aux ONG comme intermédiaires, sur la base des meilleures pratiques admises au plan international.

2

1.2 Justification de la participation de la Banque 1.2.1 En 2005, l’Égypte a commencé à mettre en œuvre des réformes approfondies qui ont depuis lors fait de ce pays une des économies enregistrant la croissance la plus rapide dans la région, croissance supérieure de 1,5 point de pourcentage à celle des pays de la région du Moyen-Orient et d’Afrique du Nord (MENA), et s’établissant à 1,8 point de pourcentage pour chaque point de pourcentage de croissance du PIB mondial3. Toutefois, en dépit de cette performance exemplaire, la pauvreté et la vulnérabilité demeurent des défis majeurs en Égypte. Le caractère inégal de la croissance a eu un impact négatif sur l’élasticité de la réduction de la pauvreté, ce qui s’est traduit par l’accentuation de la pauvreté chronique et l’exacerbation des inégalités régionales. Près des trois quarts des pauvres résident dans les zones rurales et 55 % en Haute Égypte rurale. Le Gouvernement de l’Égypte (GoE) est conscient de ces défis. C’est la raison pour laquelle le PND 2007-2012 s’est fixé les objectifs suivants : i) créer chaque année 750 000 nouveaux emplois, dont 10 % dans le secteur de l’agriculture et les secteurs connexes ; ii) promouvoir l’investissement dans l’agriculture, en tant que catalyseur pour stimuler le développement du secteur privé dans les économies rurales ; iii) relever les niveaux du revenu des citoyens démunis ; iv) améliorer le niveau de vie des citoyens, et notamment des populations vivant en Haute Égypte ; et v) autonomiser les femmes sur le plan économique et créer 60 000 emplois par an pour les femmes. Ces objectifs sont conformes à la Stratégie à moyen terme de la Banque qui encourage une croissance économique durable et équitable pour favoriser la création d’emplois, par la promotion du développement de l’agroindustrie dans les zones rurales. 1.2.2 Pour réaliser ces objectifs, il est nécessaire d’adopter une approche mieux centrée sur les marchés et basant les décisions en matière de production sur les besoins des marchés, en lieu et place de l’approche habituelle axée sur la production. Toutefois, les populations rurales d’Égypte sont peu préparées aux réalités d’un monde centré sur le marché. Les petits exploitants agricoles déploient des efforts pour être compétitifs dans une situation où ils ne disposent pas de bonnes liaisons avec les marchés et où ils manquent de savoir, de compétences et de ressources financières pour participer pleinement aux transactions commerciales. En particulier, l’accès limité aux financements demeure une contrainte clé entravant le développement des économies rurales, en particulier pour les MPE engagées dans l’agroindustrie. Selon les estimations, une proportion de 5 % seulement du marché potentiel de la microfinance bénéficie actuellement de crédits, et la Banque centrale d’Égypte (CBE) signale que les prêts octroyés par les banques aux MPE demeurent limités à moins de 1 % de tous les prêts. Il est probable que la récente crise financière mondiale aggrave cette contrainte. 1.2.3 Dans ce contexte, le projet proposé s’inscrit donc dans le cadre de la réponse holistique de la Banque visant à combler le déficit sur le marché financier, à offrir aux agriculteurs pauvres des zones rurales des possibilités d’amélioration de leurs moyens de subsistance tirés de l’agriculture, et à permettre aux petits exploitants agricoles de tirer parti des marchés efficients et de la valeur ajoutée au niveau local.

3 Economist Intelligence Unit : Egypt Country Report, July 2008.

3

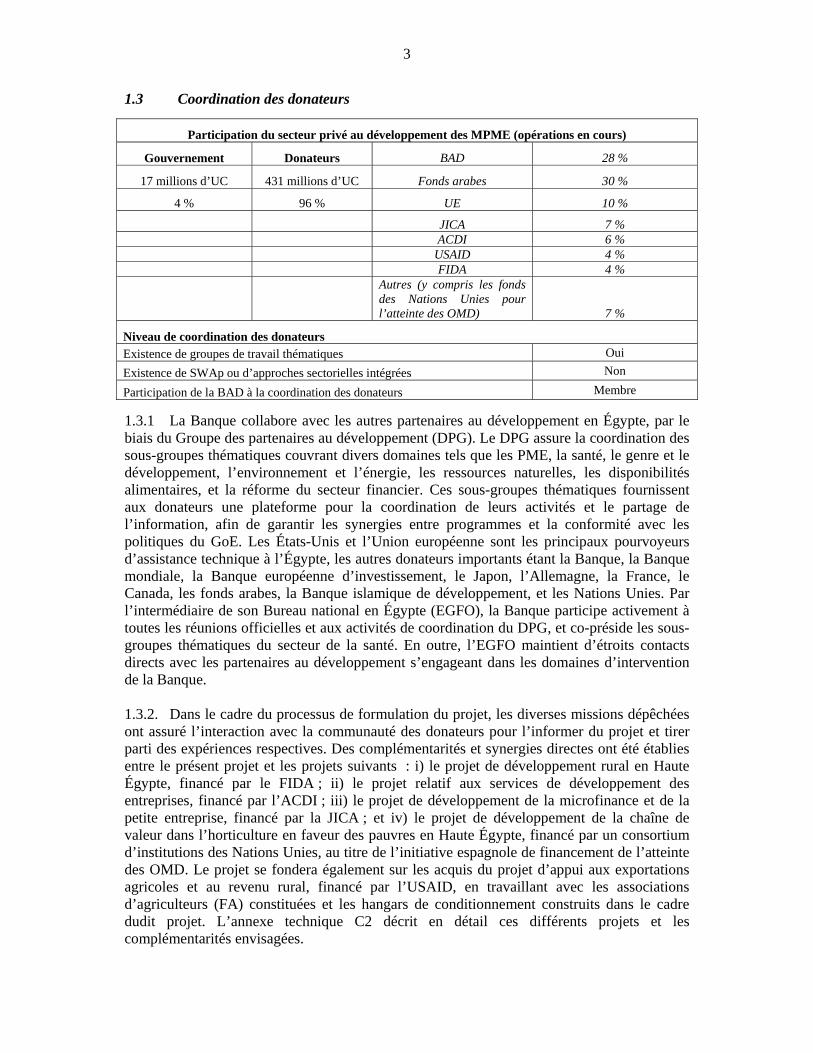

1.3 Coordination des donateurs

Participation du secteur privé au développement des MPME (opérations en cours)

Gouvernement Donateurs BAD 28 %

17 millions d’UC 431 millions d’UC Fonds arabes 30 %

4 % 96 % UE 10 %

JICA 7 % ACDI 6 % USAID 4 % FIDA 4 %

Autres (y compris les fonds des Nations Unies pour l’atteinte des OMD) 7 %

Niveau de coordination des donateurs Existence de groupes de travail thématiques Oui Existence de SWAp ou d’approches sectorielles intégrées Non

Participation de la BAD à la coordination des donateurs Membre 1.3.1 La Banque collabore avec les autres partenaires au développement en Égypte, par le biais du Groupe des partenaires au développement (DPG). Le DPG assure la coordination des sous-groupes thématiques couvrant divers domaines tels que les PME, la santé, le genre et le développement, l’environnement et l’énergie, les ressources naturelles, les disponibilités alimentaires, et la réforme du secteur financier. Ces sous-groupes thématiques fournissent aux donateurs une plateforme pour la coordination de leurs activités et le partage de l’information, afin de garantir les synergies entre programmes et la conformité avec les politiques du GoE. Les États-Unis et l’Union européenne sont les principaux pourvoyeurs d’assistance technique à l’Égypte, les autres donateurs importants étant la Banque, la Banque mondiale, la Banque européenne d’investissement, le Japon, l’Allemagne, la France, le Canada, les fonds arabes, la Banque islamique de développement, et les Nations Unies. Par l’intermédiaire de son Bureau national en Égypte (EGFO), la Banque participe activement à toutes les réunions officielles et aux activités de coordination du DPG, et co-préside les sous-groupes thématiques du secteur de la santé. En outre, l’EGFO maintient d’étroits contacts directs avec les partenaires au développement s’engageant dans les domaines d’intervention de la Banque. 1.3.2. Dans le cadre du processus de formulation du projet, les diverses missions dépêchées ont assuré l’interaction avec la communauté des donateurs pour l’informer du projet et tirer parti des expériences respectives. Des complémentarités et synergies directes ont été établies entre le présent projet et les projets suivants : i) le projet de développement rural en Haute Égypte, financé par le FIDA ; ii) le projet relatif aux services de développement des entreprises, financé par l’ACDI ; iii) le projet de développement de la microfinance et de la petite entreprise, financé par la JICA ; et iv) le projet de développement de la chaîne de valeur dans l’horticulture en faveur des pauvres en Haute Égypte, financé par un consortium d’institutions des Nations Unies, au titre de l’initiative espagnole de financement de l’atteinte des OMD. Le projet se fondera également sur les acquis du projet d’appui aux exportations agricoles et au revenu rural, financé par l’USAID, en travaillant avec les associations d’agriculteurs (FA) constituées et les hangars de conditionnement construits dans le cadre dudit projet. L’annexe technique C2 décrit en détail ces différents projets et les complémentarités envisagées.

