Langages

Pages

Légal

Rapport Annuel 07/ Annual Report 07

Le Groupe BLOMBANK est fidèle à sa mission premièrede veiller à la sérénité “Peace of Mind” de nos clients en

leur offrant une large gamme de produits et services bancairesadaptée à leurs besoins diversifiés.

Dans cet esprit, nous accordons une importance particulière audéveloppement de notre réseau international afin d’accompagner

nos clients à travers le monde pour leur assurer la sérénité à laquelleils aspirent dans leurs opérations bancaires.

Direction GénéraleM. Michel ADWAN - M. Gilbert MOINE - M. Samer AZHARI - M. Iskandar ARAMAN

06 CONSEIL D’ADMINISTRATION07 ORGANIGRAMME DU GROUPE9 RAPPORT DE L’ACTIVITE DE LA BANQUE EN 200712 BILAN CONSOLIDE14 COMPTE DE RESULTAT CONSOLIDE16 RAPPORT DES COMMISSAIRES AUX COMPTES

SUR LES COMPTES CONSOLIDES21 TABLE DES MATIERES DE L’ANNEXE DE L’ANNEE 2007100 ADRESSES DE BLOM BANK GROUP

BOARD OF DIRECTORS 06GROUP CHART 07PRINCIPAL FEATURES OF THE FINANCIAL YEAR 2007 56CONSOLIDATED BALANCE SHEET 58CONSOLIDATED PROFIT AND LOSS ACCOUNT 60STATUTORY AUDITORS’ REPORT ON THE CONSOLIDATEDFINANCIAL STATEMENTS 62TABLE OF CONTENTS OF YEAR 2007 ANNEX 65DIRECTORY OF BLOM BANK GROUP 100

SOMMAIRE / SUMMARY

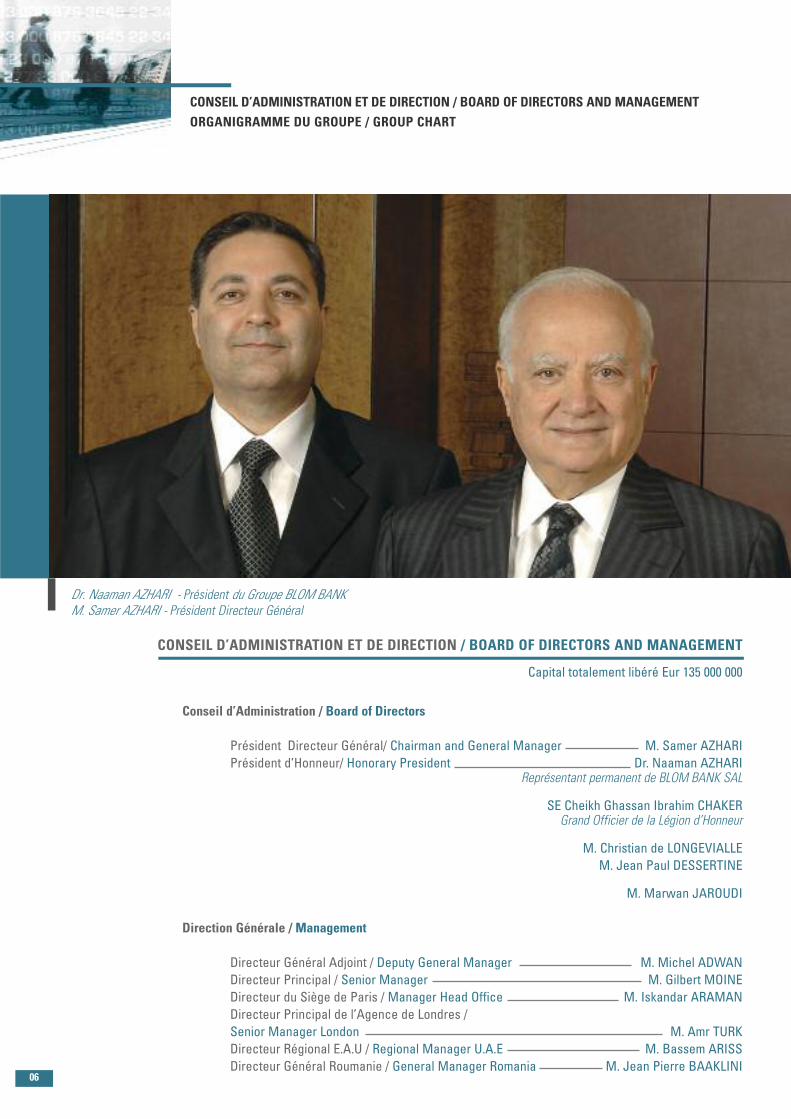

Dr. Naaman AZHARI - Président du Groupe BLOM BANKM. Samer AZHARI - Président Directeur Général

06

CONSEIL D’ADMINISTRATION ET DE DIRECTION / BOARD OF DIRECTORS AND MANAGEMENT

Capital totalement libéré Eur 135 000 000

CONSEIL D’ADMINISTRATION ET DE DIRECTION / BOARD OF DIRECTORS AND MANAGEMENT

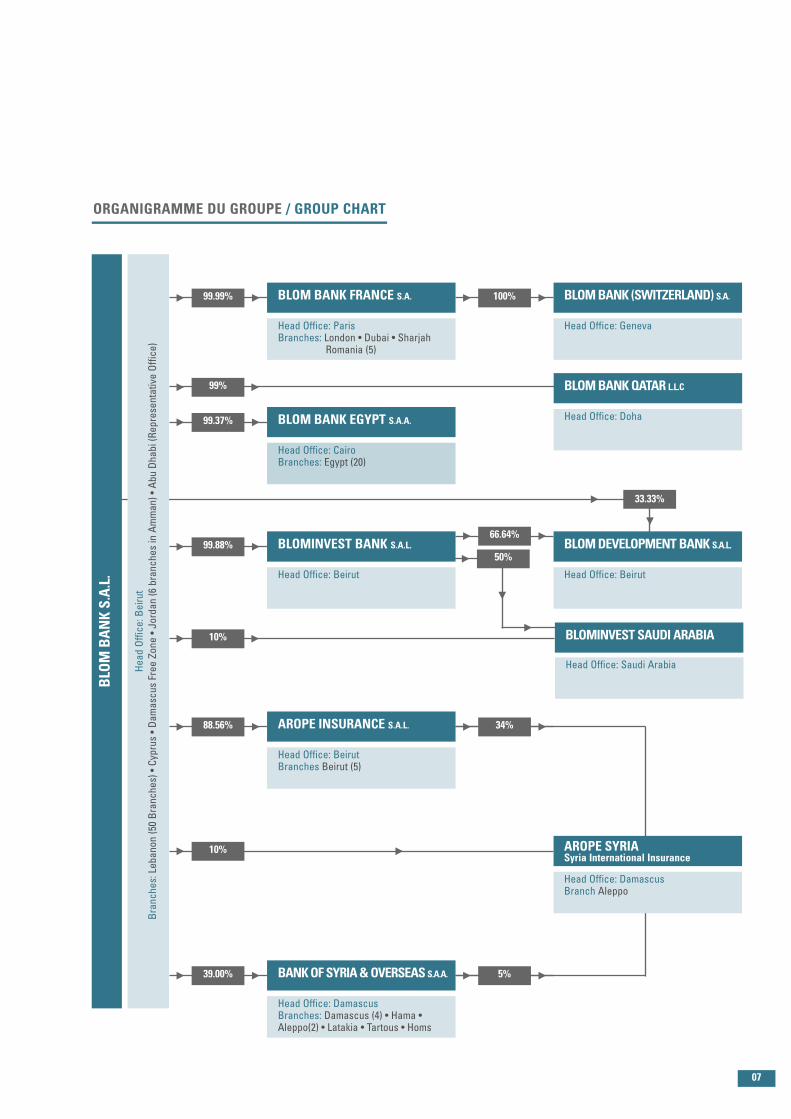

ORGANIGRAMME DU GROUPE / GROUP CHART

Conseil d’Administration / Board of Directors

Président Directeur Général/ Chairman and General Manager M. Samer AZHARIPrésident d’Honneur/ Honorary President Dr. Naaman AZHARI

Représentant permanent de BLOM BANK SAL

SE Cheikh Ghassan Ibrahim CHAKERGrand Officier de la Légion d’Honneur

M. Christian de LONGEVIALLEM. Jean Paul DESSERTINE

M. Marwan JAROUDI

Direction Générale / Management

Directeur Général Adjoint / Deputy General Manager M. Michel ADWANDirecteur Principal / Senior Manager M. Gilbert MOINEDirecteur du Siège de Paris / Manager Head Office M. Iskandar ARAMANDirecteur Principal de l’Agence de Londres /Senior Manager London M. Amr TURKDirecteur Régional E.A.U / Regional Manager U.A.E M. Bassem ARISSDirecteur Général Roumanie / General Manager Romania M. Jean Pierre BAAKLINI

33.33%

ORGANIGRAMME DU GROUPE / GROUP CHART

50%

BLO

MBANKS.A.L.

HeadOffice:B

eirut

Branches:Lebanon(50Branches)•C

yprus•D

amascusFree

Zone

•Jordan(6branches

inAmman)•

Abu

Dhabi(RepresentativeOffice)

BLOM BANK FRANCE S.A.

Head Office: ParisBranches: London • Dubai • Sharjah

Romania (5)

99.99% BLOMBANK (SWITZERLAND) S.A.

Head Office: Geneva

100%

BLOM BANK EGYPT S.A.A.

Head Office: CairoBranches: Egypt (20)

99.37%

BLOMINVEST BANK S.A.L.

Head Office: Beirut

99.88% BLOMDEVELOPMENTBANK S.A.L.

Head Office: Beirut

66.64%

AROPE INSURANCE S.A.L.

Head Office: BeirutBranches Beirut (5)

AROPE SYRIASyria International Insurance

Head Office: DamascusBranch Aleppo

88.56%

10%

Head Office: DamascusBranches: Damascus (4) • Hama •Aleppo(2) • Latakia • Tartous • Homs

39.00%

34%

5%BANKOFSYRIA&OVERSEASS.A.A.

BLOMINVEST SAUDI ARABIA10%

Head Office: Saudi Arabia

99% BLOMBANKQATAR L.L.C

Head Office: Doha

07

M. Samer AZHARI - Président Directeur Général

08

RAPPORT DE L’ACTIVITE DE LA BANQUE EN 2007

Comme les années précédentes, l’année 2007 a été marquée par une situation instable auMoyen-Orient, confortant ainsi la stratégie du Groupe de renforcer l’activité de sa filialefrançaise. BLOM BANK FRANCE a, dans cet environnement, prouvé une fois de plus la stabilitéde ses assises avec des résultats en progression continue et des ratios bilanciels etprudentiels remarquables, confirmant ainsi la volonté jamais démentie de progresser touten privilégiant la politique de prudence qui caractérise sa gestion.

Cet exercice aura été marqué principalement par l’intégration dans nos comptes des branchesRoumaines, précédemment détenues par Blom Bank Egypt, laquelle s’est finalisée le 30novembre 2007.L’exercice 2007 aura également vu notre société adopter une nouvelle structure organisationnellequi s’articule principalement autour de :- la séparation entre la structure du siège –renforcée par des départements fonctionnels et desupport- et l’agence de Paris.- la mise en place de filières intégrées dans le dispositif des agences et rapportantfonctionnellement aux diverses directions du siège dans les domaines de la gestionde risques, de l’informatique, des ressources humaines, de la finance et comptabilitéet de l’audit interne.- la mise en place d’une nouvelle approche budgétaire.- l’intégration de membres du Conseil d’Administration au Comité d’Audit et l’adoption d’unecharte d’audit.

Sur le plan purement financier, malgré une nouvelle baisse de la parité US Dollar / Euro (moins12%en2007etmoins25%endeuxans) le total bilandeBLOMBANKFranceestenprogression (+11%pourles comptes sociaux et + 9%pour les comptes consolidés).Les résultats pour leur part sont encore en augmentation à EUR 9 844 492 pour le résultat social et àEUR 14 555 865 pour le résultat consolidé (soit respectivement + 27% et + 23% par rapport à 2006).

Malgré la situation au Liban qui continue à se dégrader, notre Maison Mère, La BLOM BANKSAL, qui détient plus de 99% de nos actions, présente pour l’exercice 2007 des résultats bilancielstoujours en progression. Toutes les composantes du groupe sont en progression et les chiffresconsolidés présentent des niveaux en croissance remarquable.BLOM BANK SAL s’est vu décerner par « Moody’s » le meilleur rating local soit « Aa1,lb ».

RAPPORT DE L’ACTIVITE DE LA BANQUE EN 2007

09

Comme le groupe BLOM BANK FRANCE, les autres filiales de BLOM BANK SAL, tant en Syrie avec«Bank of Syria and Overseas» qu’en Egypte avec «Blom Bank Egypt», ont continué leur progression.

Les principales caractéristiques de notre Maison Mère «BLOM BANK SAL» sur base consolidéepour l’exercice 2007 sont les suivantes :

- Augmentation de 17% du total bilan à US Dollar 16.6 Milliards.- Croissance également des dépôts de 17% atteignant US$ 13.7 Milliards fin 2007.- Des profits nets atteignant USD 204.9 millions (en augmentation de 13.8%).- Un ratio de solvabilité à plus du double du niveau requis au Liban.- Des fonds propres (Tier I & II Capital) à USD 1.4 milliard.

Le total du bilan de BLOM BANK FRANCE s’élève à EUR 1 816 millions à fin 2007 en progressionde 9,31 % par rapport à fin 2006.L’ensemble des crédits à la clientèle s'établit à EUR 307 millions à fin 2007 contre EUR 249millions à fin 2006 (soit une progression de 23,55% due pour une bonne part à l’intégration dessuccursales roumaines).

Les immobilisations s’élèvent à fin 2007 à 10,79 millions d’euros et sont en progression de prèsde 121% essentiellement en raison de l’intégration des biens immobiliers détenus dans leslivres des succursales roumaines.

Les dépôts de la clientèle s’élèvent à EUR 1 437 millions à fin 2007, soit une progression de 8 %sur les chiffres de l’exercice précédent (20,8 % sur les chiffres exprimés en USD) ; la part desdépôts des branches roumaines s’élève à EUR 41 millions.

Les engagements vis-à-vis de la clientèle ne représentent que 21 % des dépôts de la clientèleet seulement 19 % de l’ensemble des dépôts, reflétant ainsi l’excellent niveau de la liquiditéglobale et confirmant, si besoin était, la prudence évoquée ci-dessus.

Le produit net bancaire s’élève pour 2007 à EUR 36,42 Millions (35,71 compte non tenu de laRoumanie) contre 31,09 millions en 2006.

RAPPORT DE L’ACTIVITE DE LA BANQUE EN 2007

10

Les charges générales d’exploitation (frais généraux, frais de personnel, taxes, etc.) sont enaugmentation de 17.85 % à EUR 15.87 millions contre EUR 13.47 millions l’an passé. Outrel’intégration des succursales roumaines qui intervient à hauteur d’environ 10%, cetteaugmentation est principalement causée par la hausse des charges de personnel consécutive auxrecrutements effectués cette année, notamment à Paris et aux Emirats Arabes Unis, et aunécessaire ajustement des salaires aux Emirats Arabes Unis du fait de l’inflation très élevéedans cette région.

Les dotations aux amortissements des immobilisations sont stables et se montent à EUR 0.50millions en 2007 (0.53 en 2006).

Les dotations nettes aux provisions sur créances de la clientèle s’élèvent à EUR 0.92 millions(1.49 millions en 2006).

Le bénéfice brut d’exploitation (avant impôt sur les bénéfices, dotation et reprise de provi-sions pour créances, mais après amortissement) ressort à EUR 20.04 millions (contre 17.09Millions en 2006), soit 17.26% de progression.

Le bénéfice consolidé de l’exercice s’élève à EUR 14 555 864.69 contre EUR 11 799 888.61 en2006.

Le contexte politique au Moyen-Orient, ainsi que l’effet des turbulences économiques des marchés,ne feront certainement pas changer BLOM BANK FRANCE dans sa manière d’appréhender sondéveloppement, c'est-à-dire de façon prudente et modérée. Toutefois, notre société s’attend àprofiter des fruits de son récent développement (tant interne qu’externe) et reste donc optimistepour les prochains exercices.

La structuration organisationnelle entreprise cette année doit se poursuivre et notre sociétéreste vigilante à toute opportunité de développement à la condition première que celle-ciréponde à nos exigences en matière de maîtrise des risques.

11

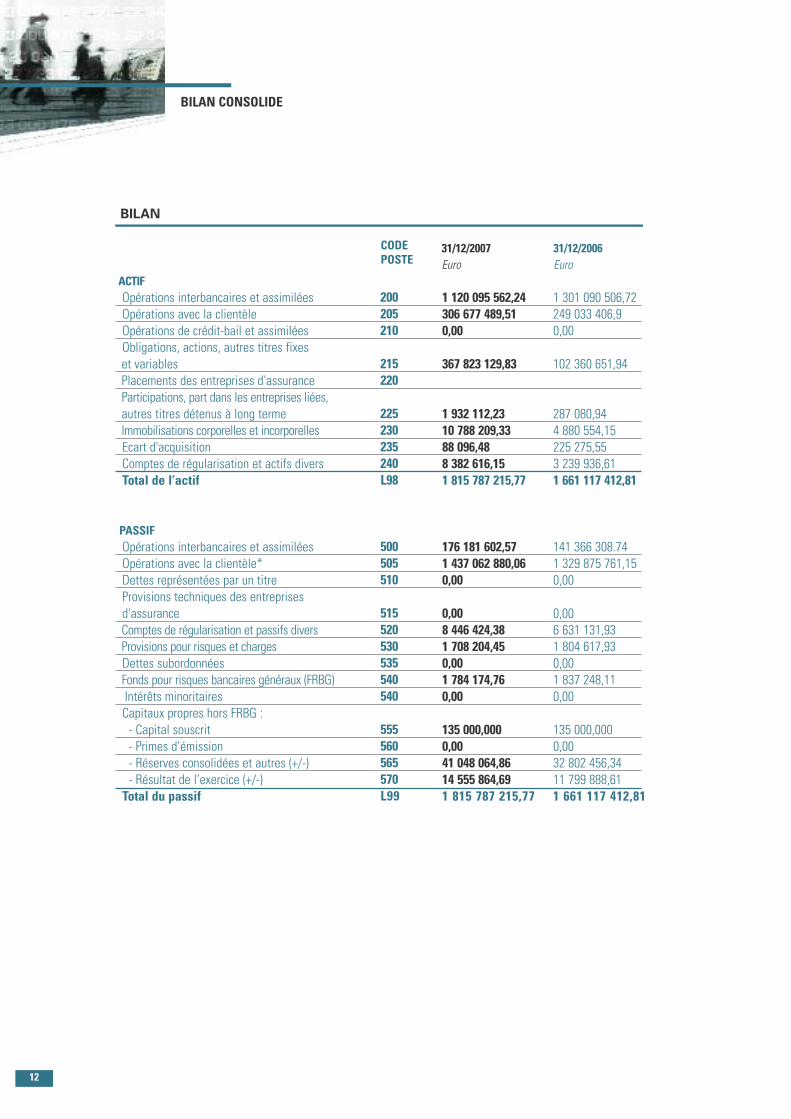

BILAN CONSOLIDE

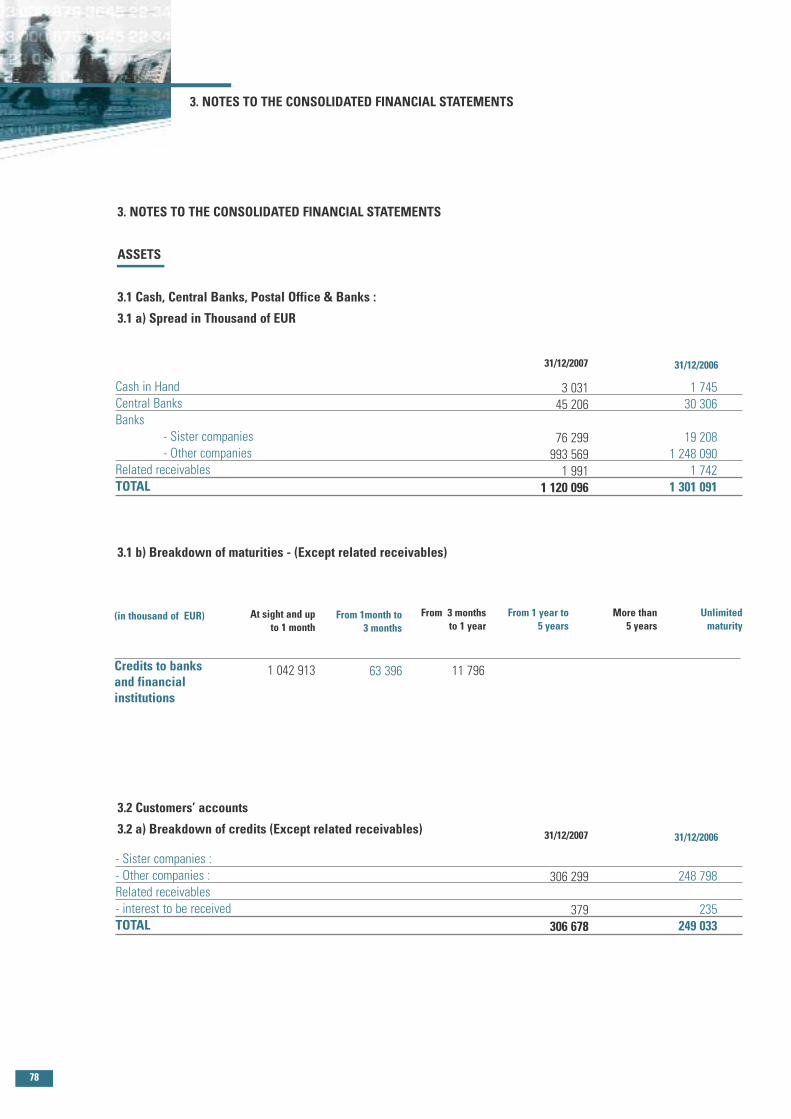

ACTIFOpérations interbancaires et assimiléesOpérations avec la clientèleOpérations de crédit-bail et assimiléesObligations, actions, autres titres fixeset variablesPlacements des entreprises d'assuranceParticipations, part dans les entreprises liées,autres titres détenus à long termeImmobilisations corporelles et incorporellesEcart d'acquisitionComptes de régularisation et actifs diversTotal de l’actif

