five leadership issues worthy of board and executive attention · Innovation within any large...

7

FIVE LEADERSHIP ISSUES WORTHY OF BOARD AND EXECUTIVE ATTENTION FINANCIAL SERVICES SECTOR

Transcript of five leadership issues worthy of board and executive attention · Innovation within any large...

five leadership issues worthy of board and

executive attention

financial services sector

encouraging and capturing innovation

� Innovation within any large institution is difficult, but in a heavily-regulated financial services firm it is particularly challenging.

� Learning from attackers, watching competitors, and creating cultures and teams designed to innovate will be critical to staying relevant to the clients of the future.

29% of banking executives cite this as one of the top three investment priorities1

“Research, development

and innovation”

1. PwC’s Retail Banking 2020 Survey: Evolution or Revolution, February 2014

companies are creating roles dedicated to innovation

Chief Innovation and Disruption Officer

Chief Innovation Officer

Chief Innovation Officer

Technology Evangelist

Key points � Learn from the best – non-financial

institutions are typically more open to giving employees time to develop new ideas and reward trying them (even if experiments fail).

� Actively monitor new technologies, products and customer service models happening outside of financial services.

� Invest in incentive systems that encourage experimentation and the testing of new ideas.

“Lloyds Banking Group ... has been working with the prime minister’s office to test whether banks could vouch for their customers’ identities to other organisations via a simple smartphone app ...

... It’s the latest attempt to rethink the role of banks in the digital era – both to avoid their businesses being cannibalised by start-ups and to restore their image.”