4

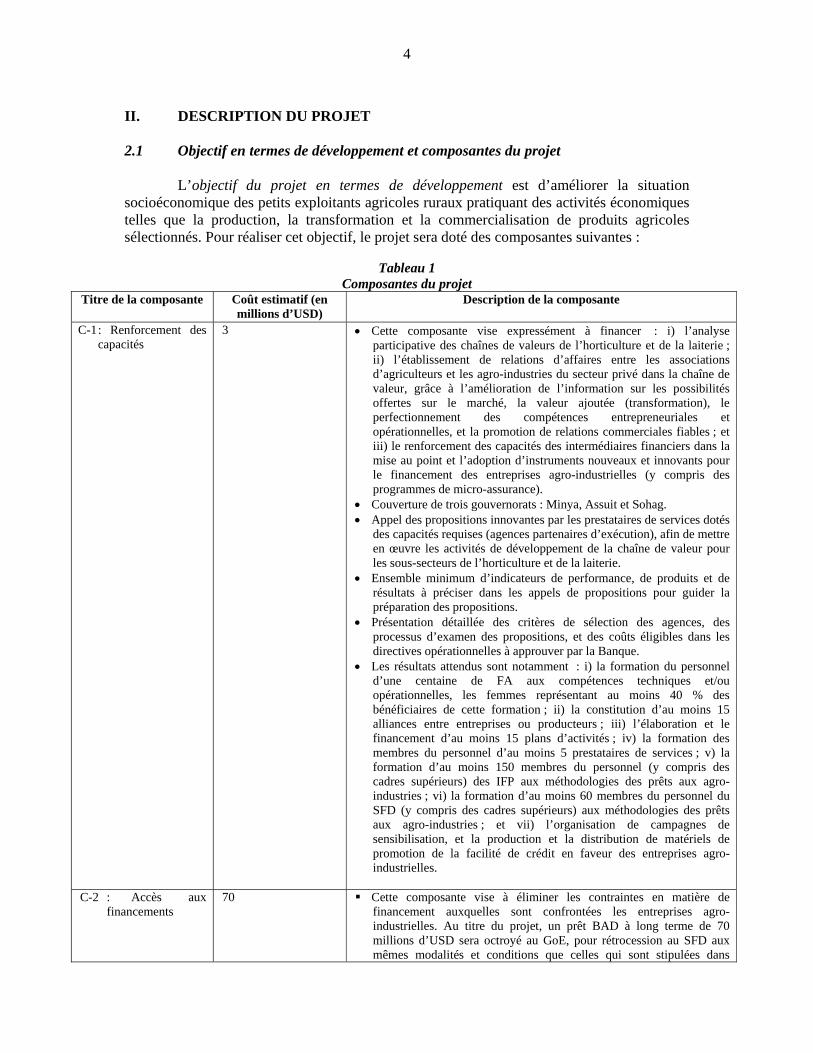

II. DESCRIPTION DU PROJET 2.1 Objectif en termes de développement et composantes du projet L’objectif du projet en termes de développement est d’améliorer la situation socioéconomique des petits exploitants agricoles ruraux pratiquant des activités économiques telles que la production, la transformation et la commercialisation de produits agricoles sélectionnés. Pour réaliser cet objectif, le projet sera doté des composantes suivantes :

Tableau 1 Composantes du projet

Titre de la composante Coût estimatif (en millions d’USD)

Description de la composante

C-1 : Renforcement des capacités

3 • Cette composante vise expressément à financer : i) l’analyse participative des chaînes de valeurs de l’horticulture et de la laiterie ; ii) l’établissement de relations d’affaires entre les associations d’agriculteurs et les agro-industries du secteur privé dans la chaîne de valeur, grâce à l’amélioration de l’information sur les possibilités offertes sur le marché, la valeur ajoutée (transformation), le perfectionnement des compétences entrepreneuriales et opérationnelles, et la promotion de relations commerciales fiables ; et iii) le renforcement des capacités des intermédiaires financiers dans la mise au point et l’adoption d’instruments nouveaux et innovants pour le financement des entreprises agro-industrielles (y compris des programmes de micro-assurance).

• Couverture de trois gouvernorats : Minya, Assuit et Sohag. • Appel des propositions innovantes par les prestataires de services dotés

des capacités requises (agences partenaires d’exécution), afin de mettre en œuvre les activités de développement de la chaîne de valeur pour les sous-secteurs de l’horticulture et de la laiterie.

• Ensemble minimum d’indicateurs de performance, de produits et de résultats à préciser dans les appels de propositions pour guider la préparation des propositions.

• Présentation détaillée des critères de sélection des agences, des processus d’examen des propositions, et des coûts éligibles dans les directives opérationnelles à approuver par la Banque.

• Les résultats attendus sont notamment : i) la formation du personnel d’une centaine de FA aux compétences techniques et/ou opérationnelles, les femmes représentant au moins 40 % des bénéficiaires de cette formation ; ii) la constitution d’au moins 15 alliances entre entreprises ou producteurs ; iii) l’élaboration et le financement d’au moins 15 plans d’activités ; iv) la formation des membres du personnel d’au moins 5 prestataires de services ; v) la formation d’au moins 150 membres du personnel (y compris des cadres supérieurs) des IFP aux méthodologies des prêts aux agro-industries ; vi) la formation d’au moins 60 membres du personnel du SFD (y compris des cadres supérieurs) aux méthodologies des prêts aux agro-industries ; et vii) l’organisation de campagnes de sensibilisation, et la production et la distribution de matériels de promotion de la facilité de crédit en faveur des entreprises agro-industrielles.

C-2 : Accès aux

financements 70 Cette composante vise à éliminer les contraintes en matière de

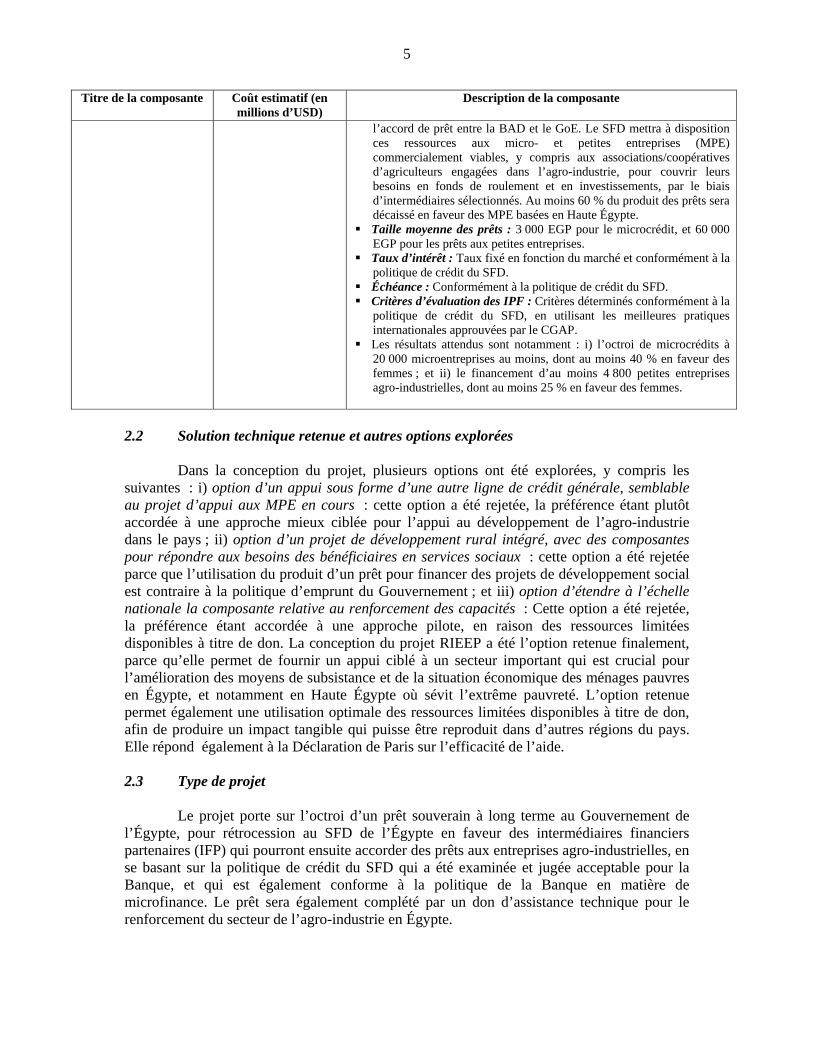

financement auxquelles sont confrontées les entreprises agro-industrielles. Au titre du projet, un prêt BAD à long terme de 70 millions d’USD sera octroyé au GoE, pour rétrocession au SFD aux mêmes modalités et conditions que celles qui sont stipulées dans

5

Titre de la composante Coût estimatif (en millions d’USD)

Description de la composante

l’accord de prêt entre la BAD et le GoE. Le SFD mettra à disposition ces ressources aux micro- et petites entreprises (MPE) commercialement viables, y compris aux associations/coopératives d’agriculteurs engagées dans l’agro-industrie, pour couvrir leurs besoins en fonds de roulement et en investissements, par le biais d’intermédiaires sélectionnés. Au moins 60 % du produit des prêts sera décaissé en faveur des MPE basées en Haute Égypte.

Taille moyenne des prêts : 3 000 EGP pour le microcrédit, et 60 000 EGP pour les prêts aux petites entreprises.

Taux d’intérêt : Taux fixé en fonction du marché et conformément à la politique de crédit du SFD.

Échéance : Conformément à la politique de crédit du SFD. Critères d’évaluation des IPF : Critères déterminés conformément à la

politique de crédit du SFD, en utilisant les meilleures pratiques internationales approuvées par le CGAP.

Les résultats attendus sont notamment : i) l’octroi de microcrédits à 20 000 microentreprises au moins, dont au moins 40 % en faveur des femmes ; et ii) le financement d’au moins 4 800 petites entreprises agro-industrielles, dont au moins 25 % en faveur des femmes.