PASSIFOpérations interbancaires et assimiléesOpérations avec la clientèle*Dettes représentées par un titreProvisions techniques des entreprisesd'assuranceComptes de régularisation et passifs diversProvisions pour risques et chargesDettes subordonnéesFonds pour risques bancaires généraux (FRBG)Intérêts minoritairesCapitaux propres hors FRBG :- Capital souscrit- Primes d’émission- Réserves consolidées et autres (+/-)- Résultat de l’exercice (+/-)Total du passif

BILAN

1 120 095 562,24306 677 489,510,00

367 823 129,83

1 932 112,2310 788 209,3388 096,488 382 616,151 815 787 215,77

176 181 602,571 437 062 880,060,00

0,008 446 424,381 708 204,450,001 784 174,760,00

135 000,0000,0041 048 064,8614 555 864,691 815 787 215,77

1 301 090 506,72249 033 406,90,00

102 360 651,94

287 080,944 880 554,15225 275,553 239 936,611 661 117 412,81

141 366 308.741 329 875 761,150,00

0,006 631 131,931 804 617,930,001 837 248,110,00

135 000,0000,0032 802 456,3411 799 888,611 661 117 412,81

31/12/2007Euro

31/12/2006Euro

200205210

215220

225230235240L98

500505510

515520530535540540

555560565570L99

CODEPOSTE

12

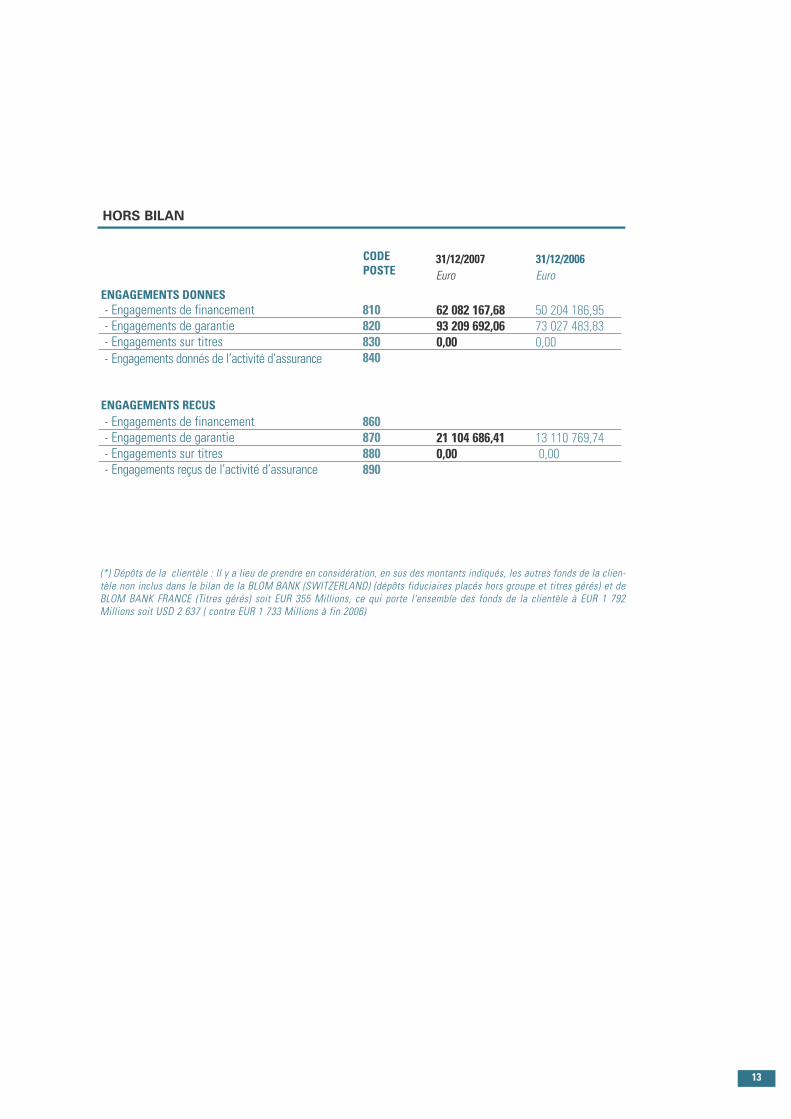

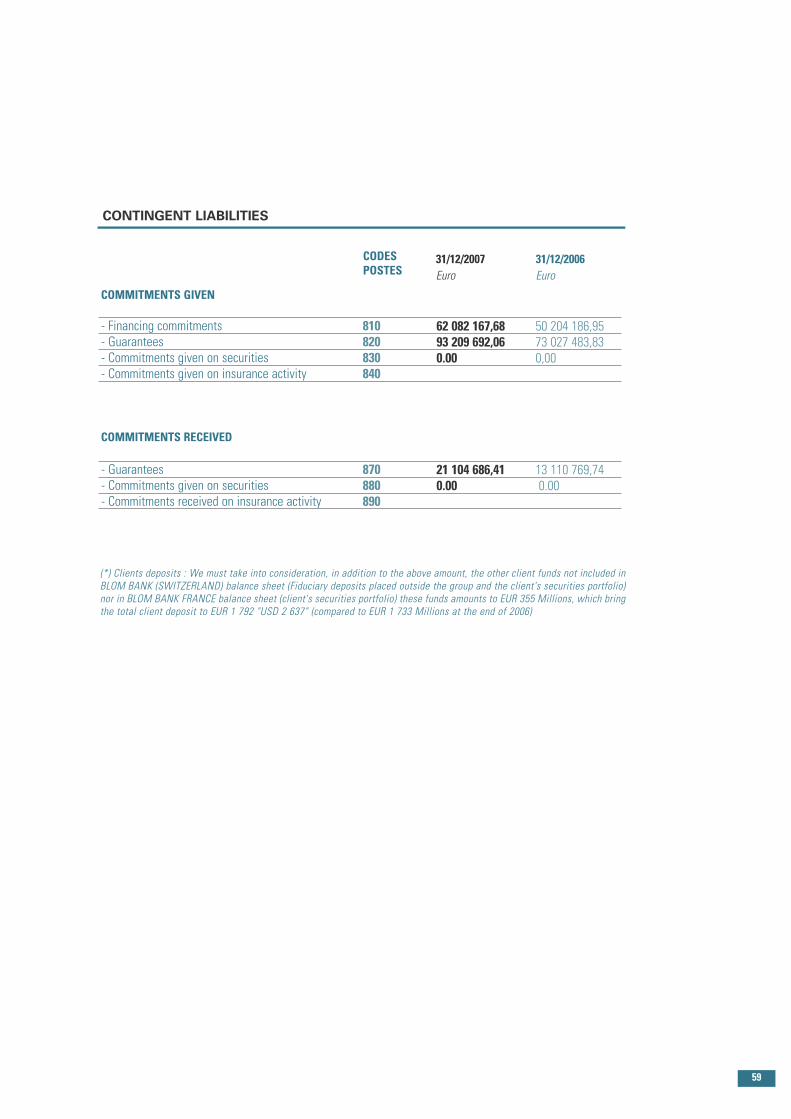

ENGAGEMENTS DONNES- Engagements de financement- Engagements de garantie- Engagements sur titres- Engagements donnés de l’activité d’assurance

ENGAGEMENTS RECUS- Engagements de financement- Engagements de garantie- Engagements sur titres- Engagements reçus de l’activité d’assurance

HORS BILAN

62 082 167,6893 209 692,060,00

21 104 686,410,00

50 204 186,9573 027 483,830,00

13 110 769,740,00

31/12/2007Euro

31/12/2006Euro

810820830840

860870880890

CODEPOSTE

(*) Dépôts de la clientèle : Il y a lieu de prendre en considération, en sus des montants indiqués, les autres fonds de la clien-tèle non inclus dans le bilan de la BLOM BANK (SWITZERLAND) (dépôts fiduciaires placés hors groupe et titres gérés) et deBLOM BANK FRANCE (Titres gérés) soit EUR 355 Millions, ce qui porte l'ensemble des fonds de la clientèle à EUR 1 792Millions soit USD 2 637 ( contre EUR 1 733 Millions à fin 2006)

13

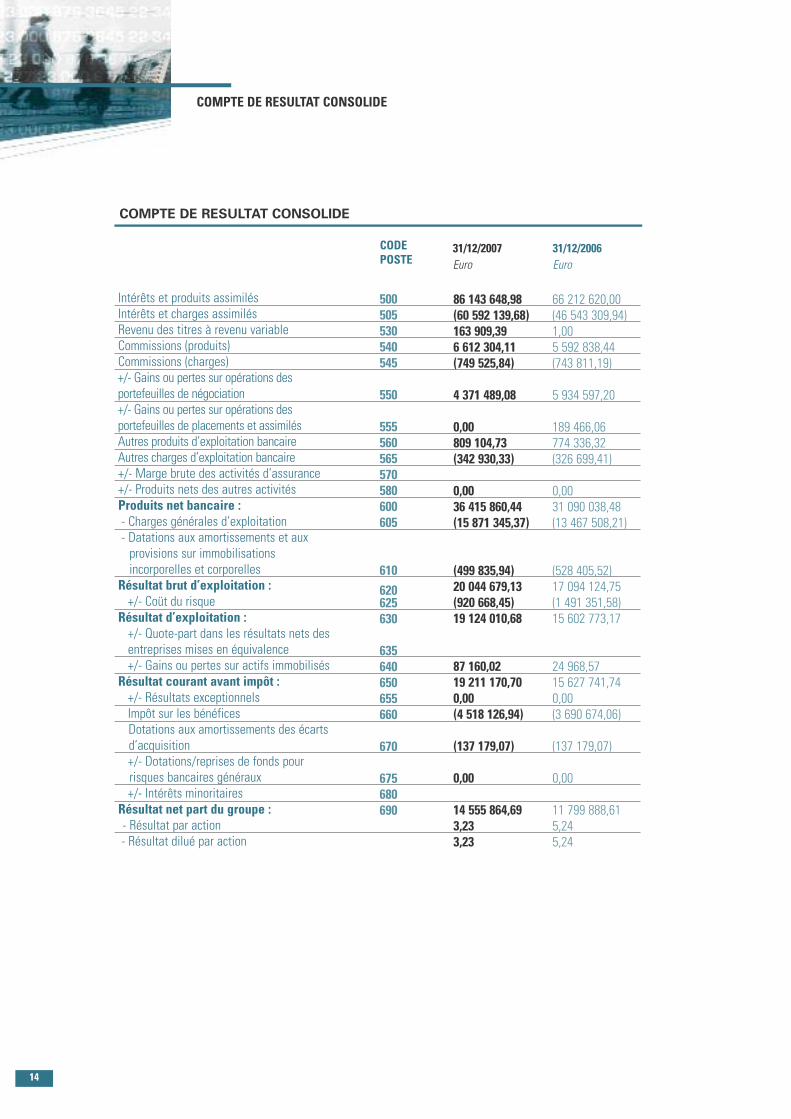

COMPTE DE RESULTAT CONSOLIDE

Intérêts et produits assimilésIntérêts et charges assimilésRevenu des titres à revenu variableCommissions (produits)Commissions (charges)+/- Gains ou pertes sur opérations desportefeuilles de négociation+/- Gains ou pertes sur opérations desportefeuilles de placements et assimilésAutres produits d’exploitation bancaireAutres charges d’exploitation bancaire+/- Marge brute des activités d’assurance+/- Produits nets des autres activitésProduits net bancaire :- Charges générales d’exploitation- Datations aux amortissements et auxprovisions sur immobilisationsincorporelles et corporelles

Résultat brut d’exploitation :+/- Coüt du risque

Résultat d’exploitation :+/- Quote-part dans les résultats nets desentreprises mises en équivalence+/- Gains ou pertes sur actifs immobilisés

Résultat courant avant impôt :+/- Résultats exceptionnelsImpôt sur les bénéficesDotations aux amortissements des écartsd’acquisition+/- Dotations/reprises de fonds pourrisques bancaires généraux+/- Intérêts minoritaires

Résultat net part du groupe :- Résultat par action- Résultat dilué par action

COMPTE DE RESULTAT CONSOLIDE

86 143 648,98(60 592 139,68)163 909,396 612 304,11(749 525,84)

4 371 489,08

0,00809 104,73(342 930,33)

0,0036 415 860,44(15 871 345,37)

(499 835,94)20 044 679,13(920 668,45)19 124 010,68

87 160,0219 211 170,700,00(4 518 126,94)

(137 179,07)

0,00

14 555 864,693,233,23

66 212 620,00(46 543 309,94)1,005 592 838,44(743 811,19)

5 934 597,20

189 466,06774 336,32(326 699,41)

0,0031 090 038,48(13 467 508,21)

(528 405,52)17 094 124,75(1 491 351,58)15 602 773,17

24 968,5715 627 741,740,00(3 690 674,06)

(137 179,07)

0,00

11 799 888,615,245,24

31/12/2007Euro

31/12/2006Euro

500505530540545

550

555560565570580600605

610

620625630

635640650655660

670

675680690

CODEPOSTE

14

RAPPORT DES COMMISSAIRES AUX COMPTES SUR LES COMPTES CONSOLIDES

16

17

20

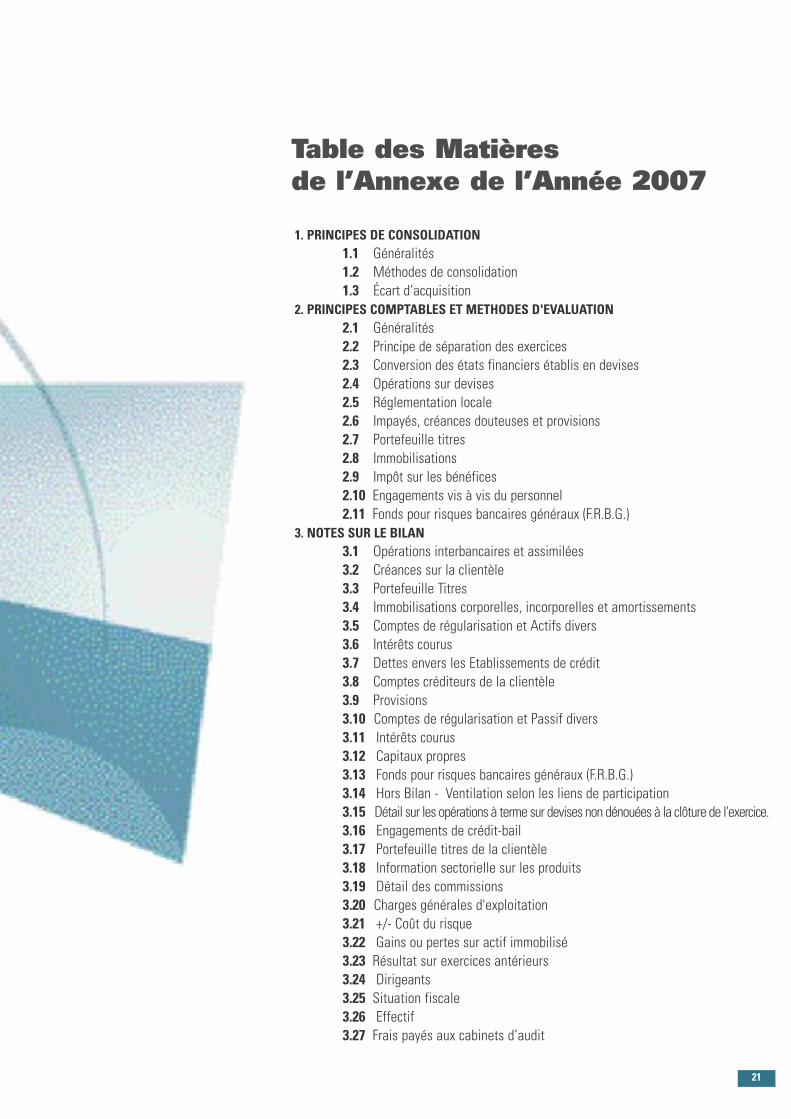

Table des Matièresde l’Annexe de l’Année 2007

1. PRINCIPES DE CONSOLIDATION1.1 Généralités1.2 Méthodes de consolidation1.3 Écart d’acquisition

2. PRINCIPES COMPTABLES ET METHODES D'EVALUATION2.1 Généralités2.2 Principe de séparation des exercices2.3 Conversion des états financiers établis en devises2.4 Opérations sur devises2.5 Réglementation locale2.6 Impayés, créances douteuses et provisions2.7 Portefeuille titres2.8 Immobilisations2.9 Impôt sur les bénéfices2.10 Engagements vis à vis du personnel2.11 Fonds pour risques bancaires généraux (F.R.B.G.)

3. NOTES SUR LE BILAN3.1 Opérations interbancaires et assimilées3.2 Créances sur la clientèle3.3 Portefeuille Titres3.4 Immobilisations corporelles, incorporelles et amortissements3.5 Comptes de régularisation et Actifs divers3.6 Intérêts courus3.7 Dettes envers les Etablissements de crédit3.8 Comptes créditeurs de la clientèle3.9 Provisions3.10 Comptes de régularisation et Passif divers3.11 Intérêts courus3.12 Capitaux propres3.13 Fonds pour risques bancaires généraux (F.R.B.G.)3.14 Hors Bilan - Ventilation selon les liens de participation3.15 Détail sur les opérations à terme sur devises non dénouées à la clôture de l'exercice.3.16 Engagements de crédit-bail3.17 Portefeuille titres de la clientèle3.18 Information sectorielle sur les produits3.19 Détail des commissions3.20 Charges générales d'exploitation3.21 +/- Coût du risque3.22 Gains ou pertes sur actif immobilisé3.23 Résultat sur exercices antérieurs3.24 Dirigeants3.25 Situation fiscale3.26 Effectif3.27 Frais payés aux cabinets d’audit

21

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

1. PRINCIPES DE CONSOLIDATION

1. PRINCIPES DE CONSOLIDATION

1.1 Généralités

Les états financiers présentés ci-après comprennent les comptes de BLOM BANKFRANCE et de ses filiales :

- BLOM BANK SWITZERLAND (Suisse)- La société « SC LOTUS SERVICES AND TRADING SRL » (Roumanie).