Financial Times, September 2, 2014

Asset MAnAgeMent

� Proliferation of players

� Alpha/beta separation

� Squeezed “middle”, move to passive or specialized players

BAnking � Markets breaking

away under regulatory changes

� Non-regulated attackers

� Payment providers

� Aggregators

insurAnce � Capital pressures

� Aggregators

trAditionAl FinAnciAl services

MArgins

margins are under pressure across much of financial services

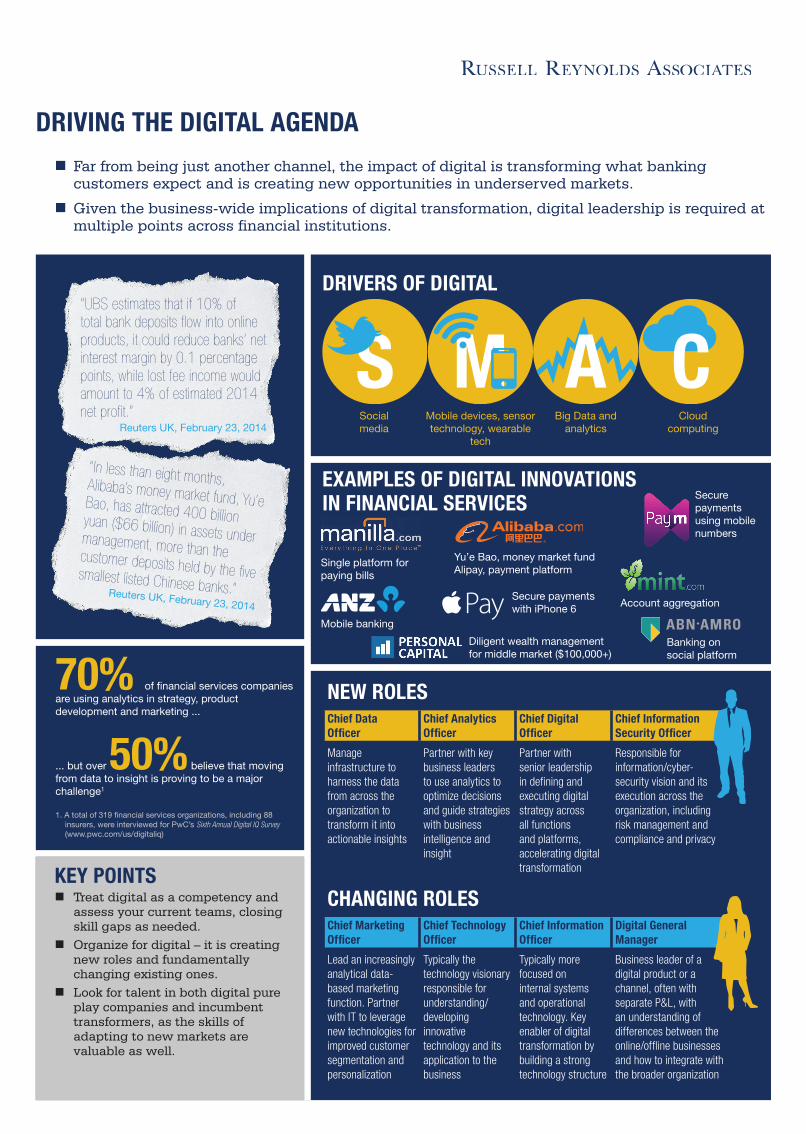

driving the digital agenda

� Far from being just another channel, the impact of digital is transforming what banking customers expect and is creating new opportunities in underserved markets.

� Given the business-wide implications of digital transformation, digital leadership is required at multiple points across financial institutions.

drivers of digital

examples of digital innovations in financial services

Social media

Mobile devices, sensor technology, wearable

tech

Big Data and analytics

Cloud computing

M AS C“UBS estimates that if 10% of total bank deposits flow into online products, it could reduce banks’ net interest margin by 0.1 percentage points, while lost fee income would amount to 4% of estimated 2014 net profit.”

Reuters UK, February 23, 2014

“In less than eight months, Alibaba’s money market fund, Yu’e Bao, has attracted 400 billion yuan ($66 billion) in assets under management, more than the customer deposits held by the five smallest listed Chinese banks.”Reuters UK, February 23, 2014

Mobile banking

Yu’e Bao, money market fund Alipay, payment platform

Account aggregation

Banking on social platform

Single platform for paying bills

Secure payments using mobile numbers

Diligent wealth management for middle market ($100,000+)

new rolesChief Data Officer

Chief Analytics Officer

Chief Digital Officer

Chief Information Security Officer

Manage infrastructure to harness the data from across the organization to transform it into actionable insights

Partner with key business leaders to use analytics to optimize decisions and guide strategies with business intelligence and insight

Partner with senior leadership in defining and executing digital strategy across all functions and platforms, accelerating digital transformation

Responsible for information/cyber- security vision and its execution across the organization, including risk management and compliance and privacy

changing rolesChief Marketing Officer

Chief Technology Officer

Chief Information Officer

Digital General Manager

Lead an increasingly analytical data-based marketing function. Partner with IT to leverage new technologies for improved customer segmentation and personalization

Typically the technology visionary responsible for understanding/developing innovative technology and its application to the business

Typically more focused on internal systems and operational technology. Key enabler of digital transformation by building a strong technology structure

Business leader of a digital product or a channel, often with separate P&L, with an understanding of differences between the online/offline businesses and how to integrate with the broader organization

70% of financial services companies are using analytics in strategy, product development and marketing ...

... but over 50% believe that moving from data to insight is proving to be a major challenge1

1. A total of 319 financial services organizations, including 88 insurers, were interviewed for PwC’s Sixth Annual Digital IQ Survey (www.pwc.com/us/digitaliq)

Key points � Treat digital as a competency and

assess your current teams, closing skill gaps as needed.

� Organize for digital – it is creating new roles and fundamentally changing existing ones.

� Look for talent in both digital pure play companies and incumbent transformers, as the skills of adapting to new markets are valuable as well.