2.2 Solution technique retenue et autres options explorées Dans la conception du projet, plusieurs options ont été explorées, y compris les suivantes : i) option d’un appui sous forme d’une autre ligne de crédit générale, semblable au projet d’appui aux MPE en cours : cette option a été rejetée, la préférence étant plutôt accordée à une approche mieux ciblée pour l’appui au développement de l’agro-industrie dans le pays ; ii) option d’un projet de développement rural intégré, avec des composantes pour répondre aux besoins des bénéficiaires en services sociaux : cette option a été rejetée parce que l’utilisation du produit d’un prêt pour financer des projets de développement social est contraire à la politique d’emprunt du Gouvernement ; et iii) option d’étendre à l’échelle nationale la composante relative au renforcement des capacités : Cette option a été rejetée, la préférence étant accordée à une approche pilote, en raison des ressources limitées disponibles à titre de don. La conception du projet RIEEP a été l’option retenue finalement, parce qu’elle permet de fournir un appui ciblé à un secteur important qui est crucial pour l’amélioration des moyens de subsistance et de la situation économique des ménages pauvres en Égypte, et notamment en Haute Égypte où sévit l’extrême pauvreté. L’option retenue permet également une utilisation optimale des ressources limitées disponibles à titre de don, afin de produire un impact tangible qui puisse être reproduit dans d’autres régions du pays. Elle répond également à la Déclaration de Paris sur l’efficacité de l’aide. 2.3 Type de projet Le projet porte sur l’octroi d’un prêt souverain à long terme au Gouvernement de l’Égypte, pour rétrocession au SFD de l’Égypte en faveur des intermédiaires financiers partenaires (IFP) qui pourront ensuite accorder des prêts aux entreprises agro-industrielles, en se basant sur la politique de crédit du SFD qui a été examinée et jugée acceptable pour la Banque, et qui est également conforme à la politique de la Banque en matière de microfinance. Le prêt sera également complété par un don d’assistance technique pour le renforcement du secteur de l’agro-industrie en Égypte.

6

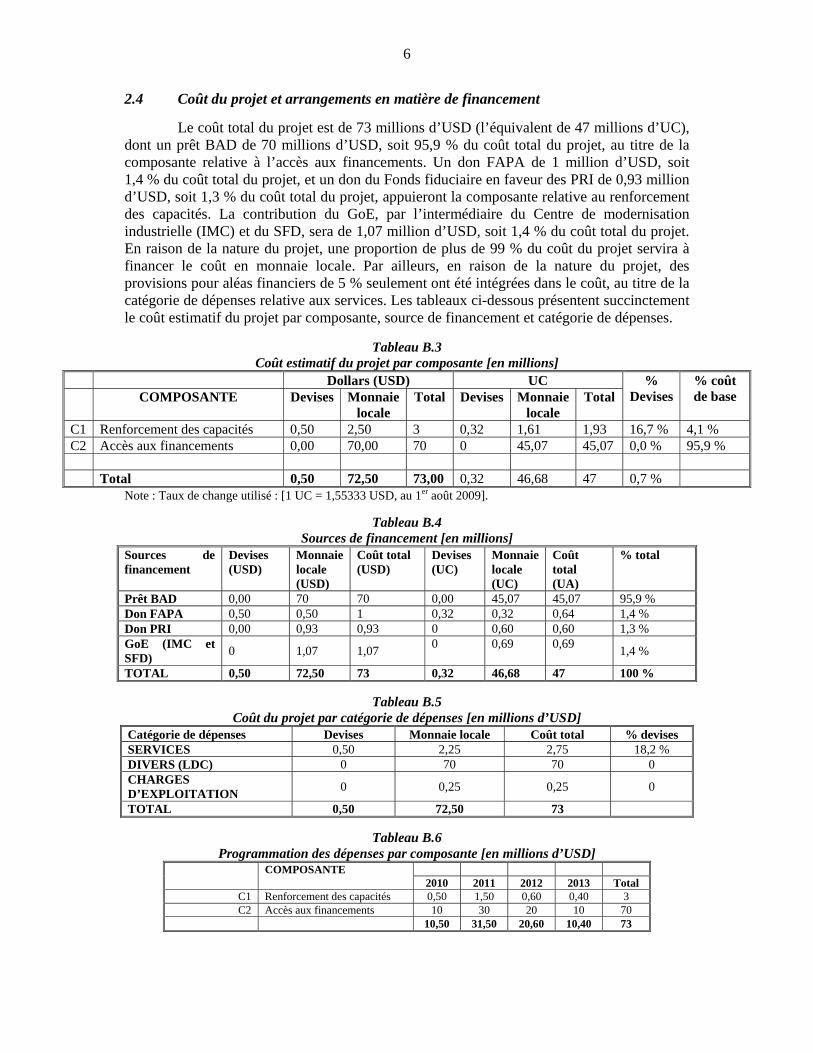

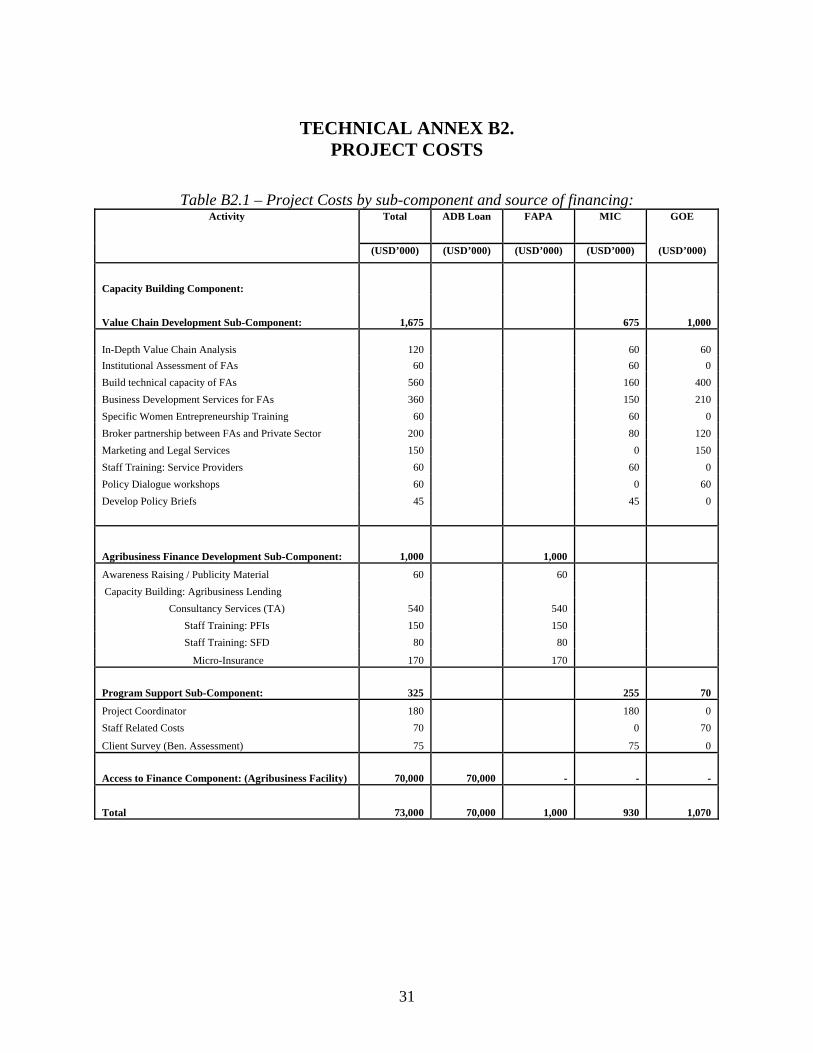

2.4 Coût du projet et arrangements en matière de financement Le coût total du projet est de 73 millions d’USD (l’équivalent de 47 millions d’UC), dont un prêt BAD de 70 millions d’USD, soit 95,9 % du coût total du projet, au titre de la composante relative à l’accès aux financements. Un don FAPA de 1 million d’USD, soit 1,4 % du coût total du projet, et un don du Fonds fiduciaire en faveur des PRI de 0,93 million d’USD, soit 1,3 % du coût total du projet, appuieront la composante relative au renforcement des capacités. La contribution du GoE, par l’intermédiaire du Centre de modernisation industrielle (IMC) et du SFD, sera de 1,07 million d’USD, soit 1,4 % du coût total du projet. En raison de la nature du projet, une proportion de plus de 99 % du coût du projet servira à financer le coût en monnaie locale. Par ailleurs, en raison de la nature du projet, des provisions pour aléas financiers de 5 % seulement ont été intégrées dans le coût, au titre de la catégorie de dépenses relative aux services. Les tableaux ci-dessous présentent succinctement le coût estimatif du projet par composante, source de financement et catégorie de dépenses.

Tableau B.3 Coût estimatif du projet par composante [en millions]

Dollars (USD) UC COMPOSANTE Devises Monnaie

locale Total Devises Monnaie

locale Total

% Devises

% coût de base

C1 Renforcement des capacités 0,50 2,50 3 0,32 1,61 1,93 16,7 % 4,1 % C2 Accès aux financements 0,00 70,00 70 0 45,07 45,07 0,0 % 95,9 % Total 0,50 72,50 73,00 0,32 46,68 47 0,7 %

Note : Taux de change utilisé : [1 UC = 1,55333 USD, au 1er août 2009].