Toutes deux, sous contrôle exclusif, ont été consolidées, par intégration globale, du fait queleur activité se situe dans le prolongement des activités bancaires ou financières ou relèved’activités connexes au sens de l’article L.311-2 du code monétaire et financier même si,comme c’est le cas pour la société de services « LOTUS SERVICES », les comptes individuels deces entreprises sont structurés demanière différente de ceux des autres entreprises incluses dansle périmètre de consolidation, parce qu’elles appartiennent à des secteurs d’activité différents telsnotamment l’assurance, les sociétés foncières et depromotion immobilière oude services informatiques.

Les états financiers de ces deux sociétés ont été établis d’après les règles comptableslocales, les retraitements et reclassements nécessaires ont été effectués afin de lesrendre conformes aux principes énoncés dans le Règlement 91-01 modifié du Comité dela Réglementation Bancaire et 99-07 du Comité de la Réglementation Comptable et auxrègles généralement admises par la profession bancaire française et internationale.

Toute participation de BLOM BANK FRANCE dans une société dont l'activité ne constitue pas unprolongement de celle de la Banque n’est pas consolidée, si celle-ci ne fait partie des critères deconsolidation définis par le CRC 99-07.

Il est à noter par ailleurs que les comptes du groupe BLOM BANK FRANCE sont intégrésdans les comptes de la maison mère, BLOM BANK, suivant la méthode de l’intégrationglobale.

1.2 Méthodes de consolidation

C'est la méthode de l'intégration globale qui a été utilisée pour l'établissement desétats financiers, BLOM BANK FRANCE contrôlant à plus de 50% BLOM BANKSWITZERLAND (Suisse) et SC LOTUS SERVICES.

23

La méthode de l'intégration globale consiste à substituer à la valeur des titres en portefeuilledans les livres de la société mère chacun des éléments de l'actif et du passif de la filiale puisà éliminer toutes les opérations réciproques entre la société mère et la filiale. La part desintérêts minoritaires dans la situation nette et dans le résultat est inscrite distinctement aubilan et au compte de résultat consolidé.

1.3 Écart d’acquisition

Le poste "Écart d’acquisition" figurant à l'actif représente l'écart positif dégagé entre le prix derevient des titres et la part de l'actif net comptable qui leur correspond à la date d'acquisition.Ces écarts sont amortis linéairement sur 20 ans par dotations au compte de résultat.Cet écart d’acquisition a été figé aux cours de change en vigueur aux dates d’acquisition.L’écart d’acquisition a été calculé de la manière suivante :

Il est à noter que cet écart d’acquisition (goodwill), qui reflète l'écart existant à la dated'acquisition, n'est pas modifié par les résultats réalisés postérieurement à cette date, cesderniers venant s'intégrer aux fonds propres consolidés. Aussi quel que soit le niveau futur deces fonds propres, et conformément aux principes comptables, l’écart d’acquisition est amortide manière linéaire.

Cet écart d’acquisition est amorti sur une période de 20 ans et l’amortissement est exercé surla valeur figée en Euros au cours historique.

L’écart de conversion résultant de la différence entre le montant du début de l’exercice (aprèsamortissements) figé aux cours historiques et la contre-valeur au cours de fin d’exercice estintégré aux réserves consolidées. Cet écart de conversion à fin 2007 s’élève à EUR 82 889,52(négatif).

A. prix d'achat de 20.000 actionsBLOM BANK (SWITZERLAND) (100%) =

B. quote-part retraitée correspondante(100%) au 31/12/2007 dans les fonds propres

La différence étant desoit convertie en EUR aux cours d’origine :

1. PRINCIPES DE CONSOLIDATION

2. PRINCIPES COMPTABLES ET METHODES D'EVALUATION

CHF

-CHFCHFEUR

29 730 192,80

25 192 518,584 537 674,222 743 581,33

Amortissements cumulés de 1988 à 2006Amortissement pour 2007soit un écart d’acquisition au 31.12.2007 (après amortissements) de

EUREUREUR

2 518 305,78137 179,0788 096,48

24

2. PRINCIPES COMPTABLES ET METHODES D'EVALUATION

2.1 Généralités

Comme énoncé ci-dessus, les états financiers sont élaborés et présentés suivant les prescriptionsdes règlements CRB 91-01 modifié et CRC 99-07 et aux dispositions relatives aux états publiables(Règlement N°2000-04). Les règles appliquées pour l'établissement du Bilan et du Compte deRésultat suivent les normes comptables de la profession bancaire en France. Ces comptes ontété arrêtés dans le respect des règles de prudence, de la permanence des méthodes d'évaluationet de la continuité de l'exploitation.Les comptes consolidés comprennent pour la première fois les nouvelles succursalesroumaines qui ont intégré la société en date du 1er décembre 2007.

2.2 Principe de séparation des exercices

Les charges et les produits sont, d'une manière générale, enregistrés selon le principe dela spécialisation des exercices, à l'exception de certaines commissions retenues à leur encaissement.Il s'agit en particulier de certaines commissions sur les crédits documentaires et égalementde commissions sur les dépôts fiduciaires.

2.3 Conversion des états financiers établis en devises

Lorsqu’ils sont exprimés en devises, le bilan et le hors bilan des sociétés consolidées sont convertis surla base des cours de change officiels à la date de clôture.Les postes du compte de résultat sont convertis sur la base du cours de change moyen de l’exercice.La différence de valorisation des résultats de l’exercice entre le cours moyen et le cours de clôture estportée dans les capitaux propres dans la rubrique « Ecarts de conversion ».La différence de conversion sur le capital, les réserves, le report à nouveau et le résultat qui résulte del’évolution des cours de change est également portée dans la rubrique « Ecarts de conversion » desréserves consolidées.Ainsi, les écarts relatifs à la conversion des dotations en capital ne sont pas compris dans les résultatsmais sont portés parmi les réserves.Lorsque la réglementation locale impose de comptabiliser en résultat les écarts de change relatifs auxdotations en capital ou ceux relatifs à d’autres positions de change structurelles, un retraitementest opéré pour neutraliser l’effet en résultat. Ce retraitement est opéré par l’imputation d’unécart de conversion rattaché aux dotations en capital pour les positions structurelles liées à l’allocationen fonds propres des succursales et rattaché aux comptes de régularisation pour les autres positions dechange structurelles.Ces écarts de conversion sur les positions de change dites structurelles, lorsqu’ils sont défavorables,doivent faire l’objet d’un provisionnement lorsque la dépréciation peut être considérée commeirréversible et la perte en résultant comme définitive.

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

25

2. PRINCIPES COMPTABLES ET METHODES D'EVALUATION

2.4 Opérations sur devises

Les positions de change sont évaluées mensuellement au cours officiel de fin de période ; lesprofits et les pertes qui en découlent sont enregistrés dans les résultats. Les résultats desopérations de change d'arbitrage comptant contre terme sont enregistrés prorata temporis.

2.5 Réglementation locale

Pour répondre à des contraintes réglementaires locales, les succursales des Emirats ArabesUnis doivent constituer une réserve légale par appropriation de 10 % du résultat lors de chaqueexercice, soit 3 883 552 AED (718 milliers EUR) au titre de l’exercice 2007.En outre, sur demande de la banque centrale des E.A.U, une réserve correspondant à 2 % descrédits productifs doit être maintenue dans les comptes de la succursale. Cette réserve estégalement constituée par appropriation du résultat. La part du résultat approprié au titre del’exercice 2007 est de 1 057 183 AED (196 milliers EUR) et le montant total de cette réserveatteint AED 10 540 894 (1 950 milliers EUR).Dans les comptes sociaux et consolidés de BLOM BANK FRANCE, l’intégralité du résultat estappréhendée. Une dotation en capital est comptabilisée lors de l’approbation des comptes pourrépondre à la réglementation locale.

2.6 Impayés, créances douteuses et provisions

Les créances impayées depuis moins de trois mois restent classées à leur poste d'origine. Lescréances de toute nature présentant un risque de non recouvrement total ou partiel ou présentant uncaractère contentieux sont transférées en Créances Douteuses et Litigieuses et sont ajoutées aux"Comptes Ordinaires Débiteurs" l'ensemble figurant au Bilan sous cette dernière dénomination.Ces créances font l'objet de dotations aux provisions, par le débit du compte de résultat. Les intérêtsqui continuent à être comptabilisés sur ces créances sont provisionnés en totalité.Toutes ces provisions sont déduites des créances à l'actif.Vous trouverez dans les notes sur le bilan le montant des encours et des provisions.La présentation des encours douteux est effectuée en application du règlement CRC 2002-03, modifié parle règlement 2005-03 du Comité de la Réglementation Comptable, relatif au traitement comptabledu risque de crédit.BLOM BANK FRANCE ne recense aucun crédit restructuré à des conditions hors marché.Les provisions sont déterminées au cas par cas, en tenant compte pour l'évaluation du risquede la qualité du débiteur, ainsi que, notamment pour les crédits immobiliers, de l'estimationprudente des différentes garanties détenues (actifs immobiliers, etc), des dépôts nantis engarantie, et de la volonté de la banque de poursuivre à leur terme les opérations en cours desa clientèle afin de préserver au mieux les intérêts de la banque.

Les risques pays (de faible importance) sont provisionnés suivant les taux généralement pratiqués parla profession bancaire dans les différentes places (France et Suisse).

26

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

2.7 Portefeuille titres

Conformément au règlement CRB 90-01, modifié par les règlements CRB 95-04, CRC 2000-02, CRC 2002-01 et CRC 2005-01.

Les titres sont classifiés en fonction de:— leur nature : effets publics (bons du Trésor et titres assimilés), obligations et autres titresà revenu fixe (titres de créances négociables et titres du marché interbancaire), actions etautres titres à revenu variable— leur portefeuille de destination : transaction, placement, investissement, correspondant àl’objet économique de leur détention. Pour chaque catégorie de portefeuille, ils sont soumisà des règles d’évaluation similaires qui sont les suivantes

Titres de transaction

Ce sont les titres négociables sur un marché actif qui sont acquis dans une intention derevente à cout terme. Ils font l’objet d’une évaluation sur la base de leur valeur de marché àla date de clôture de l’exercice. Le solde des gains et pertes latents ainsi constaté, de mêmeque le solde des gains et pertes réalisés sur cession des titres est porté au compte de résul-tat net des opérations financières. Les coupons encaissés sur les titres à revenu fixe duportefeuille de transaction sont classés dans le compte de résultat au sein de la rubriqueRésultats nets d’intérêts relatifs aux obligations et autres titres à revenu fixe.

Titres de placement

Sont considérés comme des titres de placement les titres qui ne sont inscrits ni parmi lestitres de transaction, ni parmi les titres d’investissement.

Actions et autres titres à revenu variable

Les actions sont inscrites au bilan à leur coût d’achat hors frais d’acquisition ou à leur valeurd’apport. À la clôture de l’exercice, elles sont évaluées par rapport à leur valeur probable denégociation. Dans le cas des titres cotés, celle-ci est déterminée en fonction du cours debourse le plus récent. Seules les moins-values latentes sont comptabilisées par l’inscriptiond’une provision pour dépréciation du portefeuille titres. Les revenus de dividendes attachésaux actions de placement sont portés au compte de résultat dans la rubrique Revenus destitres à revenu variable.

27

2. PRINCIPES COMPTABLES ET METHODES D'EVALUATION

Obligations et autres titres à revenu fixe

Ces titres sont inscrits au bilan à leur prix d’acquisition hors frais d’acquisition, et concernantles obligations, hors intérêts courus non échus à la date d’acquisition. Les différences entre lesprix d’acquisition et les valeurs de remboursement (primes si elles sont positives, décotes si ellessont négatives) sont enregistrées au compte de résultat sur la durée de vie des titres concernés. Lesintérêts courus à percevoir attachés aux obligations et autres titres à revenu fixe de placement sontportés dans un compte de créances rattachées en contrepartie de la rubrique Produits d’intérêtsrelatifs aux obligations et autres titres à revenu fixe du compte de résultat.

À la clôture de l’exercice, les titres sont estimés sur la base de leur valeur probable de négociationet, dans le cas des titres cotés, des cours de bourse les plus récents. Les plus-values latentes ne sontpas comptabilisées et les moins-values latentes donnent lieu à la constitution d’une provision pourdépréciation du portefeuille titres, dont le calcul tient compte des gains provenant des éventuellesopérations de couverture effectuées.

Titres d’investissement

Il s’agit de titres à revenu fixe que l’on a l’intention de détenir de façon durable et pour lesquelson dispose de moyens permettant :- soit de se protéger de façon permanente contre une dépréciation des titres due aux variationsde taux d’intérêt au moyen d’une couverture par des instruments financiers à terme de tauxd’intérêt,- soit de conserver effectivement les titres durablement par l’obtention de ressources,incluant les fonds propres disponibles, globalement adossées et affectées au financementde ces titres.Les titres d’investissement sont comptabilisés de manière identique aux titres de placement.Toutefois, à la clôture de l’exercice, les moins-values latentes ne donnent pas lieu à la constitutiond’une provision pour dépréciation du portefeuille titres, sauf s’il existe une forte probabilité decession des titres à court terme, ou s’il existe des risques de défaillance de l’émetteur des titres.

28

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

Titres de l’activité de portefeuille

Il s’agit d’investissements réalisés avec pour seul objectif d’en retirer un gain en capital àmoyen terme sans intention d’investir durablement dans le développement de l’entreprise émet-trice, ni de participer activement à sa gestion. Ces titres sont inscrits au bilan au plus bas de leurcoût historique ou de leur valeur d’utilité (cette dernière étant déterminée en tenant compte desperspectives générales d’évolution de l’émetteur et de la durée résiduelle de détention). Lavaleur d’utilité des titres cotés est principalement déterminée par référence au cours de boursesur une période suffisamment longue. Les plus-values latentes ne sont pas comptabilisées et lesmoins-values latentes donnent lieu à la constitution d’une provision pour dépréciation duportefeuille titres.

Titres de participation, parts dans les entreprises liées et autres titres détenus à long terme

Il s’agit d’une part

A -des Titres de participation et parts dans les entreprises liées dont la possession durableest estimée utile à l’activité de l’entreprise, et notamment ceux répondant aux critèressuivants

- titres de sociétés ayant des administrateurs ou des dirigeants communs avec la sociétédétentrice, dans des conditions qui permettent l’exercice d’une influence sur l’entreprisedont les titres sont détenus

- titres de sociétés appartenant à un même groupe contrôlé par des personnes physiques oumorales exerçant un contrôle sur l’ensemble et faisant prévaloir une unité de décision

- titres représentant plus de 10 % des droits dans le capital émis par un établissement decrédit ou par une société dont l’activité se situe dans le prolongement de celle du Groupe.

Il s’agit d’autre part

B -des Autres titres détenus à long terme, constitués par les investissements réalisés sousforme de titres par l’entreprise dans l’intention de favoriser le développement de relationsprofessionnelles durables en créant un lien privilégié avec l’entreprise émettrice, sanstoutefois exercer une influence dans sa gestion en raison du faible pourcentage des droitsde vote qu’ils représentent.

Les titres de participation, parts dans les entreprises liées et autres titres détenus à longterme sont comptabilisés à leur coût d’achat hors frais d’acquisition. Les revenus de dividendesattachés à ces titres sont portés au compte de résultat dans la rubrique Revenus des titres à revenuvariable.

29

2. PRINCIPES COMPTABLES ET METHODES D'EVALUATION

À la clôture de l’exercice, les titres de participation et parts dans les entreprises liées sont évalués àleur valeur d’utilité représentative du prix que la société accepterait de décaisser pour obtenir cestitres si elle avait à les acquérir compte tenu de son objectif de détention. Cette valeur estestimée par référence à différents critères tel que les capitaux propres, la rentabilité, les coursmoyens de bourse sur une période suffisamment longue; les plus-values latentes ne sont pascomptabilisées et les moins-values latentes donnent lieu à la constitution d’une provision pourdépréciation du portefeuille titres.

2.8 Immobilisations

Les immobilisations sont enregistrées à leur prix d'acquisition et sont amorties en fonction de leurdurée de vie estimée, selon le mode linéaire. Le fond commercial est également amorti sur unebase linéaire ne dépassant pas cinq ans. Au cas où la dépréciation s'avérerait supérieure auxamortissements pratiqués, la correction de l'actif immobilisé serait constatée par une provision.

Les durées d'amortissement constatées dans le groupe sont les suivantes :- pour l’immobilier construit, entre 35 et 45 ans.- pour le mobilier, entre 8 et 10 ans.- pour les machines de bureaux et le matériel informatique entre 5 et 8 ans.- pour le matériel divers, en 5 ou 10 ans.- pour les agencements et installations, en 10 ans (ou 5 ans pour les éléments légers).- pour les logiciels, entre 3 et 5 ans.

2.9 Impôt sur les bénéfices

Il est comptabilisé un impôt différé lorsqu'il est constaté des différences temporaires nées dedécalages d'exercice entre la constatation comptable d'un produit ou d'une charge et leurprise en compte pour le résultat fiscal. L'impôt différé comprend aussi les déficits fiscauxreportables lorsque leur imputation sur les résultats futurs apparaît probable.En cas de changement de taux d'impôt, les impositions différées sont ajustées au nouveau tauxen vigueur sur l'exercice où le changement est connu et l'ajustement imputé en compte derésultat.Par contre, il n'est pas constaté d'impôt de distribution sur les dividendes lorsque la décisionde distribution n'est pas encore connue à la clôture de l'exercice.

2.10 Engagements vis à vis du personnel

Des indemnités de fin de carrière prévues par les Conventions collectives ou contractuelles ontété comptabilisées en fonction des droits acquis au 31 décembre de chaque année.

30

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

2.11 Fonds pour risques bancaires généraux (F.R.B.G.)

Ces fonds sont les montants que les dirigeants décident d'affecter à la couverture de telsrisques lorsque des raisons de prudence l'imposent eu égard aux risques inhérents auxopérations bancaires. Ces fonds ne sont pas constitués en vue de faire face à des chargesou risques qui ont un caractère probable et qui ont été clairement identifiés. Ils ne répondentdonc pas aux critères d'une provision pour risques, ni à ceux d’une véritable réserve, étantdotés et repris par le débit ou crédit du compte de résultat et non, comme pour les réserves,par l’affectation des résultats sur décision de l’assemblée générale.Les provisions excédentaires ayant un caractère de réserve constituées par les filialesétrangères sont reclassées en "Fonds pour Risques Bancaires Généraux" dès lors que lesdispositions comptables en vigueur dans le pays d'accueil de la filiale ne prévoient pasl'existence d'un tel poste. Dans ce cas, si cela est nécessaire, un impôt différé est calculé,et vient diminuer le résultat de l'exercice. Le FRBG comme la dotation (ou reprise) nette del'exercice apparaissent sur une ligne séparée du bilan et du compte de résultat.