Secure payments with iPhone 6

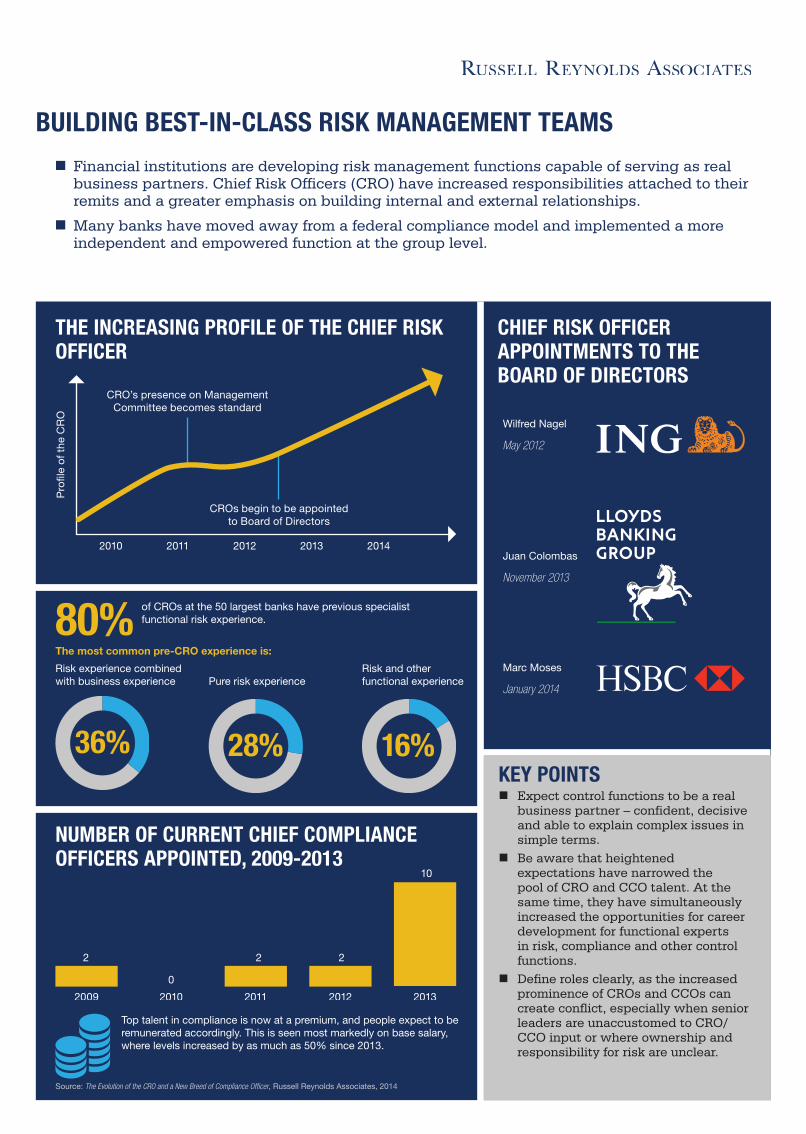

building best-in-class risK management teams

� Financial institutions are developing risk management functions capable of serving as real business partners. Chief Risk Officers (CRO) have increased responsibilities attached to their remits and a greater emphasis on building internal and external relationships.

� Many banks have moved away from a federal compliance model and implemented a more independent and empowered function at the group level.

chief risK officer appointments to the board of directors

Wilfred Nagel

May 2012

Juan Colombas

November 2013

Marc Moses

January 2014

the increasing profile of the chief risK officer

CROs begin to be appointedto Board of Directors

Pro

�le

of t

he C

RO

2010 2011 2012 2013 2014

CRO’s presence on ManagementCommittee becomes standard

80%

36%

Pure risk experienceRisk and other functional experience

Risk experience combined with business experience

28% 16%

of CROs at the 50 largest banks have previous specialist functional risk experience.

The most common pre-CRO experience is:

Top talent in compliance is now at a premium, and people expect to be remunerated accordingly. This is seen most markedly on base salary, where levels increased by as much as 50% since 2013.

Key points � Expect control functions to be a real

business partner – confident, decisive and able to explain complex issues in simple terms.

� Be aware that heightened expectations have narrowed the pool of CRO and CCO talent. At the same time, they have simultaneously increased the opportunities for career development for functional experts in risk, compliance and other control functions.

� Define roles clearly, as the increased prominence of CROs and CCOs can create conflict, especially when senior leaders are unaccustomed to CRO/CCO input or where ownership and responsibility for risk are unclear.

number of current chief compliance officers appointed, 2009-2013

2

0

2 2

10

2009 2010 2011 2012 2013

Source: The Evolution of the CRO and a New Breed of Compliance Officer, Russell Reynolds Associates, 2014

driving the diversity agenda with business logic

� Financial institutions are often ahead of the curve when it comes to diversity. However, more needs to be done to increase diversity in the executive suite.

diversity improves performancecoMpAnies with At leAst one woMAn on the BoArd outperForMed those with no woMen By 26%