Tableau B.4 Sources de financement [en millions]

Sources de financement

Devises (USD)

Monnaie locale (USD)

Coût total (USD)

Devises (UC)

Monnaie locale (UC)

Coût total (UA)

% total

Prêt BAD 0,00 70 70 0,00 45,07 45,07 95,9 % Don FAPA 0,50 0,50 1 0,32 0,32 0,64 1,4 % Don PRI 0,00 0,93 0,93 0 0,60 0,60 1,3 % GoE (IMC et SFD) 0 1,07 1,07 0 0,69 0,69 1,4 %

TOTAL 0,50 72,50 73 0,32 46,68 47 100 %

Tableau B.5 Coût du projet par catégorie de dépenses [en millions d’USD]

Catégorie de dépenses Devises Monnaie locale Coût total % devises SERVICES 0,50 2,25 2,75 18,2 % DIVERS (LDC) 0 70 70 0 CHARGES D’EXPLOITATION 0 0,25 0,25 0

TOTAL 0,50 72,50 73

Tableau B.6 Programmation des dépenses par composante [en millions d’USD]

COMPOSANTE 2010 2011 2012 2013 Total

C1 Renforcement des capacités 0,50 1,50 0,60 0,40 3 C2 Accès aux financements 10 30 20 10 70

10,50 31,50 20,60 10,40 73

7

2.5 Zone et populations cibles du projet 2.5.1 Le principal groupe cible du projet est celui des pauvres des zones rurales qui pratiquent des activités économiques et peuvent s’engager dans des activités opérationnelles apportant une valeur ajoutée à leurs activités commerciales au sein et hors de leurs exploitations agricoles. Dans la sélection des bénéficiaires du projet, il sera tenu compte du critère genre. 2.5.2 Le projet visera à appuyer à l’échelle nationale les activités de la chaîne de valeur de l’agro-industrie en vue d’améliorer le revenu des ménages. Selon les estimations, le projet contribuera à la création directe de quelque 60 500 emplois (dont au moins 40 % revenant aux femmes). L’analyse de la chaîne de valeur, au titre de la composante relative au renforcement des capacités, sera axée sur les produits et ciblera initialement deux sous-secteurs prometteurs pour la sécurité alimentaire et/ou les exportations, à savoir le sous-secteur de la laiterie et celui de l’horticulture. Ces sous-secteurs ont été sélectionnés pour les raisons suivantes : i) la précieuse possibilité offerte en matière de participation des petits exploitants ; ii) les faibles contraintes (en termes de compétences, de technologies et de risques) à surmonter pour entrer sur le marché de la production et de la transformation des produits ; iii) la précieuse possibilité offerte en matière de participation des femmes ; iv) la précieuse possibilité offerte en matière d’établissement de relations d’affaires le long de la chaîne de valeur ; et v) le fort potentiel d’amélioration du revenu des ménages et/ou de création d’emplois le long de la chaîne de valeur. Le projet permettra également d’appliquer la philosophie de discrimination positive en faveur de la Haute Égypte, ce qui est conforme aux orientations gouvernementales actuelles accordant la priorité à la Haute Égypte dans l’aide au développement. À cet égard, les activités de renforcement des capacités seront limitées aux gouvernorats de Minya, d’Assuit et de Sohag. Ces gouvernorats ont été sélectionnés pour les raisons suivantes : i) la prévalence et le caractère absolu de la pauvreté qui y sévit ; ii) la structure de production actuelle des produits ciblés (produits laitiers dans le gouvernorat de Minya et produits horticoles dans tous les trois gouvernorats) ; iii) le potentiel en matière de croissance économique ; iv) l’exploitation limitée des possibilités offertes dans le domaine de l’agro-industrie ; v) les possibilités de commercialisation des produits ciblés ; vi) le nombre potentiel de bénéficiaires ; vii) l’accès limité aux financements destinés à l’agriculture ; viii) les possibilités offertes en matière de participation des femmes et des jeunes ; et ix) le potentiel en matière de création d’emplois. Cette approche pilote des activités de développement de la chaîne de valeur est nécessaire, au regard des ressources limitées disponibles à titre de don et du caractère innovant du projet pour le SFD. 2.6 Processus participatif de conception et d’exécution du projet L’équipe du projet a mené de larges consultations au cours des phases de préparation et d’évaluation du projet. Elle a tenu des discussions avec des représentants du Ministère de l’Agriculture, du Ministère de l’Industrie et du Commerce, du Centre de modernisation industrielle (IMC) et du Centre de recherche agricole, ainsi qu’avec le Chef de la Chambre des industries alimentaires, le Conseil d’administration de l’Association des exportateurs de produits horticoles, le Chef de l’Union des producteurs et exportateurs de produits horticoles, les responsables des associations et coopératives d’agriculteurs, des chaînes des supermarchés, des ONG et des OBC, tout comme avec des consultants et des acteurs du secteur privé intervenant dans l’agro-industrie. L’équipe du projet a également mené des consultations avec des représentants d’institutions financières telles la Commercial

8

International Bank, la National Bank of Egypt, la Faisal Islamic Bank, la Credit Guarantee Company et plusieurs ONG intervenant dans l’intermédiation de la microfinance. Elle est parvenue à la conclusion que le projet bénéficie d’un large appui à tous les niveaux, y compris parmi les acteurs du secteur privé. Un comité consultatif national, composé de représentants des diverses parties prenantes, sera mis sur pied pour guider et orienter le projet. La cartographie et l’analyse de la chaîne de valeur seront effectuées d’une manière participative pour s’assurer que tous les acteurs de la chaîne de valeur participent activement à l’identification des contraintes à surmonter et des possibilités à saisir, ainsi qu’à la préparation des plans d’activités. Des initiatives positives seront prises pour engager les petits exploitants agricoles et les autres acteurs de la chaîne de valeur, par l’organisation de campagnes de promotion et de sensibilisation, la formation et le renforcement des capacités des FA. Dans le cadre de l’appui de la Banque visant à améliorer le cadre de suivi et d’évaluation (S&E) du SFD, au titre du projet d’appui aux MPE en cours (Voir Annexe technique A4 pour la description de ce projet), il sera fait appel à des outils de suivi communautaire participatif pour obtenir la rétroaction des bénéficiaires sur le processus d’exécution du projet et pour s’assurer que toutes les activités du projet sont mises en œuvre d’une manière satisfaisante et durable. 2.7 Prise en compte, dans la conception du projet, de l’expérience acquise et des

leçons apprises La conception du projet a été guidée par les leçons apprises au sein du SFD et en Égypte en général dans l’exécution des projets financés par la Banque, ainsi que par l’expérience acquise dans l’exécution des projets financés par d’autres donateurs. Au nombre de ces leçons, l’on pourrait citer : a) l’importance cruciale de l’assistance technique pour l’amélioration de l’impact des opérations des lignes de crédit en termes de développement ; b) l’impact accru et le meilleur rapport coût/efficacité des arrangements coordonnés/harmonisés en matière d’exécution, par rapport à l’exécution isolée de projets ; c) l’importance cruciale des mécanismes de suivi et d’évaluation tenant compte des structures et outils communautaires de gouvernance pour la responsabilisation en matière de résultats ; et d) la durabilité accrue des interventions ciblant le développement des entreprises, lorsqu’il est fait appel au secteur privé pour la prestation de services. Ces leçons ont été intégrées dans la conception du projet comme suit : a) le panachage du prêt BAD avec un don visant à couvrir les besoins du projet en assistance technique ; b) l’utilisation des cadres institutionnels du SFD et de l’IMC et la création d’un comité consultatif national qui sera chargé de la supervision générale et des orientations pour l’exécution du projet, en plus de faciliter la coordination avec les autres initiatives nationales similaires ; c) le recours aux outils de suivi communautaire et au cadre S&E pour améliorer la responsabilisation en ce qui concerne les résultats du projet ; et d) la promotion des canaux du secteur privé pour la prestation de services, afin d’approfondir le développement des entreprises et d’améliorer la réactivité à l’égard de la demande d’entreprises et la viabilité commerciale des activités du projet apportant une valeur ajoutée. Les leçons apprises de l’exécution des projets des portefeuilles de l’USAID, de l’UE et du FIDA ciblant le secteur de l’agriculture en Égypte montrent qu’il est nécessaire d’entreprendre l’analyse de toute la chaîne de valeur pour certains produits clés en vue de promouvoir la productivité et la croissance dans une économie à prédominance agricole. Le présent projet prévoit donc une analyse de la chaîne de valeur des principaux produits dans les domaines ciblés en vue de l’identification des domaines dans lesquels le projet pourrait intervenir de façon à apporter une valeur ajoutée. D’autres leçons génériques, apprises de la récente revue du portefeuille de la Banque en Égypte, ont également été prises en compte, notamment : i) la garantie d’une participation suffisante des différents acteurs à la conception du projet et la réduction à un

9

niveau minimal des conditions des prêts pour améliorer la qualité des projets à l’entrée ; ii) la conduite d’audits techniques et l’utilisation d’outils de responsabilisation communautaire pour donner des assurances sur le plan fiduciaire ; et iii) le renforcement de l’orientation vers les résultats dans les projets financés par la Banque, afin d’optimiser l’impact sur le développement. 2.8 Indicateurs de performance clés En général, le projet mettra l’accent sur les produits stratégiques suivants : i) le financement d’au moins 4 800 petites entreprises agro-industrielles et de 20 000 microentreprises, la création de plus de 60 500 emplois sur la période de cinq ans couverte par le projet ; et ii) le renforcement des capacités du SFD et de ses intermédiaires financiers partenaires dans les méthodologies des prêts aux entreprises agro-industrielles. Les résultats spécifiques attendus seront notamment : a) le nombre de ménages dont le revenu et le niveau de vie se sont durablement améliorés, au regard de la réduction du pourcentage des personnes vivant dans l’extrême pauvreté dans les gouvernorats pilotes ; b) la création d’un plus grand nombre d’emplois ; c) l’augmentation de la part du portefeuille des prêts des IFP octroyés aux entreprises ; d) l’augmentation du volume des échanges commerciaux concernant les produits ciblés (produits horticoles et laitiers) ; et e) la réduction des pertes après récolte (déchets).