31

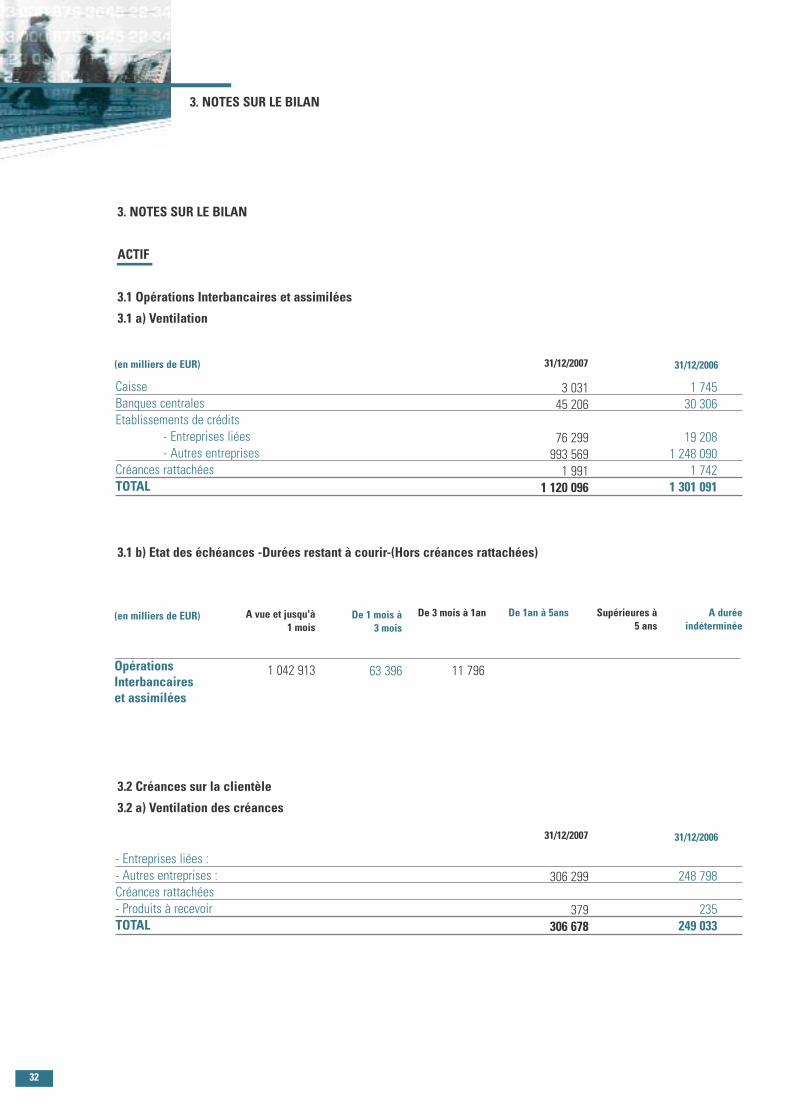

3. NOTES SUR LE BILAN

3. NOTES SUR LE BILAN

ACTIF

3.1 Opérations Interbancaires et assimilées

3.1 a) Ventilation

3.1 b) Etat des échéances -Durées restant à courir-(Hors créances rattachées)

3.2 Créances sur la clientèle

3.2 a) Ventilation des créances

CaisseBanques centralesEtablissements de crédits

- Entreprises liées- Autres entreprises

Créances rattachéesTOTAL

1 74530 306

19 2081 248 090

1 7421 301 091

OpérationsInterbancaireset assimilées

A vue et jusqu'à1 mois

De 1 mois à3 mois

De 1an à 5ans Supérieures à5 ans

De 3 mois à 1an A duréeindéterminée

(en milliers de EUR)

1 042 913 63 396 11 796

31/12/200631/12/2007

3 03145 206

76 299993 5691 991

1 120 096

- Entreprises liées :- Autres entreprises :Créances rattachées- Produits à recevoirTOTAL

248 798

235249 033

31/12/200631/12/2007

306 299

379306 678

(en milliers de EUR)

32

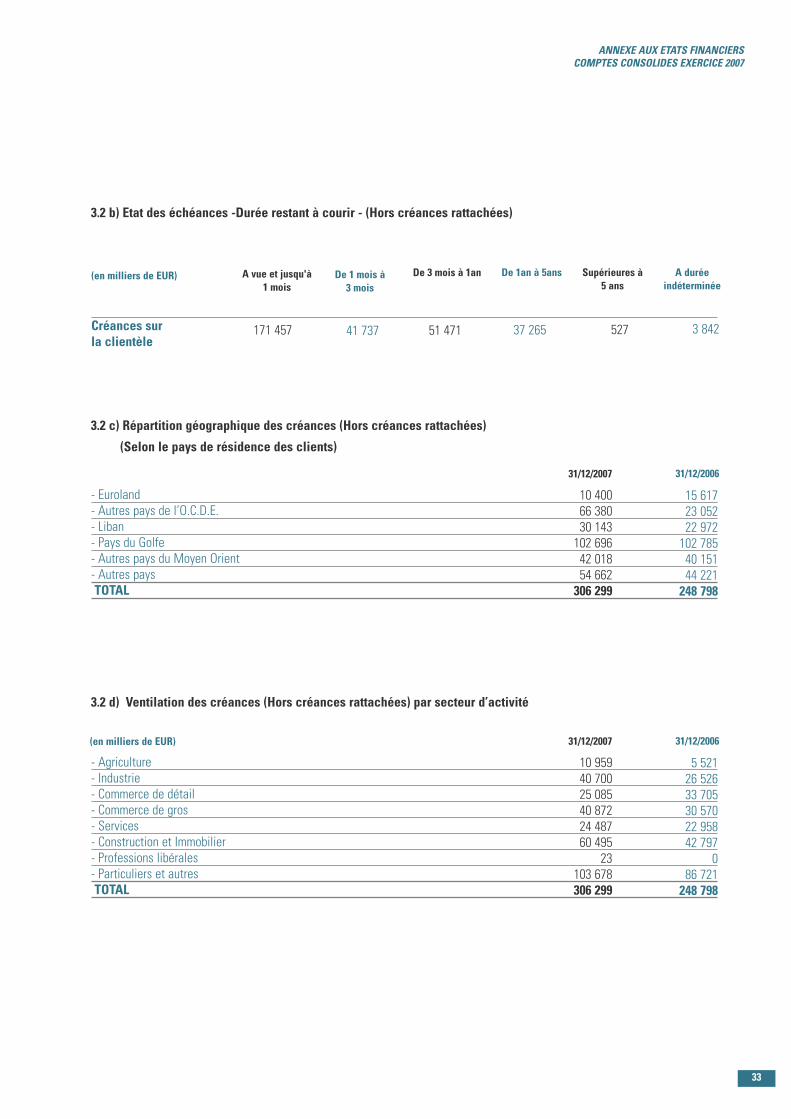

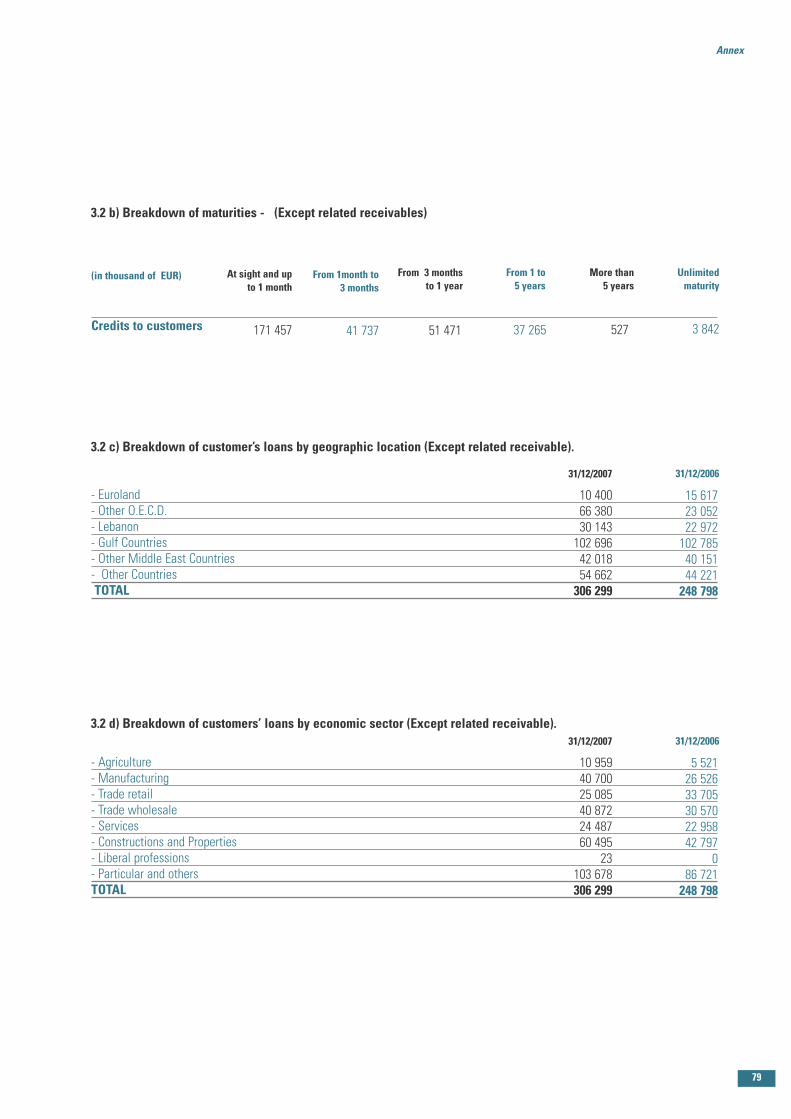

3.2 b) Etat des échéances -Durée restant à courir - (Hors créances rattachées)

3.2 c) Répartition géographique des créances (Hors créances rattachées)

(Selon le pays de résidence des clients)

3.2 d) Ventilation des créances (Hors créances rattachées) par secteur d’activité

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

Créances surla clientèle

A vue et jusqu'à1 mois

De 1 mois à3 mois

De 1an à 5ans Supérieures à5 ans

De 3 mois à 1an A duréeindéterminée

(en milliers de EUR)

171 457 41 737 51 471 37 265 527 3 842

- Euroland- Autres pays de l’O.C.D.E.- Liban- Pays du Golfe- Autres pays du Moyen Orient- Autres paysTOTAL

15 61723 05222 972102 78540 15144 221248 798

31/12/2007 31/12/2006

10 40066 38030 143102 69642 01854 662306 299

- Agriculture- Industrie- Commerce de détail- Commerce de gros- Services- Construction et Immobilier- Professions libérales- Particuliers et autresTOTAL

5 52126 52633 70530 57022 95842 797

086 721248 798

31/12/2007 31/12/2006

10 95940 70025 08540 87224 48760 495

23103 678306 299

(en milliers de EUR)

33

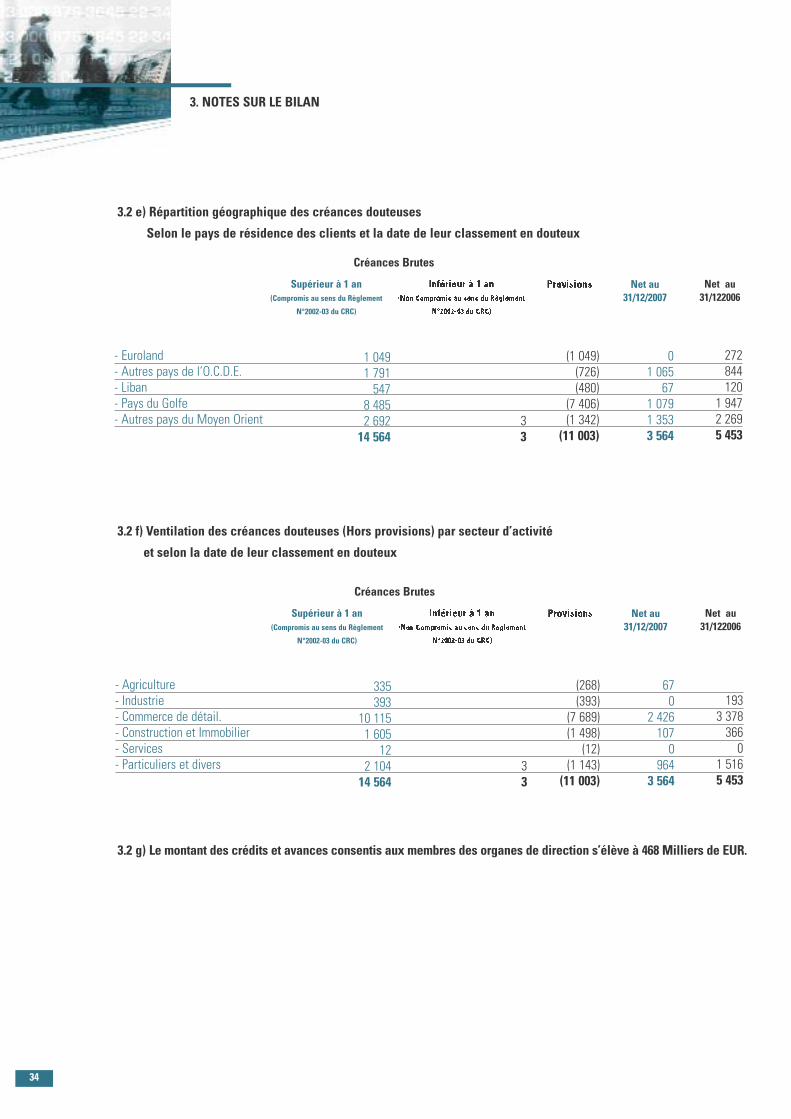

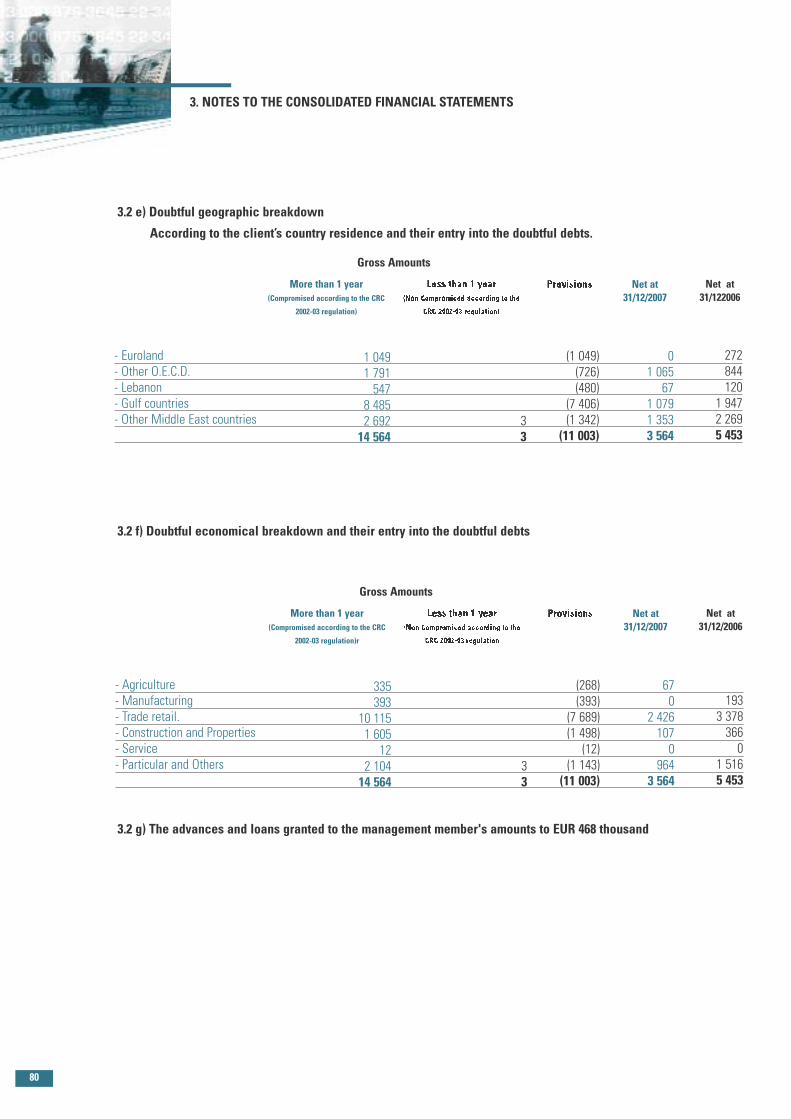

3.2 e) Répartition géographique des créances douteuses

Selon le pays de résidence des clients et la date de leur classement en douteux

3.2 f) Ventilation des créances douteuses (Hors provisions) par secteur d’activité

et selon la date de leur classement en douteux

3.2 g) Le montant des crédits et avances consentis aux membres des organes de direction s’élève à 468 Milliers de EUR.

- Euroland- Autres pays de l’O.C.D.E.- Liban- Pays du Golfe- Autres pays du Moyen Orient

3. NOTES SUR LE BILAN

Créances Brutes

Supérieur à 1 an(Compromis au sens du Règlement

N°2002-03 du CRC)

33

1 0491 791547

8 4852 69214 564

(1 049)(726)(480)

(7 406)(1 342)

(11 003)

Net au31/12/2007

01 065

671 0791 3533 564

Net au31/122006

272844120

1 9472 2695 453

- Agriculture- Industrie- Commerce de détail.- Construction et Immobilier- Services- Particuliers et divers

Créances Brutes

Supérieur à 1 an(Compromis au sens du Règlement

N°2002-03 du CRC)

33

335393

10 1151 605

122 10414 564

(268)(393)

(7 689)(1 498)

(12)(1 143)

(11 003)

Net au31/12/2007

670

2 4261070

9643 564

Net au31/122006

1933 3783660

1 5165 453

34

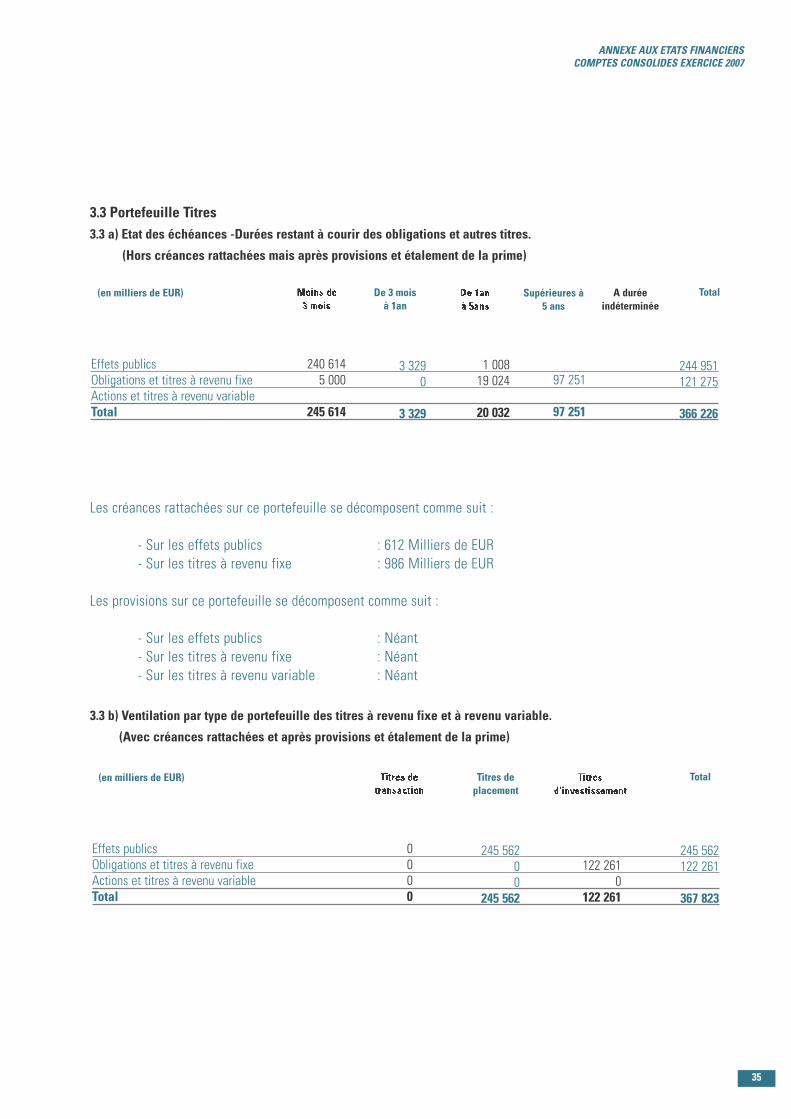

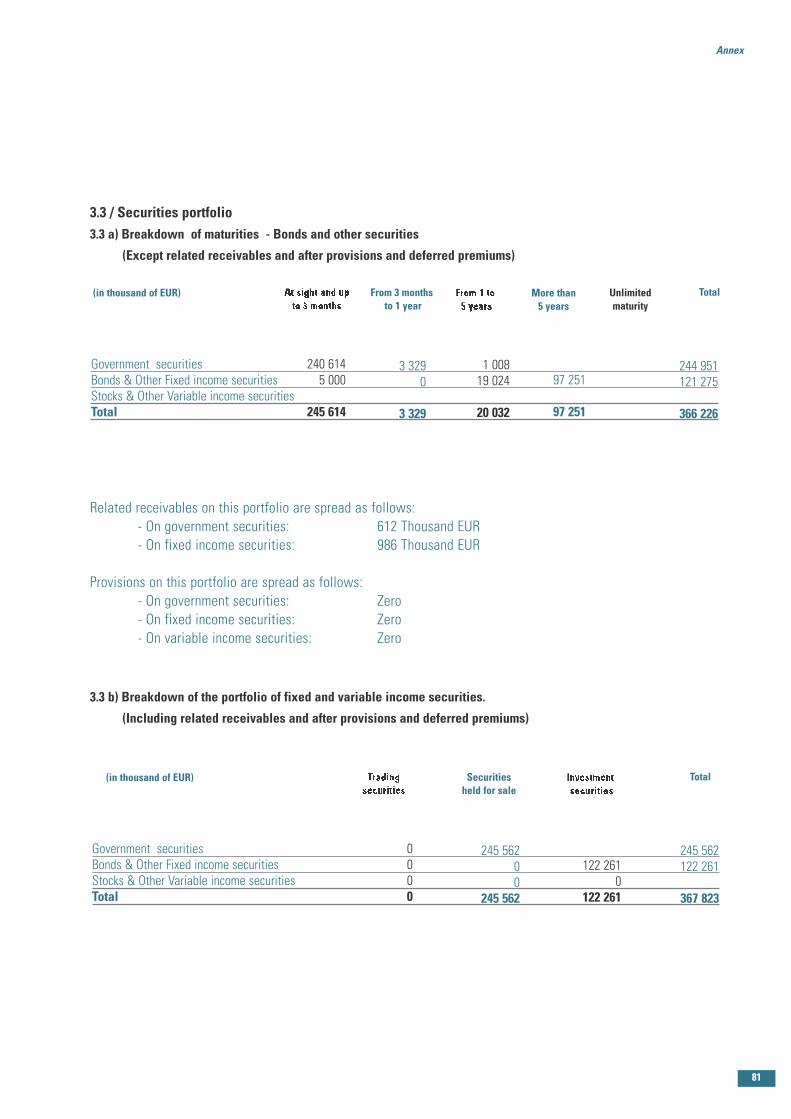

3.3 Portefeuille Titres3.3 a) Etat des échéances -Durées restant à courir des obligations et autres titres.

(Hors créances rattachées mais après provisions et étalement de la prime)

Les créances rattachées sur ce portefeuille se décomposent comme suit :

- Sur les effets publics : 612 Milliers de EUR- Sur les titres à revenu fixe : 986 Milliers de EUR

Les provisions sur ce portefeuille se décomposent comme suit :

- Sur les effets publics : Néant- Sur les titres à revenu fixe : Néant- Sur les titres à revenu variable : Néant

3.3 b) Ventilation par type de portefeuille des titres à revenu fixe et à revenu variable.