Credit Suisse, Gender Diversity and Corporate Performance 2012 Survey, Performance over six years

26%

financial services firms are ahead of the curveFinAnciAl services coMpAnies Account For 1 in 4 oF the times’ top 50 eMployers For woMen in 2013

1 in 4

but, still, there are very few women at the top

diversity doesn’t only mean gender

INSURANCE

2% of CEOs are women

ASSET MANAGEMENT

7% of CEOs are women

BANKING

4% of CEOs are women

Key points � Keep your business needs and objectives at the

forefront of any diversity initiatives. � Be flexible and creative. Consider options such

as job sharing and redeployment for individuals who would flourish in a different environment.

� Approach diversity as a business initiative, not a check-the-box activity.

� Enlist the help of objective advisors to avoid hiring like-for-like. This is one of the greatest obstacles to diversity.

18%oF ceos At top BAnking institutions Are oF A diFFerent nAtionAlity FroM their heAdquArters

creating a highly effective board

� Best-in-class corporate governance is becoming more important as corporations face a significant increase in regulatory scrutiny and heightened expectations regarding risk management.

� Financial institutions are focused on improving Board composition and effectiveness, growing the presence of cross-functional experts and formalizing CEO succession plans.

boards’ understanding of it risK1

1. National Association of Corporate Directors’ 2013-2014 Public Company Governance Survey; based on 1,019 public company responses

12.9%High level of technical knowledge

62.9%Some technical knowledge butcould bene�t from improvement

24.2%Little technical knowledgeand needs improvement

$11.6 million per year,The average cost of cybercrime for a company in the United States in 2013 was

up 26% from 2012.

boards’ approach to ceo succession planning1

1. National Association of Corporate Directors’ 2013-2014 Public Company Governance Survey; based on 1,019 public company responses

54.7%

FORMAL PLANNING PROCESS

38.6%

2013

2011

INFORMAL DISCUSSIONS

38.6%

52.3%

2013

2011

NO PROCESS OR DISCUSSIONS

6.7%

9.1%

2013

2011

Key facts on diversity in board compositionOf the Non-Executive Directors of the world’s 30 largest banks:

26%Are FeMAle

36%hAve A nAtionAlity other thAn thAt oF their BAnk’s hq

59%hAve experience working in A BAnk

2 of the 30 banks have less than 10% female representation

2 of the 30 banks have over 40% female representation

The more diverse Boards in terms of nationality tend to be at European banks

Key points � Conduct regular reviews to enable the CEO,

Chairman and Directors to rate the importance of each role’s responsibilities, as well as to determine how effective the individuals currently in these roles are at delivering against those responsibilities.

� Seek out an external perspective and be open to change. There has been good progress in understanding critical Board performance issues and how to address them.

� Ensure that all parties demonstrate honesty, trust, respect and transparency. Open dialogue is the basis for any highly-performing Board.

ForMAl plAnning is increAsingly in FAvor

Russell Reynolds Associates is a global leader in assessment, recruitment and succession planning for chief executive officers, boards of directors and key roles within the C-suite. With 350 consultants in 44 offices around the world, we work closely with both public and private organisations across all industries and regions. We help our clients build boards and executive teams that can meet the challenges and opportunities presented by the digital, economic, environmental and political trends that are reshaping the global business environment.

www.russellreynolds.com

© Copyright 2014, Russell Reynolds Associates. All rights reserved

global offices

about russell reynolds associates

AMericAs• Atlanta

• Boston

• Buenos Aires

• Calgary

• Chicago

• Dallas

• Houston

• Los Angeles

• Mexico City

• Minneapolis/St. Paul

• New York

• Palo Alto

• San Francisco

• São Paulo

• Stamford

• Toronto

• Washington, D.C.

AsiA/pAciFic• Beijing

• Hong Kong

• Melbourne

• Mumbai

• New Delhi

• Seoul

• Shanghai

• Singapore

• Sydney

• Tokyo

europe• Amsterdam

• Barcelona

• Brussels

• Copenhagen

• Frankfurt

• Hamburg

• Helsinki

• Istanbul

• London

• Madrid

• Milan

• Munich

• Oslo

• Paris

• Stockholm

• Warsaw

• Zürich