III. FAISABILITÉ DU PROJET 3.1 Performance économique et financière

Tableau C.1 Principaux chiffres économiques et financiers

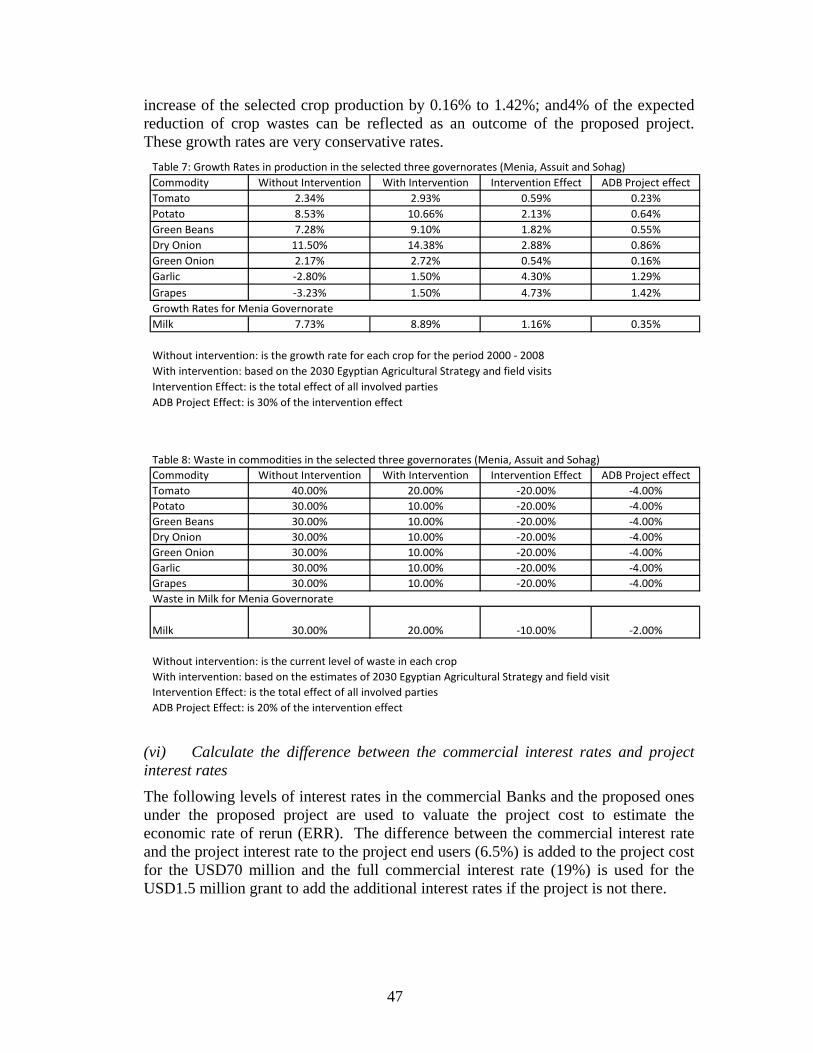

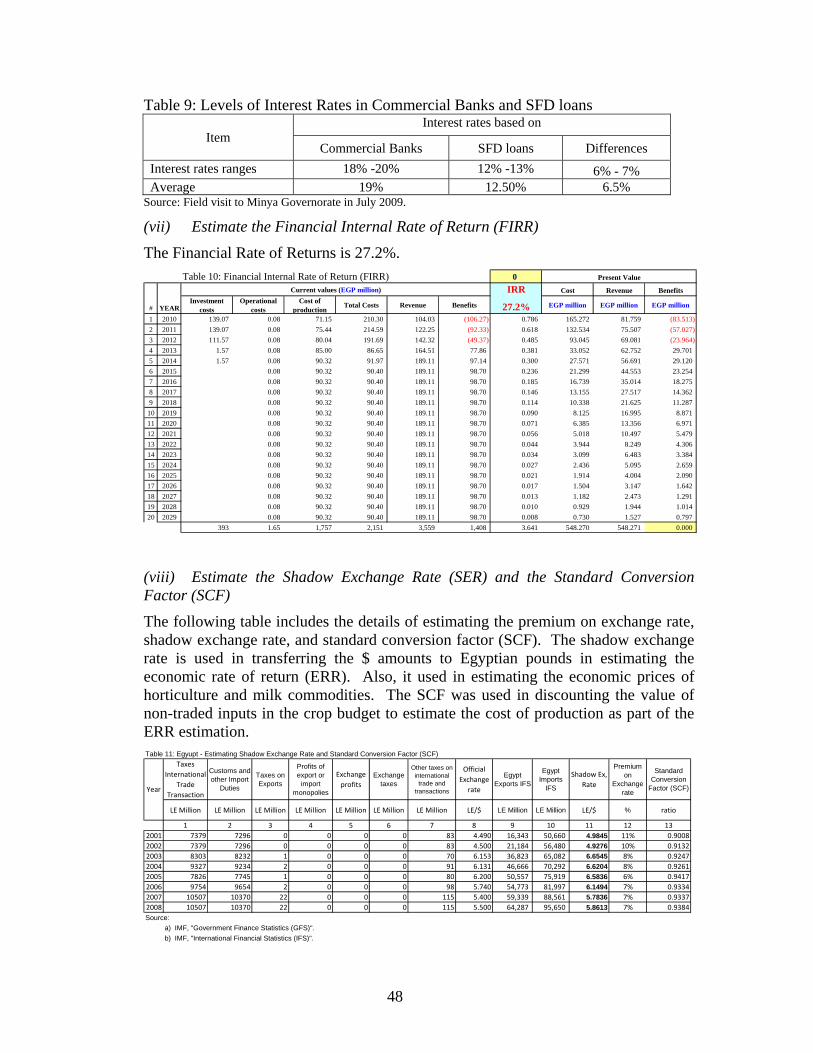

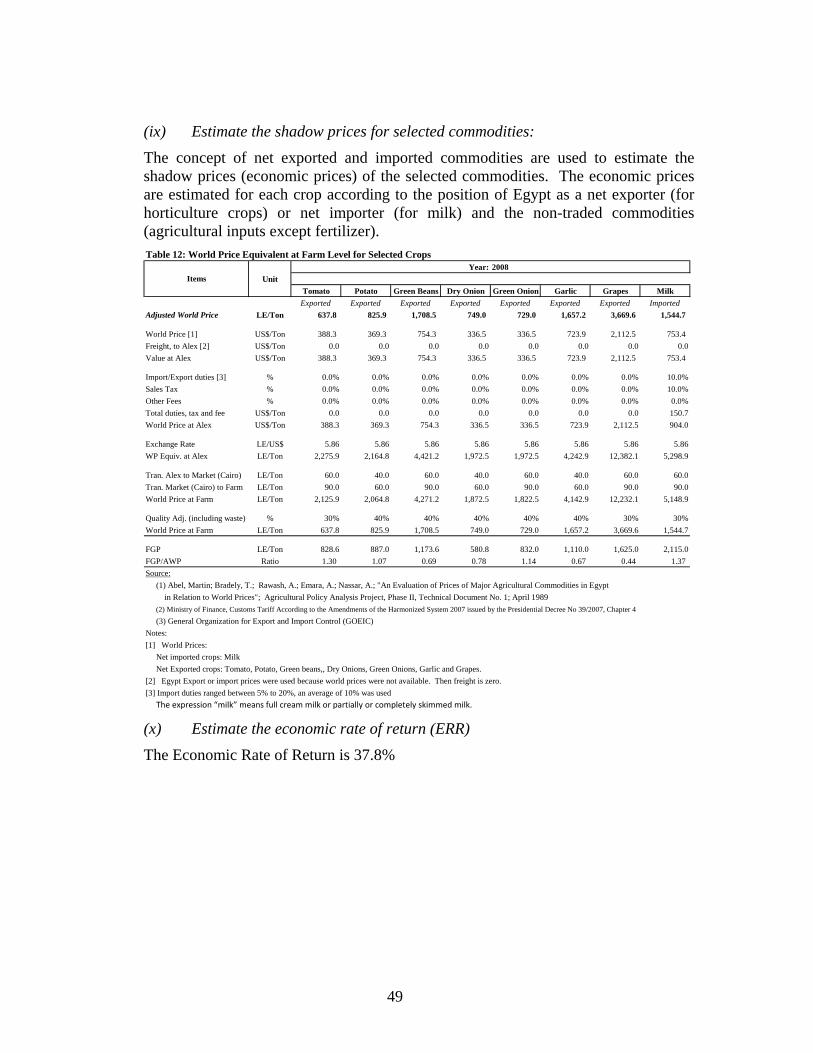

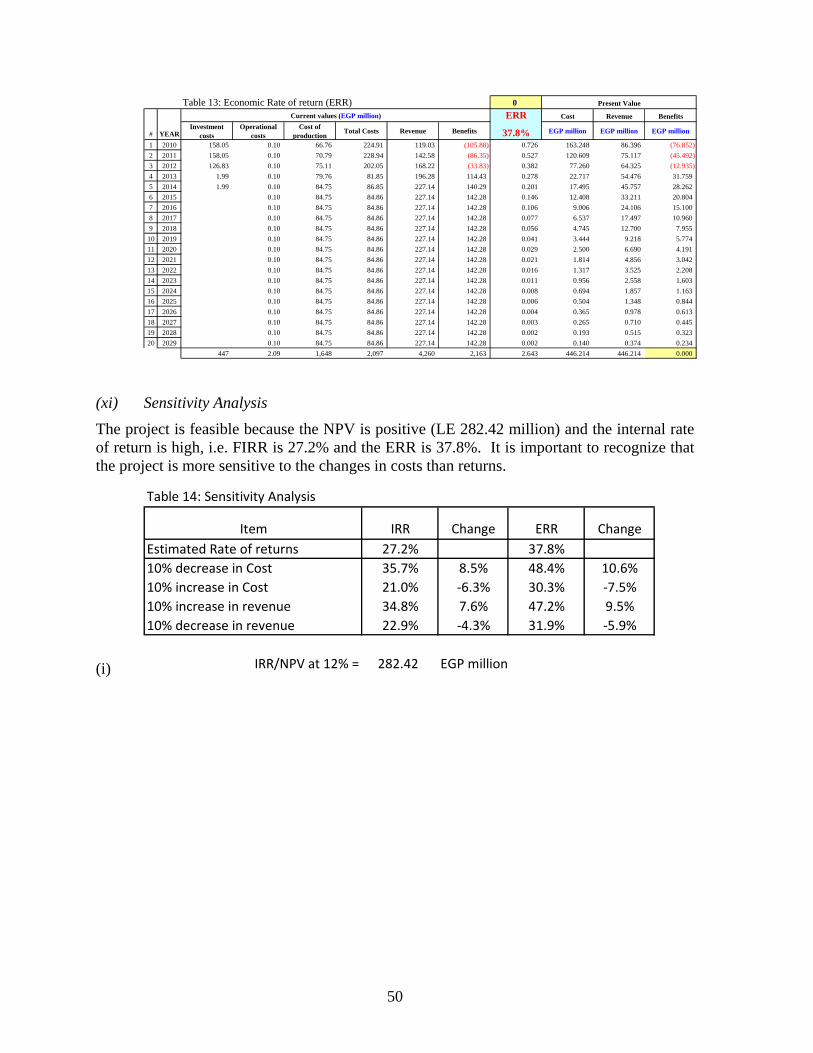

TRF, VAN (hypothèse de base) (27,2 %, soit 282,42 millions d’EGP) TRE (hypothèse de base) (37,8 %)

NB : L’annexe B6 fournit de plus amples informations sur les calculs. Le taux de rentabilité économique (TRE) global du projet est de 37,8 %, et le taux de rentabilité financière (TRF) de 27,2 %. En d’autres termes, le projet proposé est viable, tant du point de vue économique que du point de vue financier, dans la mesure où ses taux de rendement sont supérieurs au coût du capital (fixé à 12 %). L’annexe technique B7 fournit de plus amples informations sur l’analyse financière et l’analyse économique du projet. 3.2 Effets environnementaux et sociaux

Effets environnementaux 3.2.1 Conformément aux Procédures du Groupe de la Banque pour l’évaluation environnementale et sociale (ESAP), le projet est classé à la catégorie 4, du point de vue environnemental, dans la mesure où il porte sur l’investissement de fonds de la Banque par le biais d’intermédiaires financiers, pour rétrocession subséquente aux MPE. Cette catégorisation a été validée par le Département des résultats et du contrôle de la qualité (ORQR) le 15 juillet 2009. Les IFP vont octroyer des prêts aux agriculteurs, pris individuellement ou constitués en associations, et aux MPE agro-industrielles, aux fins de financement de leurs fonds de roulement et de leurs investissements. Le projet ne financera pas une infrastructure majeure, et aucune réinstallation n’est prévue au titre de la mise en œuvre des activités du projet. Toutefois, en cas d’effets environnementaux imprévus émanant des sous-projets pendant l’exécution du projet, de tels effets seront atténués et gérés conformément aux directives environnementales du SFD.

10

3.2.2 Le SFD a préparé un plan de gestion environnementale et sociale et des directives prévoyant notamment un processus adéquat d’examen et de revue pour l’évaluation des effets environnementaux et sociaux potentiels liés aux sous-projets. Ce processus déterminera les mesures de sauvegarde appropriées à appliquer et les mesures d’atténuation à mettre en œuvre pour s’attaquer à de tels effets environnementaux et sociaux potentiels. Pour les sous-projets susceptibles d’avoir des effets significatifs, des évaluations environnementales plus détaillées et plus précises seront conduites conformément à la loi égyptienne No 4 de 1994 régissant les questions environnementales et aux procédures de la Banque pour l’évaluation environnementale et sociale. La responsabilité du suivi des mesures d’atténuation pendant l’exécution du projet incombera conjointement à l’Unité du développement environnemental du SFD et à l’Agence égyptienne des affaires environnementales. En outre, le Département du développement environnemental soumettra à la Banque un rapport annuel sur la mise en œuvre de ses procédures environnementales et la performance environnementale de ses investissements financés à partir des fonds de la Banque. 3.2.3 Le projet tirera également parti de la mise en œuvre de la composante AT du Programme d’appui au secteur du franchisage financé par la Banque, qui vise à renforcer les capacités institutionnelles du SFD. Cette composante porte sur la formation d’environnementalistes et de points focaux pour assumer la responsabilité de la revue environnementale et sociale du SFD. Changement climatique 3.2.4 Il ressort des modèles du changement climatique que bien qu’il soit probable que l’Égypte soit confrontée à l’avenir aussi bien à l’augmentation des précipitations qu’à celle des températures, l’accroissement attendu des niveaux d’évapotranspiration sera compensé par l’augmentation des précipitations, et les niveaux des ruissellements resteront donc virtuellement inchangés. La rareté de l’eau est une préoccupation croissante, et le GoE encourage le recours à l’irrigation goutte-à-goutte et l’application des bonnes pratiques de gestion de l’eau. Face à la probabilité de la variabilité du climat et du changement climatique à l’avenir, le développement de l’agro-industrie contribuera à renforcer les capacités organisationnelles des agriculteurs et l’appui institutionnel aux petits exploitants agricoles, à fournir l’accès au crédit, à accroître l’efficience des marchés des échanges inter-industries, et à fournir l’accès au savoir sur l’amélioration de la gestion des terres et des systèmes agraires. Ces facteurs favoriseront le renforcement des capacités locales dans l’adaptation à la variabilité du climat à court terme et au changement climatique à long terme. Genre 3.2.5 En Égypte, l’agriculture est l’occupation principale de 83,2 % des femmes et de 43,3 % des