(Avec créances rattachées et après provisions et étalement de la prime)

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

Effets publicsObligations et titres à revenu fixeActions et titres à revenu variableTotal

244 951121 275

366 226

Supérieures à5 ans

A duréeindéterminée

1 00819 024

20 032

De 3 moisà 1an

Total

97 251

97 251

3 3290

3 329

240 6145 000

245 614

(en milliers de EUR)

Effets publicsObligations et titres à revenu fixeActions et titres à revenu variableTotal

245 562122 261

367 823

122 2610

122 261

Titres deplacement

Total

245 56200

245 562

0000

(en milliers de EUR)

35

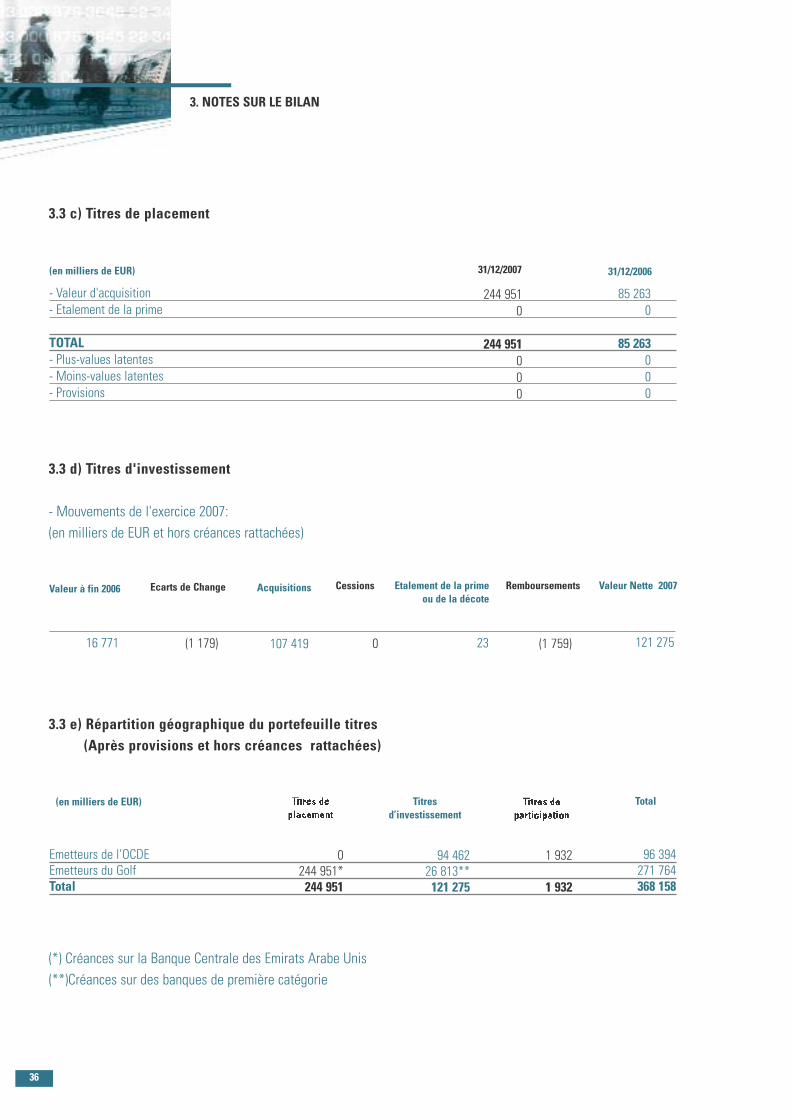

3.3 c) Titres de placement

3.3 d) Titres d'investissement

- Mouvements de l'exercice 2007:(en milliers de EUR et hors créances rattachées)

3.3 e) Répartition géographique du portefeuille titres(Après provisions et hors créances rattachées)

(*) Créances sur la Banque Centrale des Emirats Arabe Unis(**)Créances sur des banques de première catégorie

3. NOTES SUR LE BILAN

- Valeur d'acquisition- Etalement de la prime

TOTAL- Plus-values latentes- Moins-values latentes- Provisions

85 2630

85 263000

31/12/200631/12/2007

244 9510

244 951000

Ecarts de Change Acquisitions Etalement de la primeou de la décote

RemboursementsCessions Valeur Nette 2007Valeur à fin 2006

(1 179) 107 419 016 771 23 (1 759) 121 275

Emetteurs de l’OCDEEmetteurs du GolfTotal

Titresd’investissement

Total(en milliers de EUR)

0244 951*244 951

94 46226 813**121 275

1 932

1 932

96 394271 764368 158

(en milliers de EUR)

36

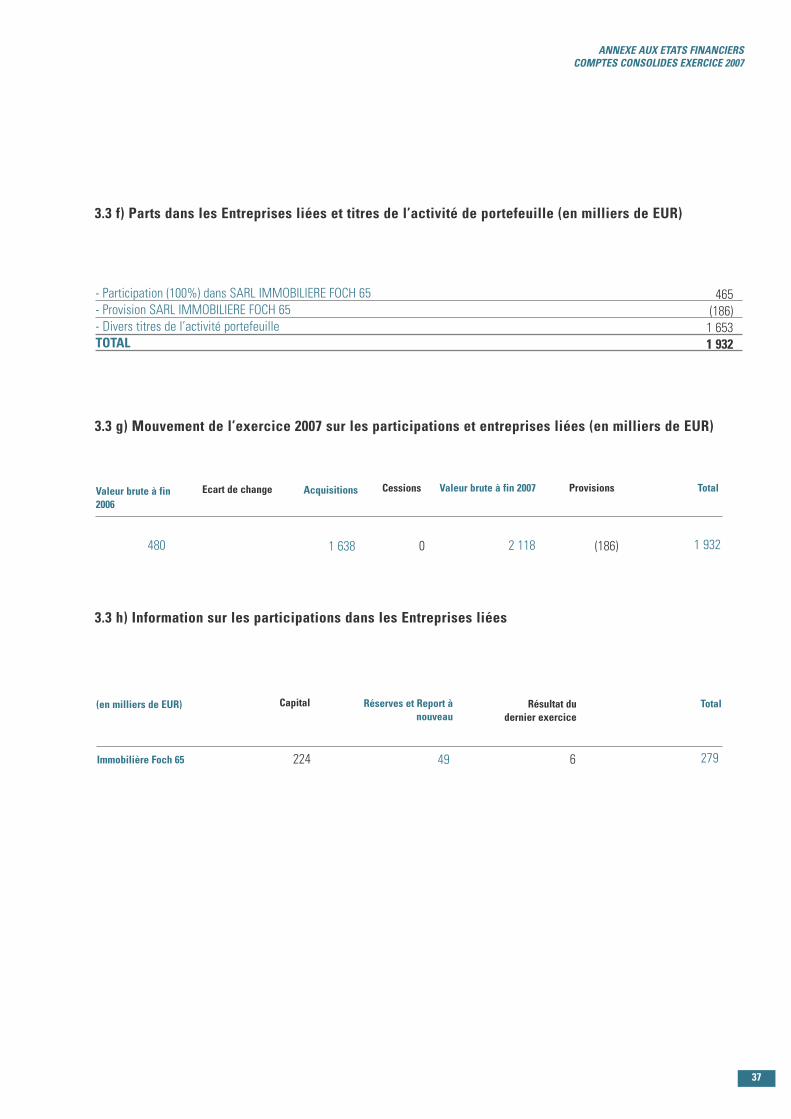

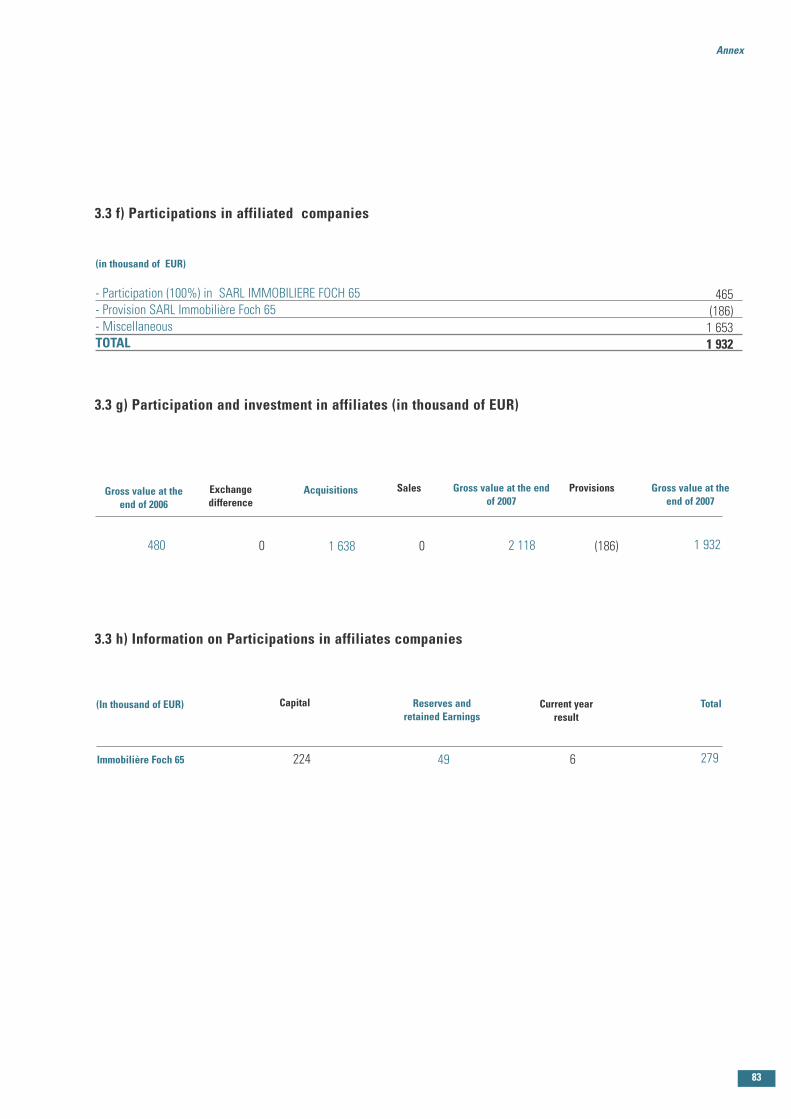

3.3 f) Parts dans les Entreprises liées et titres de l’activité de portefeuille (en milliers de EUR)

3.3 g) Mouvement de l’exercice 2007 sur les participations et entreprises liées (en milliers de EUR)

3.3 h) Information sur les participations dans les Entreprises liées

- Participation (100%) dans SARL IMMOBILIERE FOCH 65- Provision SARL IMMOBILIERE FOCH 65- Divers titres de l’activité portefeuilleTOTAL

465(186)1 6531 932

Ecart de change Acquisitions Valeur brute à fin 2007 ProvisionsCessions TotalValeur brute à fin2006

1 638 0480 2 118 (186) 1 932

Capital Réserves et Report ànouveau

Résultat dudernier exercice

(en milliers de EUR)

224 49 6 279Immobilière Foch 65

Total

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

37

3. NOTES SUR LE BILAN

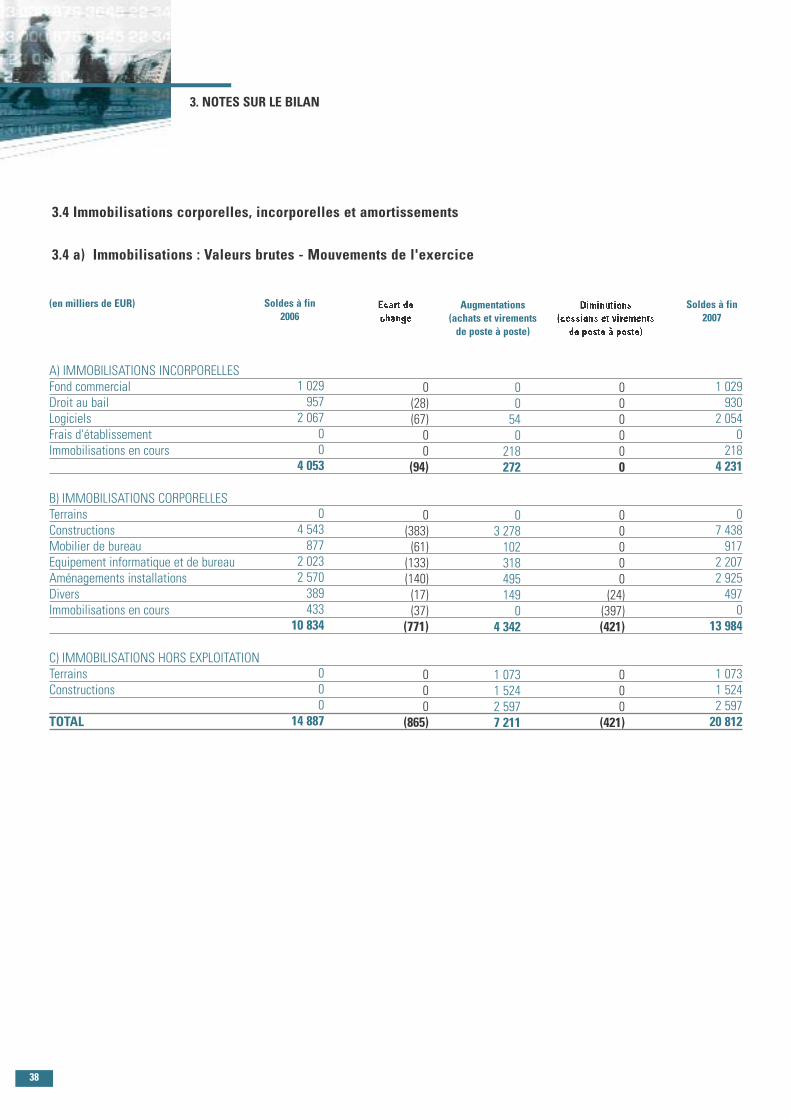

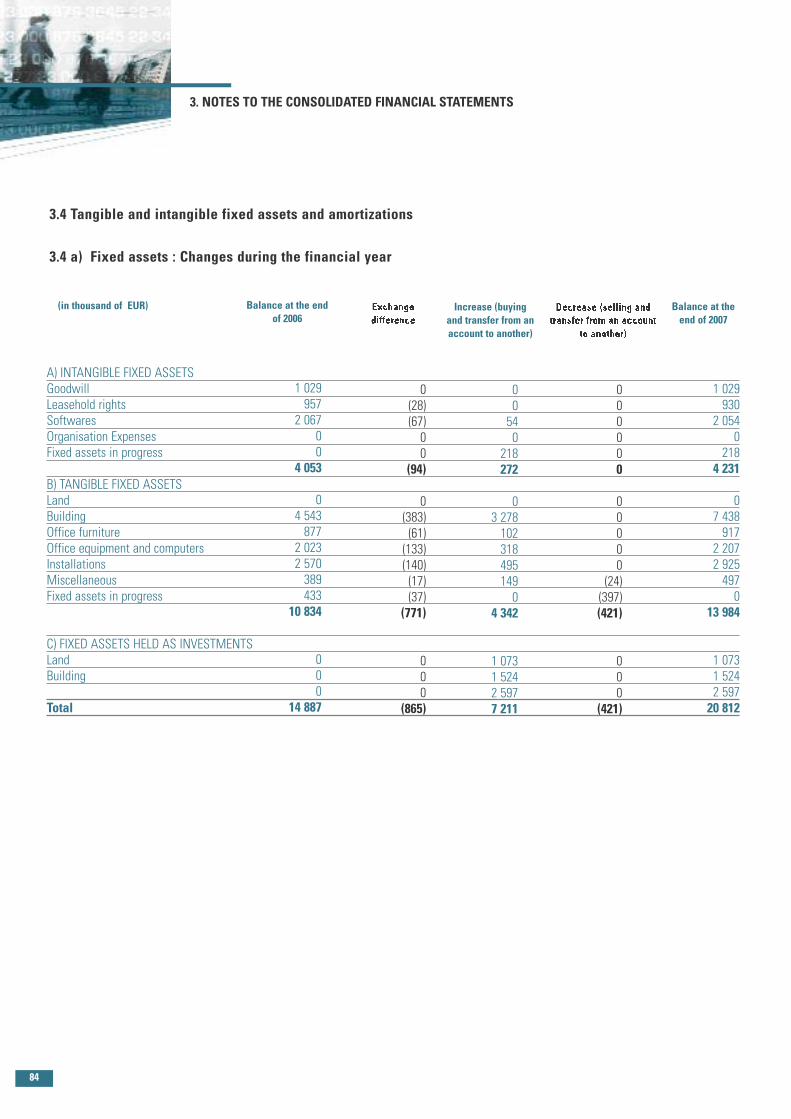

3.4 Immobilisations corporelles, incorporelles et amortissements

3.4 a) Immobilisations : Valeurs brutes - Mouvements de l'exercice

A) IMMOBILISATIONS INCORPORELLESFond commercialDroit au bailLogicielsFrais d'établissementImmobilisations en cours

B) IMMOBILISATIONS CORPORELLESTerrainsConstructionsMobilier de bureauEquipement informatique et de bureauAménagements installationsDiversImmobilisations en cours

C) IMMOBILISATIONS HORS EXPLOITATIONTerrainsConstructions

TOTAL

Augmentations(achats et virementsde poste à poste)

Soldes à fin2007

0(28)(67)00

(94)

0(383)(61)(133)(140)(17)(37)

(771)