hommes dans les zones rurales. Compte tenu de la très petite taille des propriétés foncières, les agriculteurs ont recours presque exclusivement à la main-d’œuvre familiale non rémunérée. La production vivrière des agriculteurs ruraux peut certes être relativement abondante toute l’année durant, mais leur revenu en espèces est plus modeste. C’est la raison pour laquelle bon nombre d’agriculteurs, et notamment les hommes et les membres des ménages ayant pour chef une femme, sont à la recherche d’autres emplois liés à la création d’entreprises familiales et de MPE. Les MPE rurales couvrent les besoins des communautés locales en termes de commerce et de services. La propriété et la gestion des microentreprises sont assurées dans la plupart des cas par les femmes, et celles des petites entreprises ont

11

tendance à revenir aux hommes. Selon l’étude conduite sur le marché du travail égyptien en 2008, la part des femmes dans les petites et moyennes entreprises n’était que de 17,9 %. Les femmes interviennent notamment dans des domaines tels que le lait et les produits laitiers, la transformation de base des denrées alimentaires par exemple pour les marinades et la fabrication de confitures, l’élevage et l’artisanat. Les contraintes les plus courantes entravant l’autonomisation économique des femmes rurales sont notamment l’accès limité aux financements ; les droits limités à la propriété de biens et aux actes officiels ; l’accès limité à la formation pour le personnel féminin des services de vulgarisation ; les taux élevés d’analphabétisme ; et les charges à supporter au titre des tâches domestiques, de l’encadrement des enfants et de l’attention aux personnes âgées. 3.2.6 Le projet entend éliminer bon nombre de ces contraintes, par le biais de la composante relative au renforcement des capacités. Les intermédiaires financiers seront encouragés à appliquer des plans de financement convenant aussi bien aux hommes qu’aux femmes pratiquant la petite agriculture, tandis que des campagnes de formation et de sensibilisation seront conduites, et les activités de développement social stimulées. Le projet adoptera une approche à plusieurs volets pour améliorer les résultats obtenus par les femmes sur le marché, i) en œuvrant à la promotion de l’entrepreneuriat féminin (les entreprises appartenant aux femmes devant représenter au moins 40 % de toutes les entreprises bénéficiaires) pour amener les femmes à s’engager dans des segments de la chaîne de valeur souvent dominés par les hommes, par exemple ceux de la distribution et de la commercialisation ; ii) en renforçant les compétences des femmes en matière de leadership pour que les femmes puissent participer à la gouvernance des associations et coopératives de petits exploitants agricoles ; et iii) en sensibilisant les hommes pour qu’ils appuient le renforcement du rôle des femmes dans le développement de la chaîne de valeur. Afin d’accroître la sensibilité du projet à la dimension genre, les mesures suivantes seront prises pendant l’exécution du projet : i) au moins 25 % des prêts du portefeuille de la SEDO et 40 % du portefeuille du microcrédit doivent être octroyés aux femmes chefs d’entreprises ; et ii) au moins 40 % des bénéficiaires des activités de formation visant à renforcer les capacités doivent être des femmes. Effets sociaux 3.2.7 Les statistiques récentes montrent que la pauvreté chronique est concentrée dans les zones rurales de la Haute Égypte où une proportion de 40,2 % de la population est considérée comme pauvre. En plus de la pauvreté, les zones rurales sont caractérisées par des taux d’analphabétisme élevés et l’accès limité à l’infrastructure et aux services de base. Pratiquant essentiellement l’agriculture de subsistance, avec un accès limité au revenu en espèces, un grand nombre d’hommes et de femmes sont à la recherche d’un revenu complémentaire qu’ils pourraient obtenir à la suite de la création de MPE. Toutefois, ils sont confrontés à des contraintes sociales et structurelles telles que l’accès limité aux financements, les pratiques des commerçants et des intermédiaires visant à les exploiter, l’accès limité au savoir et aux technologies, la vive méfiance régnant au sein des communautés, etc. Les pratiques agricoles actuelles sont fondées sur des méthodes traditionnelles, et l’application de technologies ou de mécanismes à valeur ajoutée est limitée, y compris au niveau de base. Le projet cherchera à éliminer ces contraintes en finançant plus de 4 800 petites entreprises agro-industrielles et plus de 20 000 microentreprises, et en facilitant localement la valeur ajoutée aux produits agricoles en vue de créer quelque 60 500 emplois sur la période de cinq ans couverte par le projet. Par ailleurs, l’encouragement d’une plus grande participation des différents acteurs et partenaires aux activités du projet contribuera à accroître ses effets positifs sur l’équité