000

(865)

00540

218272

03 2781023184951490

4 342

1 0731 5242 5977 211

000000

00000

(24)(397)(421)

000

(421)

1 029930

2 0540

2184 231

07 438917

2 2072 9254970

13 984

1 0731 5242 59720 812

Soldes à fin2006

1 029957

2 06700

4 053

04 543877

2 0232 570389433

10 834

000

14 887

(en milliers de EUR)

38

3.4 b) Amortissements : Mouvements de l'exercice

(a) Ce montant correspond en fait à une provision pour dépréciation et non aux amortissements

A) IMMOBILISATIONS INCORPORELLESFond commercialDroit au bailLogicielsFrais d'établissementImmobilisations en coursB) IMMOBILISATIONS CORPORELLESTerrainsConstructionsMobilier de bureauEquipement informatique et de bureauAménagements installationsDiversImmobilisations en cours

C) IMMOBILISATIONS HORS EXPLOITATIONTerrainsConstructions

TOTAL

Augmentations(achats et virementsde poste à poste)

Soldes à fin2007

0-28-6300

(90)0

(86)(57)(111)(117)(11)0

(382)

000

(472)

003100310

10431176101540

466

01717514

00000000000

(24)0

(24)

000

(24)

1 029(a)9301 971

00

3 9290

1 040761

1 7952 1463360

6 078

01717

10 024

Soldes à fin2006

1 029(a)9572 002

00

3 9890

1 022787

1 7292 1613180

6 017

000

10 006

(en milliers de EUR)

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

39

3. NOTES SUR LE BILAN

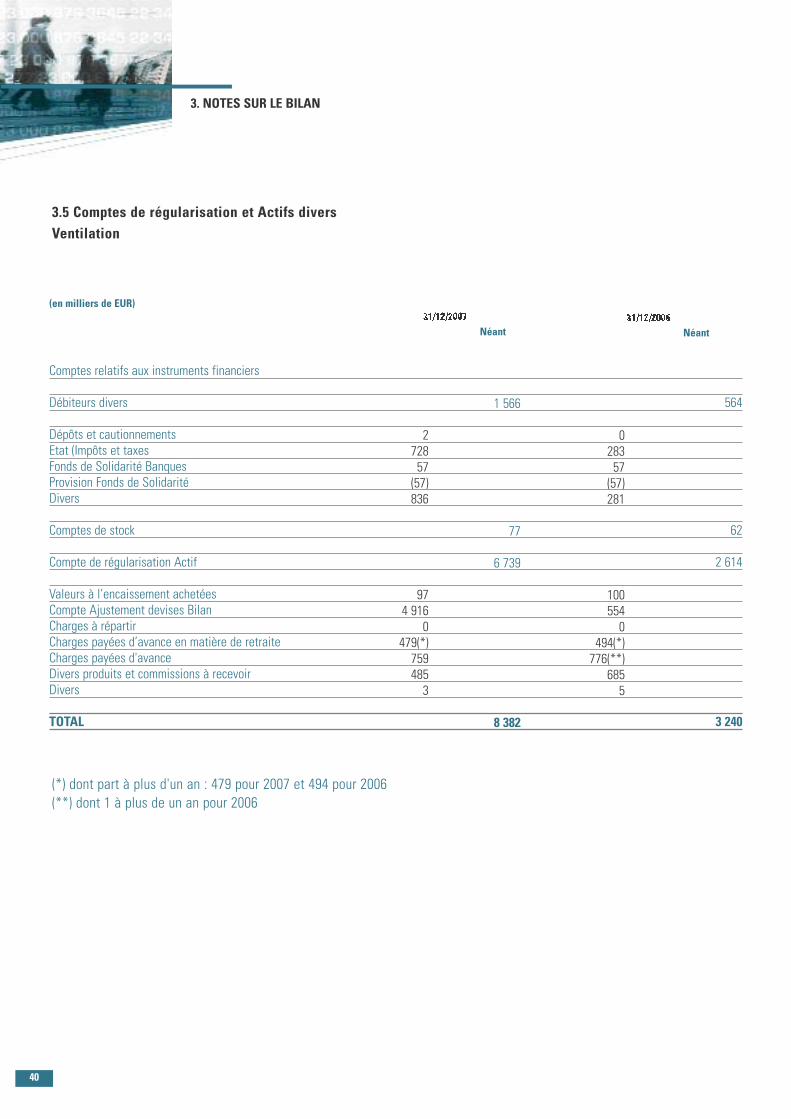

3.5 Comptes de régularisation et Actifs diversVentilation

(*) dont part à plus d'un an : 479 pour 2007 et 494 pour 2006(**) dont 1 à plus de un an pour 2006

Comptes relatifs aux instruments financiers

Débiteurs divers

Dépôts et cautionnementsEtat (Impôts et taxesFonds de Solidarité BanquesProvision Fonds de SolidaritéDivers

Comptes de stock

Compte de régularisation Actif

Valeurs à l’encaissement achetéesCompte Ajustement devises BilanCharges à répartirCharges payées d’avance en matière de retraiteCharges payées d'avanceDivers produits et commissions à recevoirDivers

TOTAL

Néant

272857(57)836

974 916

0479(*)7594853

1 566

77

6 739

8 382

028357(57)281

1005540

494(*)776(**)

6855

564

62

2 614

3 240

(en milliers de EUR)

Néant

40

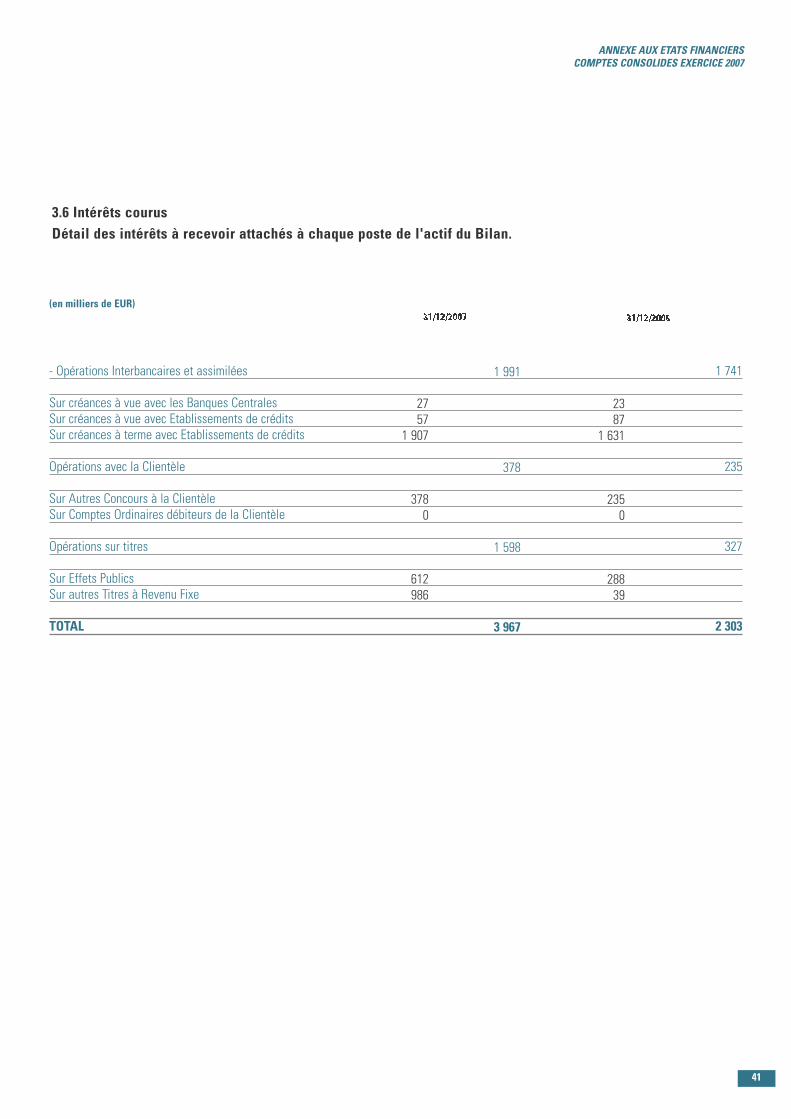

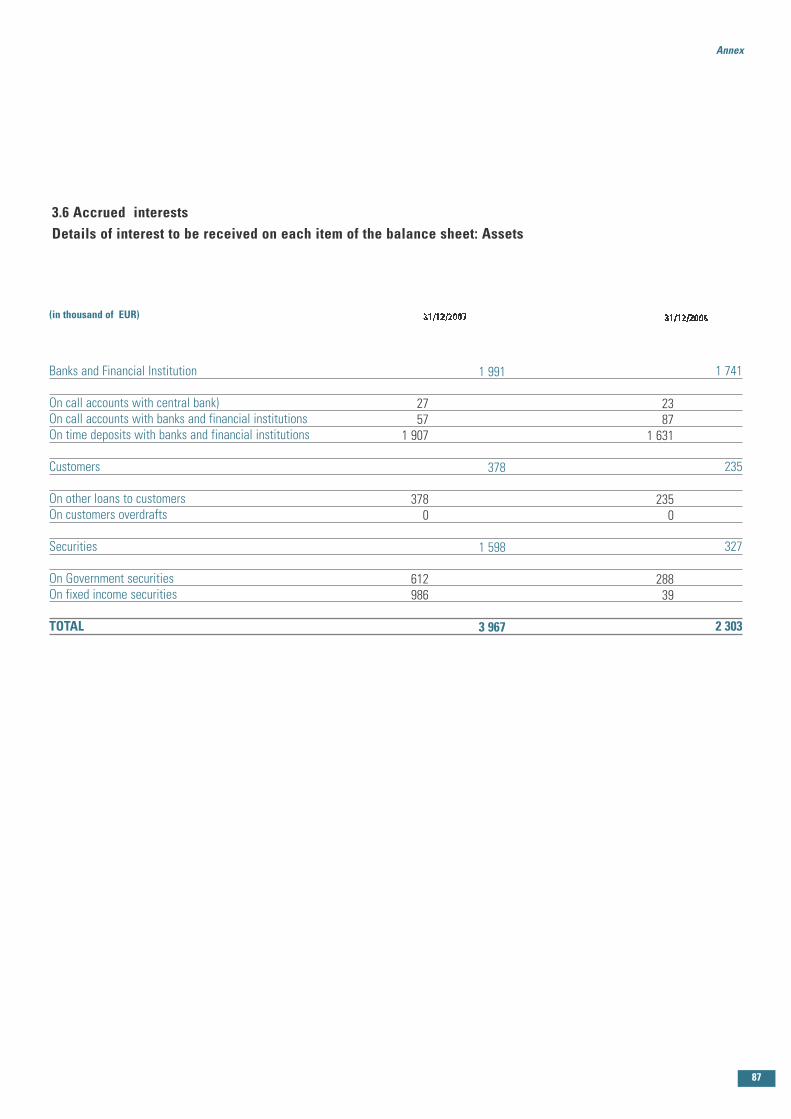

3.6 Intérêts courusDétail des intérêts à recevoir attachés à chaque poste de l'actif du Bilan.

- Opérations Interbancaires et assimilées

Sur créances à vue avec les Banques CentralesSur créances à vue avec Etablissements de créditsSur créances à terme avec Etablissements de crédits

Opérations avec la Clientèle

Sur Autres Concours à la ClientèleSur Comptes Ordinaires débiteurs de la Clientèle

Opérations sur titres

Sur Effets PublicsSur autres Titres à Revenu Fixe

TOTAL

2757

1 907

3780

612986

1 991

378

1 598

3 967

2387

1 631

2350

28839

1 741

235

327

2 303

(en milliers de EUR)

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

41

PASSIF

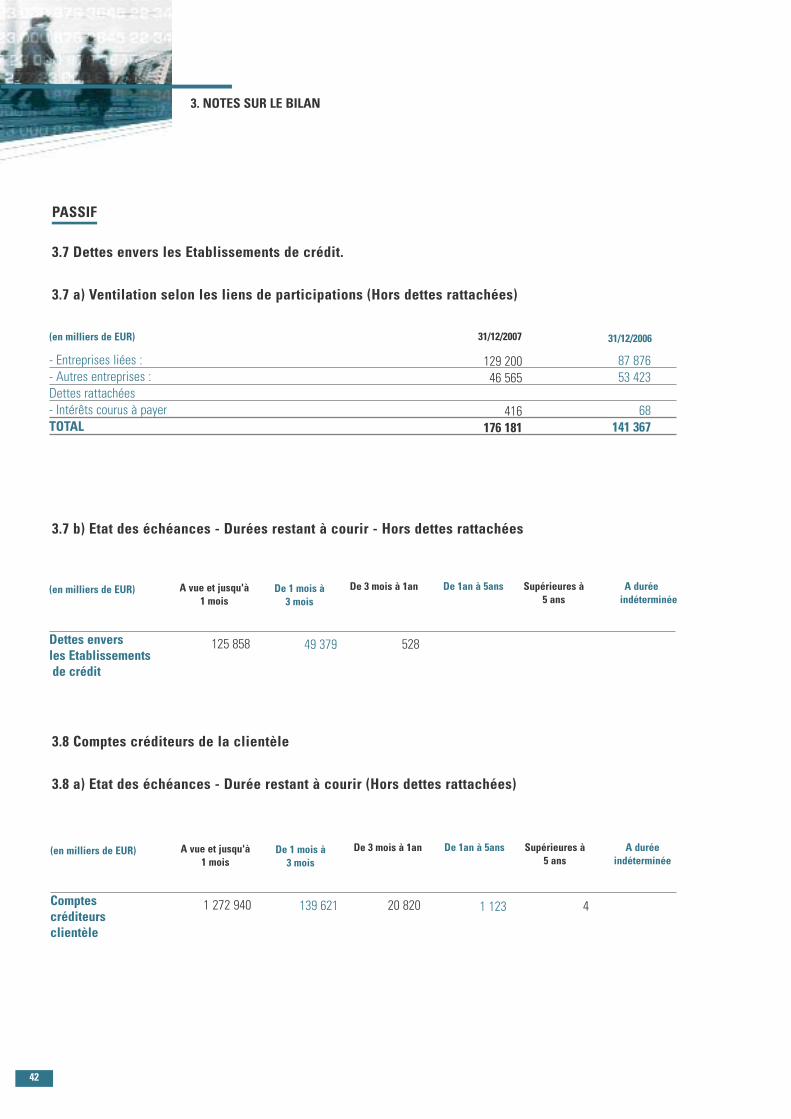

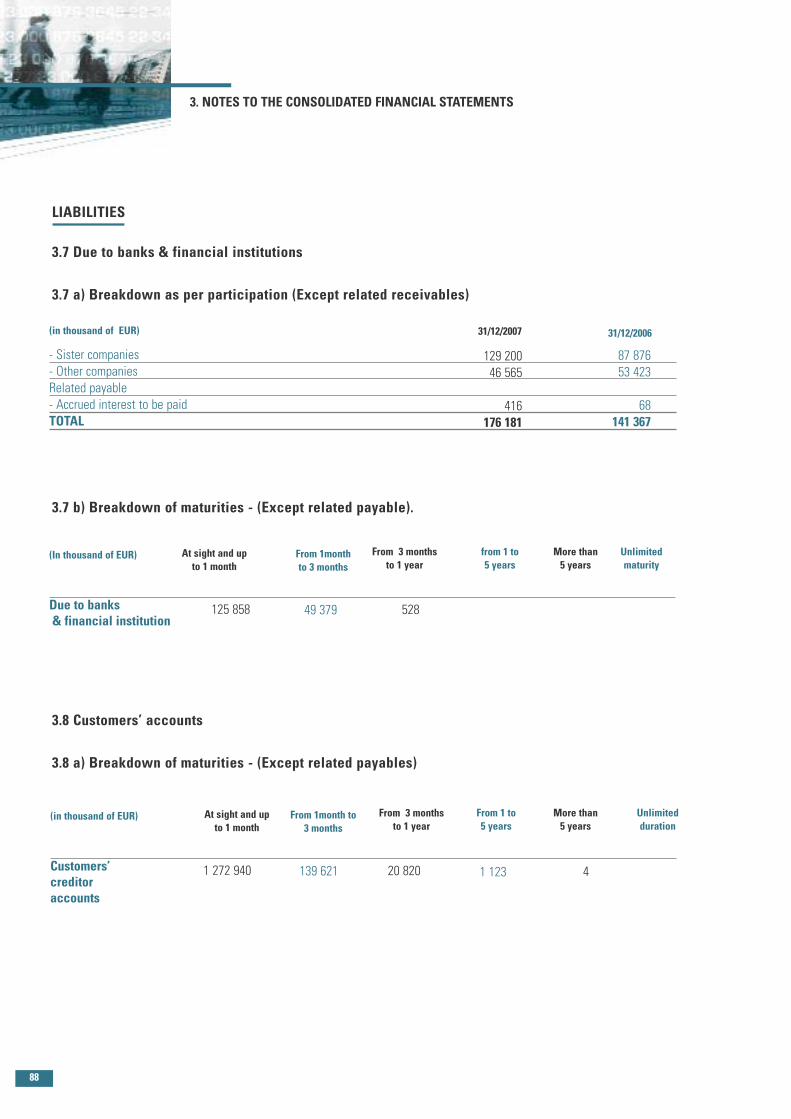

3.7 Dettes envers les Etablissements de crédit.

3.7 a) Ventilation selon les liens de participations (Hors dettes rattachées)

3.7 b) Etat des échéances - Durées restant à courir - Hors dettes rattachées

3.8 Comptes créditeurs de la clientèle

3.8 a) Etat des échéances - Durée restant à courir (Hors dettes rattachées)

3. NOTES SUR LE BILAN

- Entreprises liées :- Autres entreprises :Dettes rattachées- Intérêts courus à payerTOTAL

87 87653 423

68141 367

31/12/200631/12/2007

129 20046 565

416176 181

Dettes enversles Etablissementsde crédit

A vue et jusqu'à1 mois

De 1 mois à3 mois

De 1an à 5ans Supérieures à5 ans

De 3 mois à 1an A duréeindéterminée

(en milliers de EUR)

125 858 49 379 528

Comptescréditeursclientèle

A vue et jusqu'à1 mois

De 1 mois à3 mois

De 1an à 5ans Supérieures à5 ans

De 3 mois à 1an A duréeindéterminée

(en milliers de EUR)

1 272 940 139 621 20 820 1 123 4

(en milliers de EUR)

42

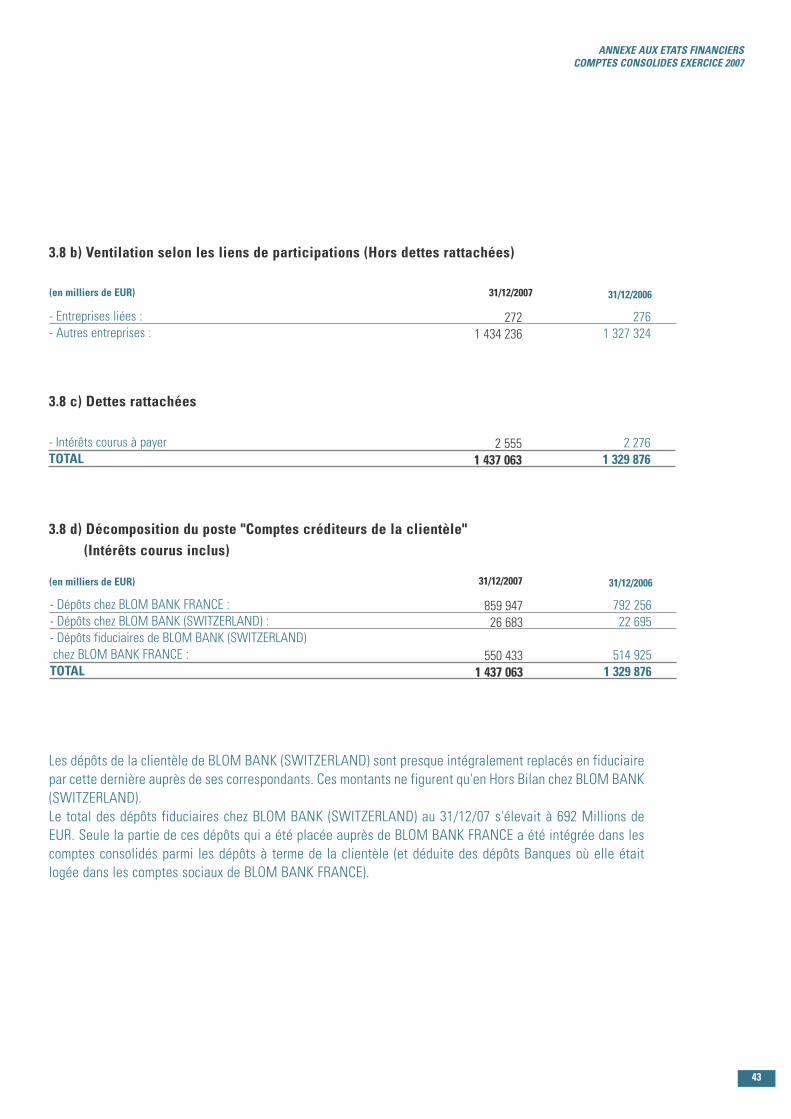

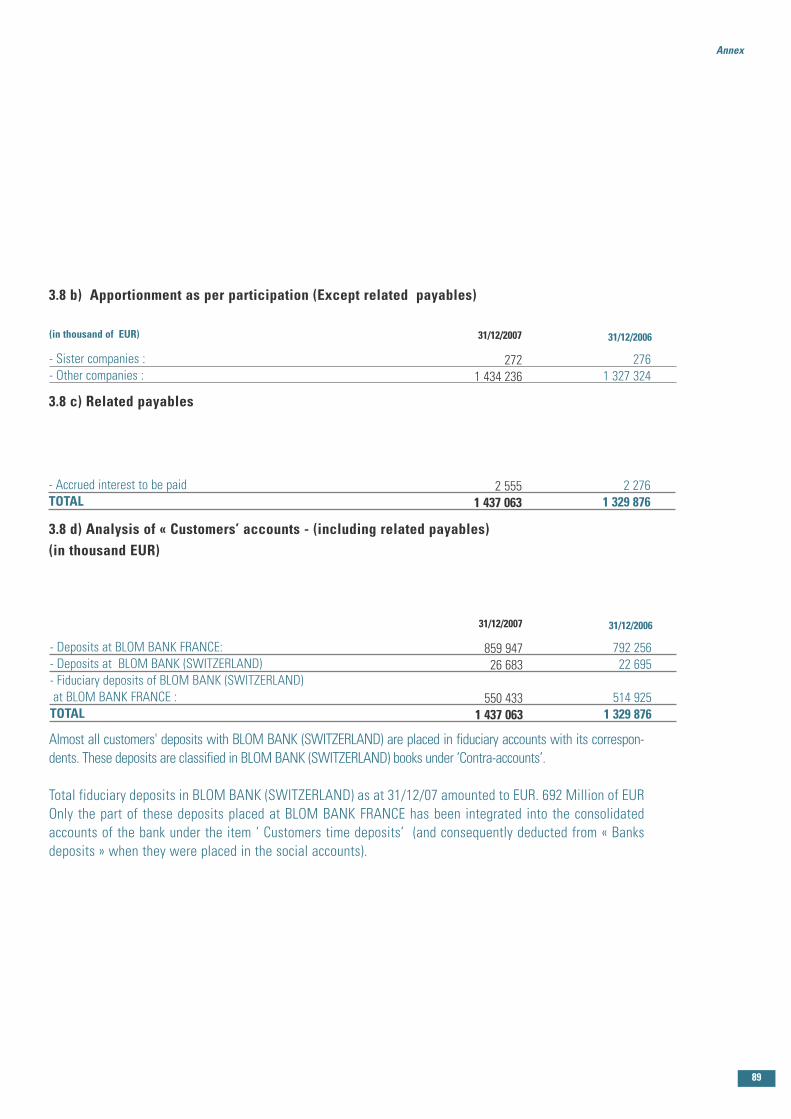

3.8 b) Ventilation selon les liens de participations (Hors dettes rattachées)

3.8 c) Dettes rattachées

3.8 d) Décomposition du poste "Comptes créditeurs de la clientèle"(Intérêts courus inclus)

Les dépôts de la clientèle de BLOM BANK (SWITZERLAND) sont presque intégralement replacés en fiduciairepar cette dernière auprès de ses correspondants. Ces montants ne figurent qu'en Hors Bilan chez BLOM BANK(SWITZERLAND).Le total des dépôts fiduciaires chez BLOM BANK (SWITZERLAND) au 31/12/07 s'élevait à 692 Millions deEUR. Seule la partie de ces dépôts qui a été placée auprès de BLOM BANK FRANCE a été intégrée dans lescomptes consolidés parmi les dépôts à terme de la clientèle (et déduite des dépôts Banques où elle étaitlogée dans les comptes sociaux de BLOM BANK FRANCE).

- Entreprises liées :- Autres entreprises :

2761 327 324

31/12/200631/12/2007

2721 434 236

- Intérêts courus à payerTOTAL

2 2761 329 876

2 5551 437 063

- Dépôts chez BLOM BANK FRANCE :- Dépôts chez BLOM BANK (SWITZERLAND) :- Dépôts fiduciaires de BLOM BANK (SWITZERLAND)chez BLOM BANK FRANCE :TOTAL

792 25622 695

514 9251 329 876

31/12/200631/12/2007

859 94726 683

550 4331 437 063

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

(en milliers de EUR)

(en milliers de EUR)

43

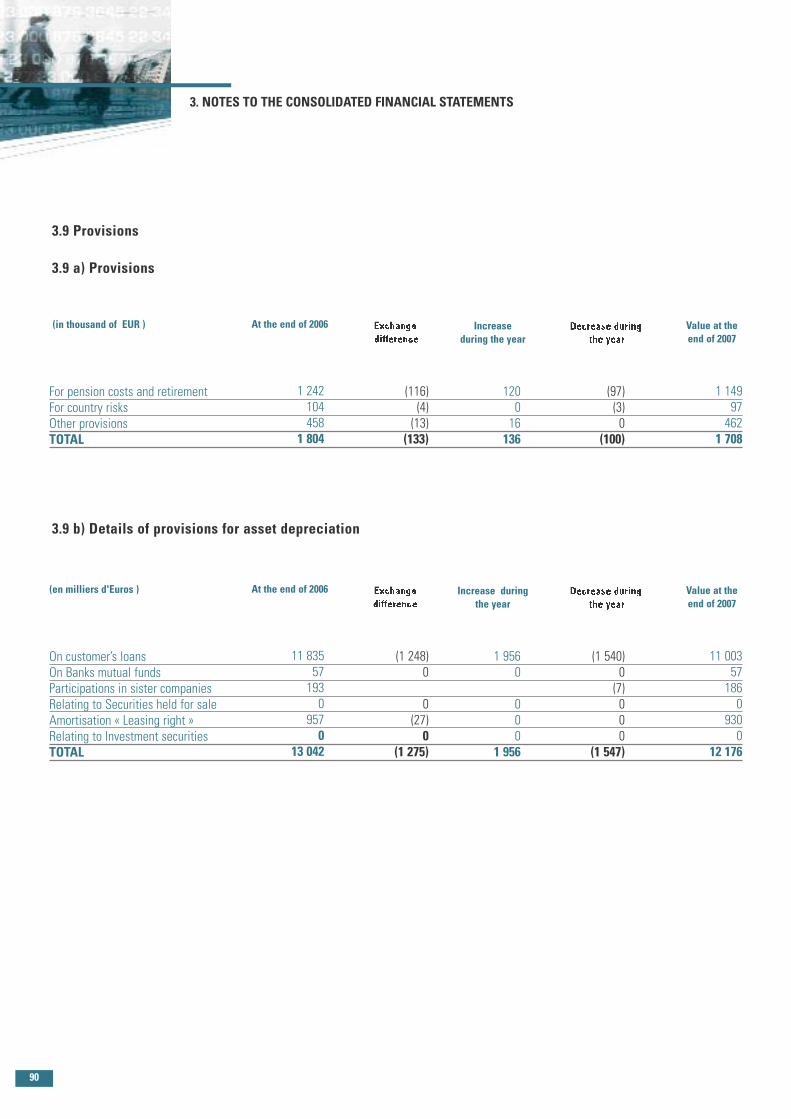

3.9 Provisions

3.9 a) Provisions

3.9 b) Détail des dépréciations des éléments d'actif.

3. NOTES SUR LE BILAN

Pour retraite et départ employésPour risques paysAutres provisionsTOTAL

Augmentation del’exercice

Valeur à fin2007

(116)(4)(13)

(133)

120016136

(97)(3)0

(100)

1 14997462

1 708

Valeur à fin 2006

1 242104458

1 804

(en milliers de EUR)

Sur créances de la clientèleSur débiteur divers “ Solidarité Banques ”Sur parts dans entreprises liéesSur Titres de placementSur Titres d’investissementPour dépréciation « droit au bailTOTAL

Augmentation del’exercice

Valeur à fin2007

(1 248)0

00

(27)(1 275)

1 9560

00

1 956

(1 540)0(7)00

(1 547)

11 0035718600

93012 176

Valeur à fin 2006

11 8355719300

95713 042

(en milliers de EUR)

44

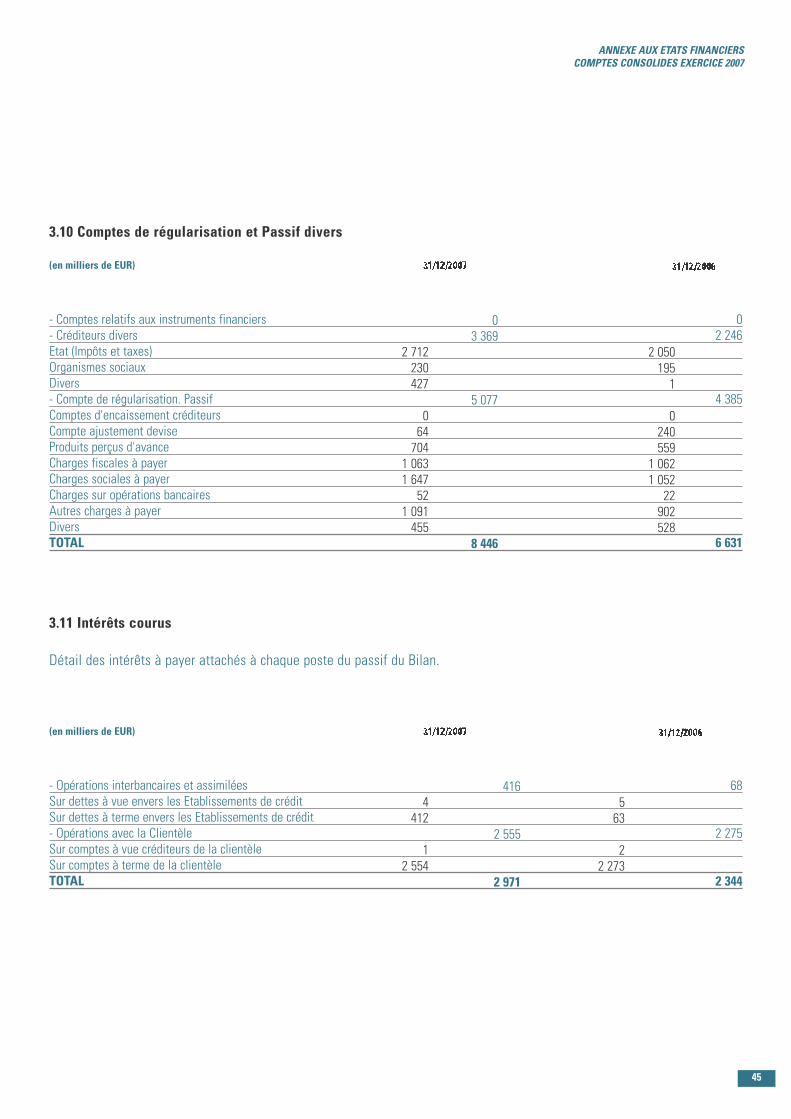

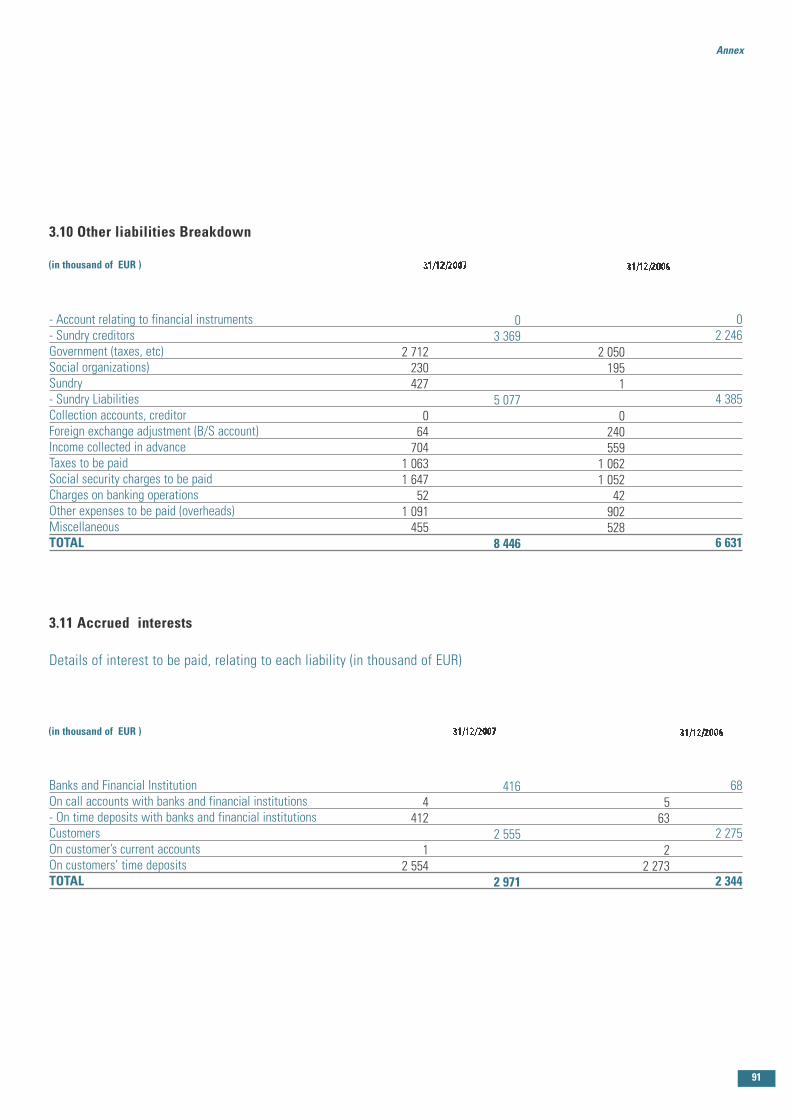

3.10 Comptes de régularisation et Passif divers

3.11 Intérêts courus

Détail des intérêts à payer attachés à chaque poste du passif du Bilan.

- Comptes relatifs aux instruments financiers- Créditeurs diversEtat (Impôts et taxes)Organismes sociauxDivers- Compte de régularisation. PassifComptes d'encaissement créditeursCompte ajustement deviseProduits perçus d'avanceCharges fiscales à payerCharges sociales à payerCharges sur opérations bancairesAutres charges à payerDiversTOTAL

2 712230427

064704

1 0631 647

521 091455

03 369

5 077

8 446

2 0501951

0240559

1 0621 052

22902528

02 246

4 385

6 631

(en milliers de EUR)

- Opérations interbancaires et assimiléesSur dettes à vue envers les Etablissements de créditSur dettes à terme envers les Etablissements de crédit- Opérations avec la ClientèleSur comptes à vue créditeurs de la clientèleSur comptes à terme de la clientèleTOTAL

4412

12 554

416

2 555

2 971

563

22 273

68

2 275

2 344

(en milliers de EUR)

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

45

3. NOTES SUR LE BILAN

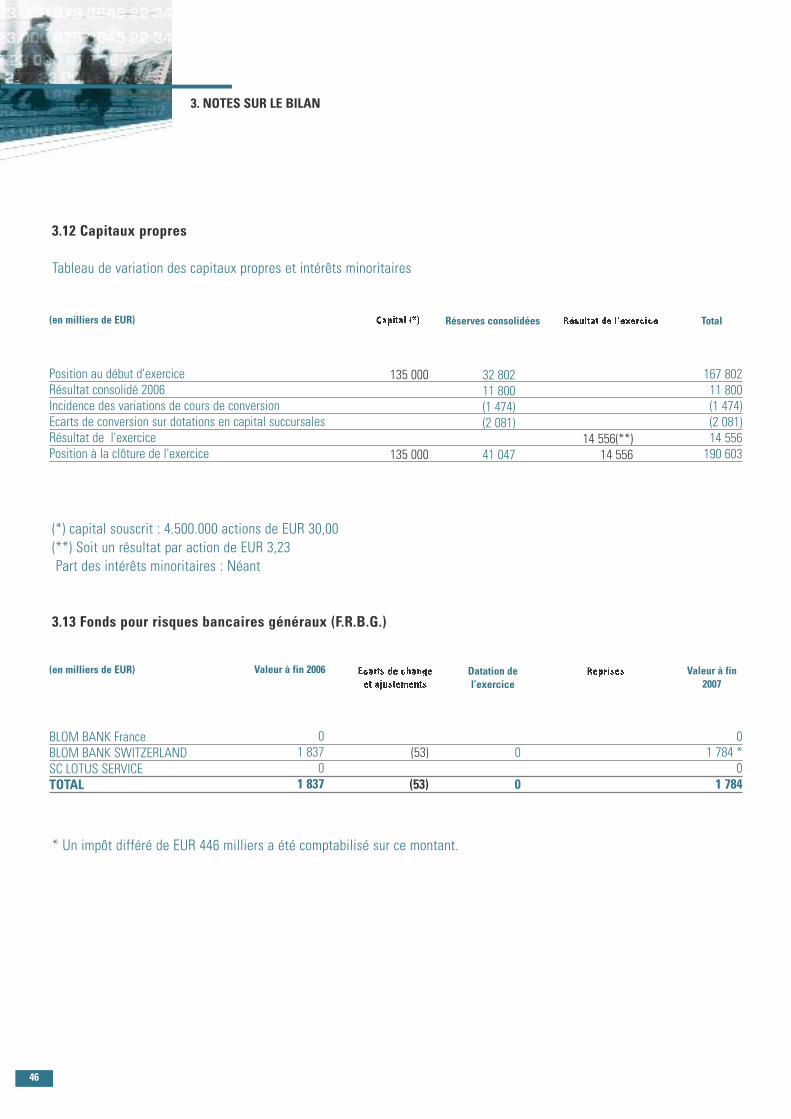

3.12 Capitaux propres

Tableau de variation des capitaux propres et intérêts minoritaires

(*) capital souscrit : 4.500.000 actions de EUR 30,00(**) Soit un résultat par action de EUR 3,23Part des intérêts minoritaires : Néant

3.13 Fonds pour risques bancaires généraux (F.R.B.G.)

* Un impôt différé de EUR 446 milliers a été comptabilisé sur ce montant.