12

sociale, grâce à : i) la réduction de l’isolement et l’amélioration de l’accès des pauvres aux possibilités offertes sur le plan économique ; et ii) la réduction de l’exclusion sociale de certains groupes tels que les femmes. L’accent mis par le projet sur le renforcement des FA et la création de partenariats public-privé sera crucial pour le renforcement du capital social local et l’appui aux interventions de développement économique à base communautaire qui contribueront à améliorer la qualité de vie des populations locales, à tous égards. Réinstallation involontaire 3.2.8 Il ne devrait pas y avoir de réinstallation involontaire dans le cadre du projet.

IV. EXÉCUTION 4.1 Arrangements en matière d’exécution Arrangements institutionnels 4.1.1 Le projet sera exécuté sur une période de cinq ans (60 mois). Le SFD sera l’organe d’exécution du projet (voir Annexe technique A2 pour une évaluation du SFD). En tant qu’organe d’exécution, le SFD entreprendra notamment les tâches spécifiques suivantes : i) fournir un appui efficace après l’approbation du prêt pour garantir la satisfaction de toutes les conditions préalables à remplir pour l’entrée en vigueur de l’accord de prêt et le premier décaissement, et l’effectivité du prêt le plus rapidement possible ; ii) assurer la gestion générale et l’administration quotidienne du projet ; et iii) assurer la tenue et la sauvegarde des dossiers et de l’actif du projet. L’Unité de l’agroindustrie du SFD, à travers le coordinateur spécial à recruter pour le projet, sera le point focal de l’exécution du projet. 4.1.2 Conformément aux pratiques opérationnelles du SFD, tous les prêts d’un montant allant jusqu’à 10 000 EGP sont considérés comme des prêts aux microentreprises et sont gérés par le MFCS, et tous les prêts d’un montant supérieur à 10 000 EGP sont considérés comme des prêts aux petites entreprises et leur administration est assurée par la SEDO. Il a été convenu avec le SFD qu’un gestionnaire de projet à plein temps (qui doit être un expert de la chaîne de valeur de l’agro-industrie) sera recruté pour assurer la promotion du projet ainsi que l’administration, la gestion et le suivi des activités quotidiennes du projet. Une partie du don d’assistance technique envisagé sera réservée pour ce poste dont le titulaire devra consacrer 75 % de son temps de travail à la Haute Égypte. L’annexe technique C3 présente le cadre de référence et le profil du gestionnaire du projet. 4.1.3 Afin de promouvoir et d’encourager les partenariats entre les acteurs nationaux et de promouvoir les synergies entre les initiatives nationales visant à développer l’agro-industrie, le projet prévoit la création d’un comité consultatif national composé de représentants du SFD, du Centre de modernisation industrielle, du Ministère de la Coopération internationale, du Ministère de l’Agriculture, du Ministère de l’Industrie et du Commerce et de la Chambre des industries alimentaires, ainsi que de représentants des gouvernorats locaux. Le SFD déléguera à l’IMC la mise en œuvre des activités de développement de la chaîne de valeur au titre de la composante relative au renforcement des capacités, compte tenu des compétences techniques avérées de l’IMC, de ses avantages comparatifs dans les domaines qu’appuie cette composante (voir Annexe technique A3 pour les informations détaillées concernant l’IMC), et de son engagement à fournir les fonds de contrepartie à hauteur de 1 million d’USD pour appuyer les activités de renforcement des capacités au titre du projet. Un accord de gestion basé sur la performance, contenant des dispositions détaillées, sera signé par le SFD et l’IMC. La signature de cet accord sera une des conditions préalables à remplir pour le décaissement des ressources du don.

13

Passation de marchés 4.1.4 Tous les marchés relatifs à l’achat de biens et à l’acquisition de services de consultants financés par la Banque, à partir des ressources du FAPA et du Fonds PRI, seront attribués conformément aux Règles et procédures de la Banque pour l’acquisition de biens et travaux ou, selon le cas, aux Règles et procédures de la Banque pour l’utilisation des consultants, en utilisant à cet effet les documents uniformisés d’appel d’offres de la Banque. Les marchés relatifs aux activités d’études et de formation spécialisées seront attribués conformément aux procédures de sélection à partir d’une liste restreinte d’institutions dotées des capacités, de l’expérience et de l’expertise requises pour entreprendre de telles activités qui comprendront notamment l’organisation de plusieurs ateliers de formation locaux à l’intention des membres du personnel du SFD et des IFP. 4.1.5 Pour le prêt de la BAD, le SFD procèdera à la rétrocession de ses ressources aux IFP, conformément à la politique de crédit du SFD. Aux termes des arrangements au titre du projet d’appui aux MPE en cours, tous les contrats relatifs aux facilités de crédit feront l’objet d’une revue à postériori. À cet égard, tous les documents relatifs au traitement des prêts, notamment les demandes de prêt, les documents de la revue, les rapports d’évaluation et d’appréciation, et les contrats signés seront tenus et conservés au siège du SFD, pour examen périodique par les missions de supervision de la Banque et les vérificateurs de la Banque. L’annexe technique B5 décrit en détail les arrangements en matière de passation de marchés au titre du projet. Décaissement 4.1.6 Les méthodes des comptes spéciaux et des paiements directs seront utilisées pour le décaissement des fonds au titre du projet. Un compte spécial distinct sera ouvert pour chaque source de fonds. L’annexe technique B4 décrit en détail les arrangements en matière de décaissement au titre du projet. Gestion financière 4.1.7 Les leçons apprises du projet relatif à la deuxième phase du Fonds social et du projet d’appui aux MPE en cours donnent à penser que le système de gestion financière du SFD est à même de produire des rapports financiers fournissant des informations suffisantes pour le suivi de l’utilisation des fonds, et de permettre la fourniture en temps voulu les financements nécessaires pour répondre aux besoins du projet. D’autres améliorations sont apportées à ce système au titre du projet d’appui aux MPE en cours, à la faveur de la mise en œuvre de la recommandation du Département de l’audit interne de la Banque demandant que le personnel de l’Unité de l’audit interne du SFD suive une formation à l’audit axé sur le risque. En réponse aux exigences fiduciaires, le SFD soumettra à la Banque des états financiers audités au moins six mois après la clôture de l’exercice financier. Le SFD veillera à ce que ses vérificateurs externes, pendant les audits annuels, émettent par écrit leur propre opinion sur l’utilisation des ressources du prêt et sur le respect des dispositions de l’accord de prêt conclu avec la BAD. Ils devront également émettre leur propre opinion sur l’utilisation des ressources fournies à titre de dons par le FAPA et le Fonds PRI. L’Unité de l’audit interne du SFD veillera à l’application des procédures convenues pour les activités opérationnelles, la comptabilité, les paiements et la passation de marchés dans le cadre de l’exécution du projet. Elle procédera chaque année à l’audit d’au moins 30 % à 40 % des prêts octroyés et décaissés en faveur des MPE, et notamment de l’utilisation des ressources de ces prêts au niveau des

14

MPE. Elle fera également des recommandations sur la résolution des problèmes systémiques identifiés, le cas échéant. Les procédures de suivi des recommandations de l’audit seront conformes aux pratiques de la Banque. 4.2 Suivi Le suivi et l’évaluation seront une partie intégrante du projet. La Direction du SFD assumera la responsabilité globale du suivi et des résultats du projet. Les capacités du SFD à cette fin sont en train d’être renforcées dans le cadre du projet d’appui aux MPE en cours. Pour toutes les autres activités du projet, les agences d’exécution fourniront mensuellement au SFD des informations sur les produits et les résultats du projet, selon le modèle convenu, y compris des rapports périodiques sur la performance du projet, en prenant soin de ventiler les données par sexe. Les données et indicateurs de référence seront déterminés pour faciliter l’évaluation des progrès réalisés par le projet et son impact. Une évaluation à mi-parcours sera conduite deux ans et demi après le démarrage de l’exécution du projet en vue de procéder à des ajustements, si nécessaire. Le SFD soumettra à la Banque des rapports trimestriels d’étape sur le projet, selon le modèle établi et couvrant tous les aspects du projet, dans les 30 jours suivant la fin de chaque trimestre. En outre, compte tenu de la nature participative et fondée sur la demande du projet, une enquête auprès des clients (basée dans une large mesure sur les outils de suivi communautaire) sera conduite avant la revue à mi-parcours du projet, afin d’évaluer les perceptions des bénéficiaires concernant l’exécution du projet et son impact sur la vie des bénéficiaires. 4.3 Gouvernance La Direction du SFD a mis en place un système efficace de contrôle interne pour garantir l’intégrité de ses opérations financières et fournir à son Conseil et à ses donateurs l’assurance que ses actifs sont sauvegardés et que des dossiers appropriés sont tenus sur ses activités. À cet égard, l’Unité de l’audit interne conduit des audits pour garantir l’adéquation, l’efficacité et la pertinence des mesures de contrôle. Les faiblesses identifiées sont portées à l’attention du Conseil et font l’objet de mesures de suivi. Par ailleurs, le SFD fait régulièrement l’objet d’audits conduits par des vérificateurs externes. La revue multidonateurs du SFD conduite en 2004 est parvenue à la conclusion qu’en général, la gouvernance institutionnelle s’est améliorée au sein du SFD depuis 2002. Par le biais du projet d’appui aux MPE en cours, la Banque contribue à d’autres améliorations à cet égard, en renforçant les capacités de l’Unité de l’audit interne du SFD. 4.4 Viabilité 4.4.1 Octroyer des prêts aux taux appliqués sur le marché, tel qu’envisagé au titre du projet, contribuera à renforcer la viabilité opérationnelle et financière à long terme des opérations de prêts du SFD et à accroître les capitaux d’emprunt nécessaires pour financer l’expansion continue de ses opérations. De même, aux termes de la politique de crédit du SFD, les banques et ONG intermédiaires sont tenues d’accorder des prêts aux emprunteurs finals aux taux d’intérêt leur permettant de garantir la viabilité et l’expansion continues de leur clientèle. 4.4.2 L’ouverture d’un compte pour le fonds renouvelable au sein du SFD, pour chaque facilité de crédit relevant des portefeuilles de la SEDO et du MFCS, permettra de garantir le maintien du processus d’intermédiation financière au-delà de la période couverte par le

15

projet. Au titre de la composante relative au renforcement des capacités, tout sera mis en œuvre pour renforcer les capacités des IFP à adapter et à accroître les prêts aux entreprises agro-industrielles. Avec une source durable de crédit, les entreprises agro-industrielles sont aussi à même de mobiliser des financements accrus pour appuyer l’expansion de leurs activités opérationnelles ou pour répondre à des besoins temporaires en fonds de roulement, contribuant ainsi à la création durable d’emplois. 4.4.3 La durabilité des activités qui seront financées dans le cadre du projet sera renforcée grâce à la solide expérience du SFD et de ses intermédiaires sélectionnés dans le financement des MPE, ainsi qu’en raison du caractère intégré de l’aide au développement fournie aux entreprises. En plus des ressources financières, le SFD fournira également aux entreprises une aide non financière, y compris la formation à la gestion des entreprises. Par ailleurs, le projet devrait améliorer certains avantages attendus des projets en cours financés par les fonds des Nations Unies pour l’atteinte des OMD et le FIDA, qui couvrent d’importantes questions telles que le renforcement des capacités techniques et gestionnaires des FA et des MPE par la formation, la promotion de la compétitivité par le biais du transfert de technologies, et l’amélioration de l’accès aux services d’appui et de l’utilisation de ces services. L’adoption d’une telle approche multidimensionnelle pour s’attaquer aux problèmes auxquels sont confrontées les MPE devrait permettre de garantir la viabilité des entreprises devant bénéficier de financements au titre du projet proposé. 4.5 Gestion des risques En raison du caractère innovant du projet en Égypte, un certain nombre de risques lui sont associés, notamment : i) les réticences du secteur privé à s’engager pleinement dans le projet ; ii) les capacités d’exécution limitées ; iii) les barrières entravant la participation des pauvres à la commercialisation des produits agricoles ; et iv) les réticences des banques intermédiaires à octroyer des prêts aux entreprises agro-industrielles. En général, l’adoption d’une approche pilote aidera à atténuer ces risques. En outre, les mesures précises préconisées pour atténuer chacun de ces risques sont les suivantes :

• Associations constituées, mais manquant de capacités pour l’élaboration et la

mise en œuvre de plans d’activités : Ce risque sera atténué par la fourniture de l’assistance technique aux associations, au titre de la composante I du projet.

• Manque d’intérêt des opérateurs d’exploitations agricoles commerciales pour

la conclusion d’alliances productives avec les associations d’agriculteurs : Ce risque sera atténué par l’engagement d’une institution nationale telle que l’IMC dans l’identification des sociétés intéressées et l’établissement de relations d’affaires entre ces sociétés et les associations d’agriculteurs en vue de la constitution d’alliances entre entreprises ou pour les différents produits.

• Barrières entravant la participation des pauvres à la commercialisation des

produits agricoles : Ce risque sera atténué par les activités liées à l’assistance technique holistique à fournir aux petits exploitants agricoles (par exemple les liens avec les marchés, le perfectionnement des compétences entrepreneuriales, la promotion de la concurrence, la publicité et la sensibilisation).

16

• Réticences des intermédiaires financiers à octroyer des prêts aux associations d’agriculteurs nouvellement constituées : Ce risque sera atténué par la formation qui sera dispensée aux membres du personnel (y compris aux cadres supérieurs) des institutions d’intermédiation financière, et par l’adoption éventuelle d’instruments de financement innovants pour les entreprises agro-industrielles.

• Risque de crédit : Au titre des arrangements de garantie du crédit en vigueur,

le SFI couvre 10 % du risque de crédit des IFP, en plus de couvrir le risque de crédit par le biais de la Société d’assurance de coopératives (CIS), jusqu’à 80 %. Il reste donc à la Banque à couvrir le risque de crédit à hauteur de 10 % pour le solde non remboursé des prêts octroyés aux MPE. Le fonctionnement de la CIS (ou d’une institution similaire) a une incidence sur l’efficacité du modèle opérationnel du SFD. Une augmentation significative du taux de défaut de remboursement chez les bénéficiaires finals pourrait avoir un impact négatif sur les capacités financières de la CIS. Bien que l’expérience montre que la plupart des prêts non productifs sont remboursés et que les sorties du bilan sont limitées, le SFD devra encore atténuer ce risque en veillant à l’application de procédures prudentes pour les critères d’évaluation et d’éligibilité, et en faisant preuve de flexibilité dans le choix des arrangements de garantie pour les IFP.

• Risque de change : La plupart des prêts obtenus par le SFD auprès des

donateurs sont libellés en devises, alors que le SFD procède à leur rétrocession globale aux intermédiaires en monnaie locale, c’est-à-dire en livres égyptiennes (LE), ce qui expose davantage le SFD au risque de change, d’où la nécessité d’assurer le suivi de ce risque sur une base continuelle. La création d’un département spécialisé de la trésorerie au sein du SFD facilitera la mise en œuvre de mesures d’atténuation et améliorera la gestion de la liquidité au sein de cette institution.

4.6 Renforcement du savoir Étant donné que l’approche de la chaîne de valeur promue au titre du présent projet est relativement nouvelle en Égypte, le renforcement du savoir sera une partie intégrante du projet. Par le biais de sa composante relative au renforcement des capacités, le projet fournira des services d’assistance technique et de formation (y compris peut-être la formation à l’étranger) à la cartographie et à l’analyse de la chaîne de valeur, à l’établissement de relations d’affaires et au développement de la chaîne de valeur, au bénéfice des pauvres dans les zones rurales. Le SDF et l’IMC diffuseront et appliqueront le savoir produit dans le cadre du projet dans la définition des rôles et mécanismes des secteurs public et privé, le ciblage des programmes sur la chaîne de valeur au bénéfice des groupes plus pauvres et des activités soucieuses de l’environnement, le financement des plans d’activités élaborés, et l’engagement des partenaires financiers. Dans le cadre de l’apprentissage axé sur l’action, les capacités des FA seront renforcées pour qu’elles puissent mieux se positionner dans la chaîne de valeur et apporter de nouvelles idées sur le plan opérationnel. Cette expérience pourrait également contribuer à infléchir la politique gouvernementale en matière de développement des entreprises.

17

V. INSTRUMENTS ET AUTORITÉ JURIDIQUES 5.1 Instruments juridiques Le présent projet sera financé par un prêt BAD et un don

du Fonds PRI. 5.2 Conditions liées à l’intervention de la Banque Conditions attachées au prêt BAD A. Conditions préalables à remplir pour l’entrée en vigueur de l’accord de prêt L’entrée en vigueur de l’accord portant octroi du prêt BAD est subordonnée à la satisfaction, par l’emprunteur, des conditions énoncées à la section 5.01 des Conditions générales applicables aux accords de prêts et de garanties de la BAD. B. Conditions préalables à remplir pour le premier décaissement Les obligations de la Banque quant au décaissement des ressources du prêt sont subordonnées à l’entrée en vigueur de l’accord de prêt et à la satisfaction, par l’emprunteur, des conditions ci-après, d’une manière acceptable pour la Banque : L’emprunteur devra avoir :

a) produit la preuve de l’ouverture d’un compte spécial en USD par le Fonds

social pour le développement (FSD) auprès d’une banque acceptable pour la Banque, aux fins de virement des montants décaissés au titre du prêt;

b) soumis à la Banque un exemplaire signé de l’accord de rétrocession du prêt conclu

entre l’emprunteur et le SFD (ci-après désigné «accord de rétrocession du prêt»), aux termes duquel l’emprunteur rétrocède l’intégralité du montant du prêt au SFD, aux mêmes modalités et conditions que celles qui sont stipulées dans l’accord de prêt.

Conditions liées au don du Fonds PRI de la Banque A. Conditions préalables à remplir pour l’entrée en vigueur de l’accord de don L’entrée en vigueur de l’accord de don est subordonnée à la signature d’une lettre d’accord par la Banque et le Gouvernement de l’Égypte (ci-après désigné le «bénéficiaire»). B. Conditions préalables à remplir pour le premier décaissement Le bénéficiaire devra avoir :