Position au début d'exerciceRésultat consolidé 2006Incidence des variations de cours de conversionEcarts de conversion sur dotations en capital succursalesRésultat de l'exercicePosition à la clôture de l'exercice

135 000

135 000

32 80211 800(1 474)(2 081)

41 04714 556(**)

14 556

167 80211 800(1 474)(2 081)14 556190 603

(en milliers de EUR) Réserves consolidées Total

BLOM BANK FranceBLOM BANK SWITZERLANDSC LOTUS SERVICETOTAL

Datation del’exercice

Valeur à fin2007

(53)

(53)

0

0

01 784 *

01 784

Valeur à fin 2006

01 837

01 837

(en milliers de EUR)

46

HORS BILAN

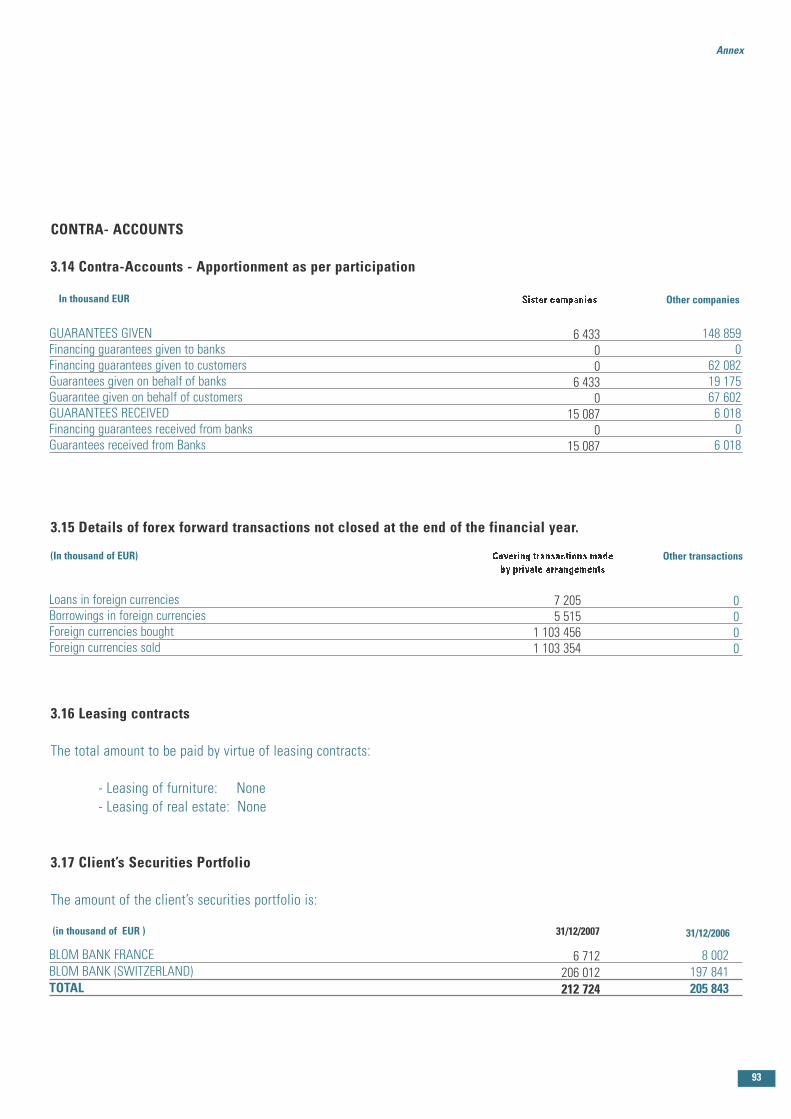

3.14 Hors Bilan - Ventilation selon les liens de participation

3.15 Détail sur les opérations à terme sur devises non dénouées à la clôture de l'exercice.

3.16 Engagements de crédit-bail

Montant total des redevances à payer sur les biens acquis en crédit-bail :

- Crédit-bail mobilier : Néant- Crédit-bail immobilier : Néant

3.17 Portefeuille titres de la clientèle

Le montant du portefeuille titres en dépôts est de :En milliers d’euros

ENGAGEMENTS DONNESEngagements de financement en faveur d'Ets de créditEngagements de financement en faveur de la clientèleEngagements de garantie d'ordre d'Ets de créditEngagements de garantie d'ordre de la clientèleENGAGEMENTS RECUSEngagements de financement reçus d'Ets de créditEngagements de garantie reçus d'Ets de crédit

6 43300

6 4330

15 0870

15 087

148 8590

62 08219 17567 6026 018

06 018

(en milliers de EUR) Autres entreprises

Prêts de devisesEmprunts de devisesDevises achetéesDevises vendues

(en milliers de EUR) Autres opérations

7 2055 515

1 103 4561 103 354

BLOM BANK FRANCEBLOM BANK (SWITZERLAND)TOTAL

8 002197 841205 843

31/12/200631/12/2007

6 712206 012212 724

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

47

3. NOTES SUR LE BILAN

COMPTE DE RESULTAT

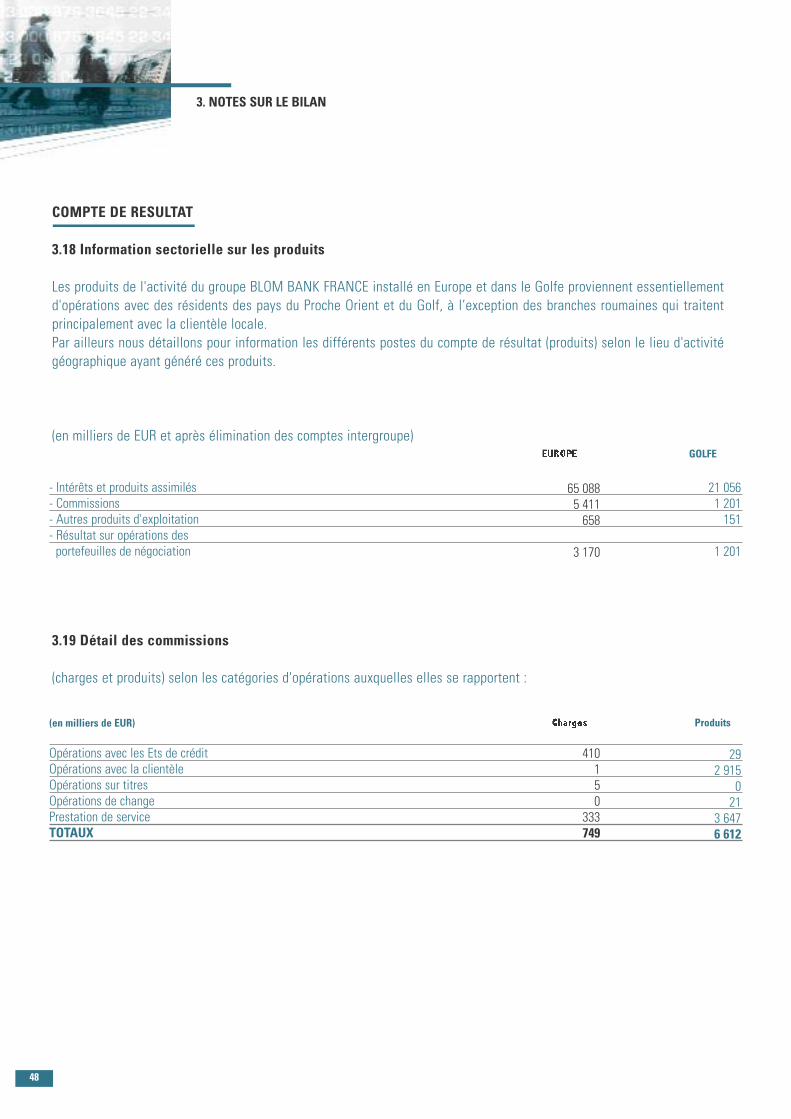

3.18 Information sectorielle sur les produits

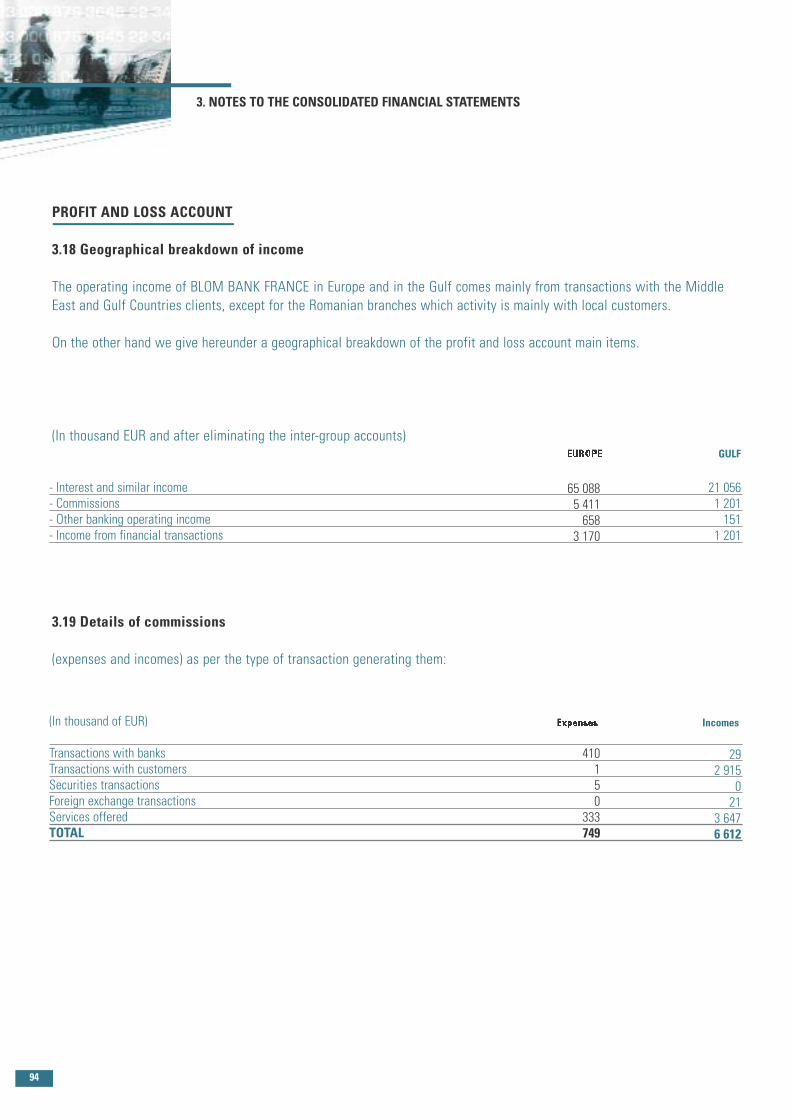

Les produits de l'activité du groupe BLOM BANK FRANCE installé en Europe et dans le Golfe proviennent essentiellementd'opérations avec des résidents des pays du Proche Orient et du Golf, à l’exception des branches roumaines qui traitentprincipalement avec la clientèle locale.Par ailleurs nous détaillons pour information les différents postes du compte de résultat (produits) selon le lieu d'activitégéographique ayant généré ces produits.

(en milliers de EUR et après élimination des comptes intergroupe)

3.19 Détail des commissions

(charges et produits) selon les catégories d'opérations auxquelles elles se rapportent :

- Intérêts et produits assimilés- Commissions- Autres produits d'exploitation- Résultat sur opérations desportefeuilles de négociation

65 0885 411658

3 170

21 0561 201151

1 201

GOLFE

Opérations avec les Ets de créditOpérations avec la clientèleOpérations sur titresOpérations de changePrestation de serviceTOTAUX

410150

333749

292 915

021

3 6476 612

Produits(en milliers de EUR)

48

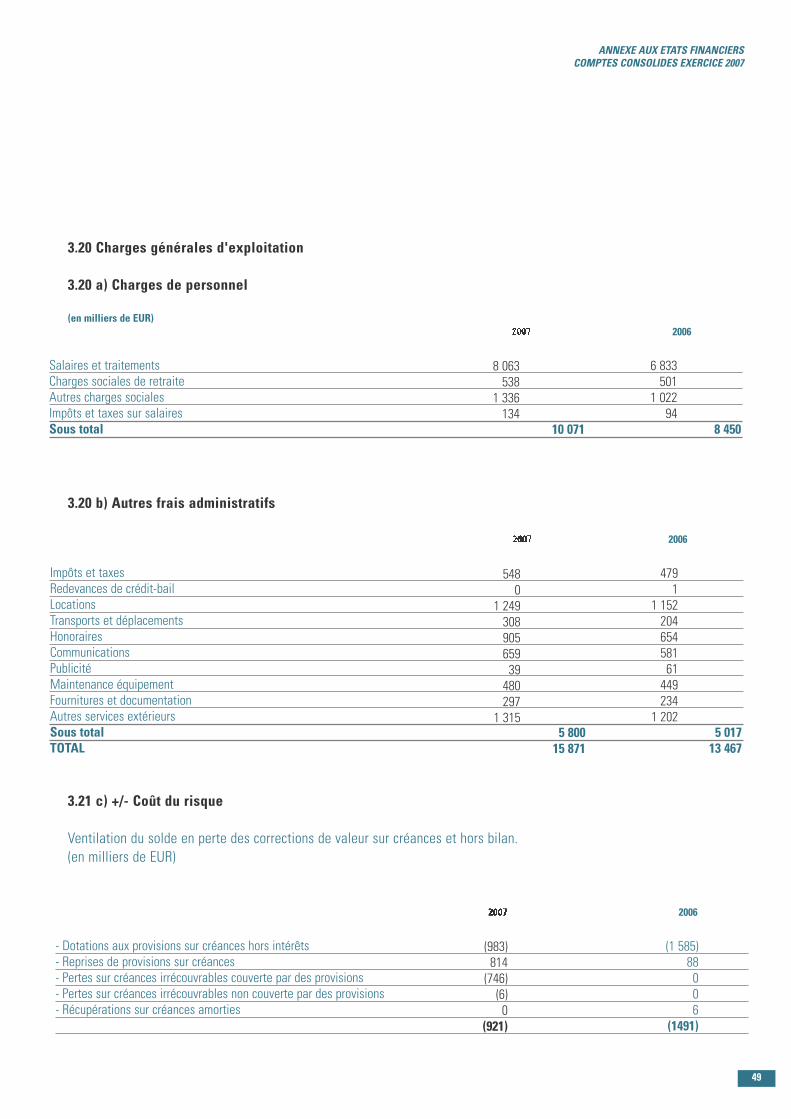

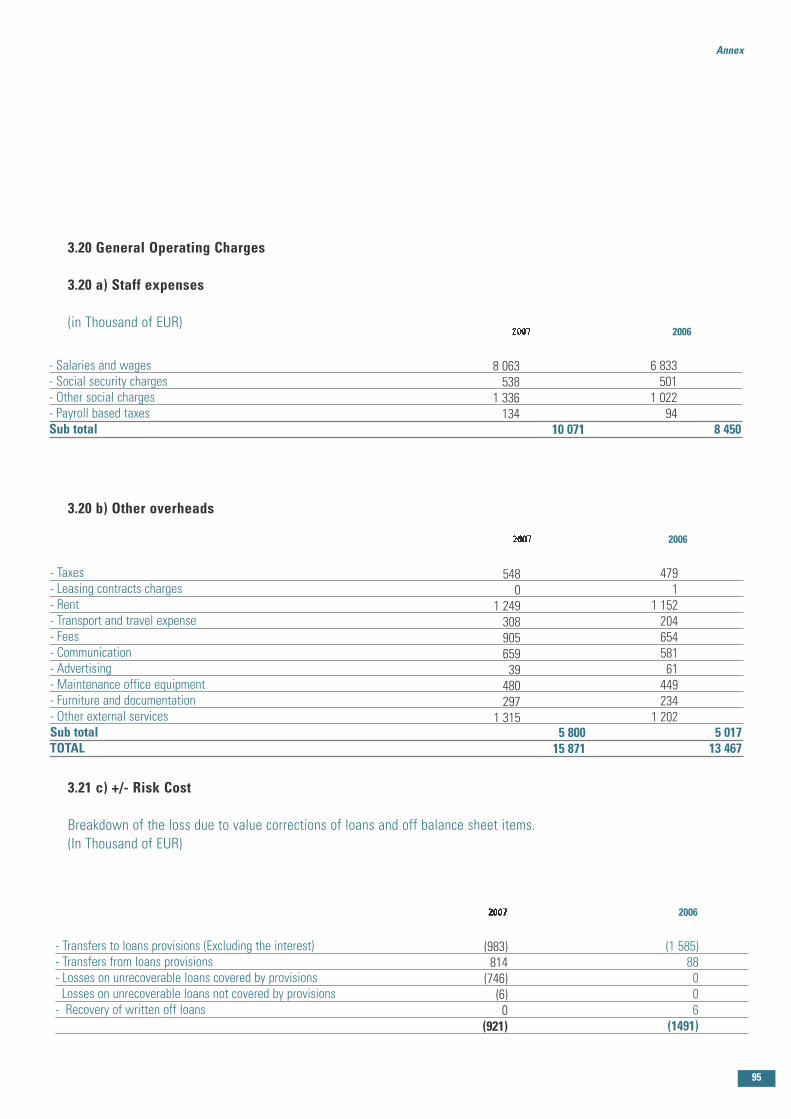

3.20 Charges générales d'exploitation

3.20 a) Charges de personnel

(en milliers de EUR)

3.20 b) Autres frais administratifs

3.21 c) +/- Coût du risque

Ventilation du solde en perte des corrections de valeur sur créances et hors bilan.(en milliers de EUR)

Salaires et traitementsCharges sociales de retraiteAutres charges socialesImpôts et taxes sur salairesSous total

8 063538

1 336134

8 450

2006

10 071

6 833501

1 02294

Impôts et taxesRedevances de crédit-bailLocationsTransports et déplacementsHonorairesCommunicationsPublicitéMaintenance équipementFournitures et documentationAutres services extérieursSous totalTOTAL

5480

1 24930890565939480297

1 3155 01713 467

5 80015 871

4791

1 15220465458161449234

1 202

- Dotations aux provisions sur créances hors intérêts- Reprises de provisions sur créances- Pertes sur créances irrécouvrables couverte par des provisions- Pertes sur créances irrécouvrables non couverte par des provisions- Récupérations sur créances amorties

(983)814(746)(6)0

(921)

2006

(1 585)88006

(1491)

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

2006

49

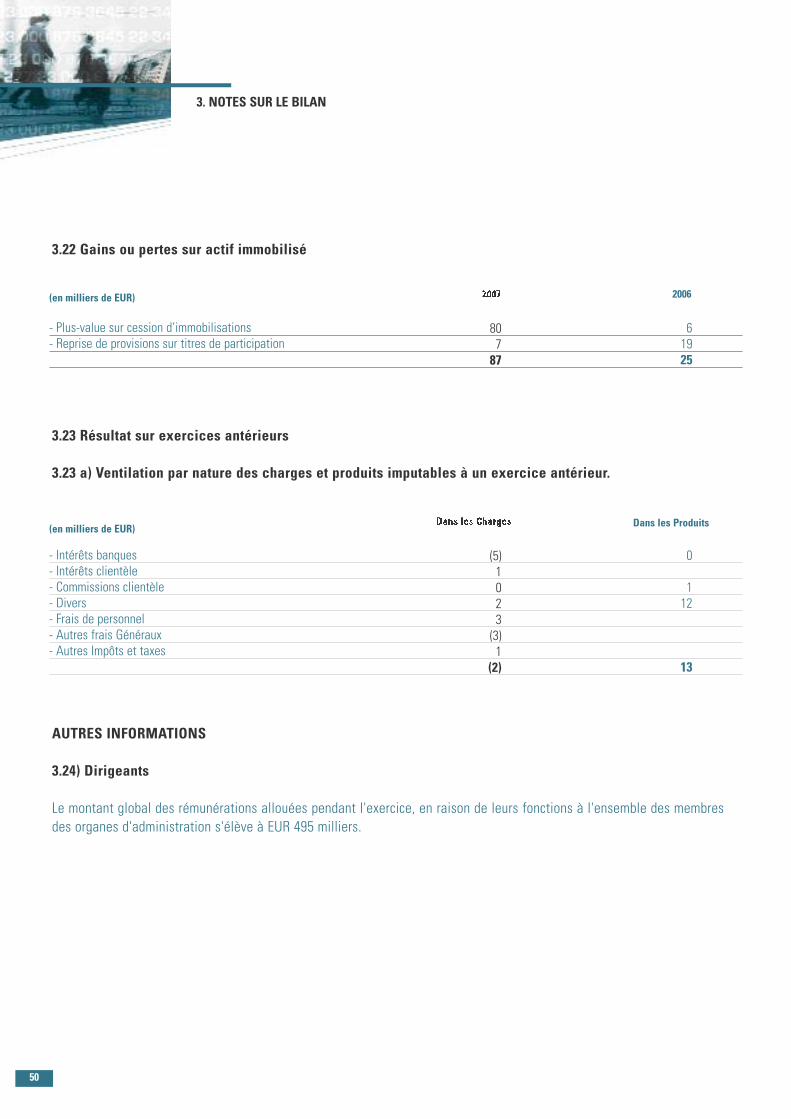

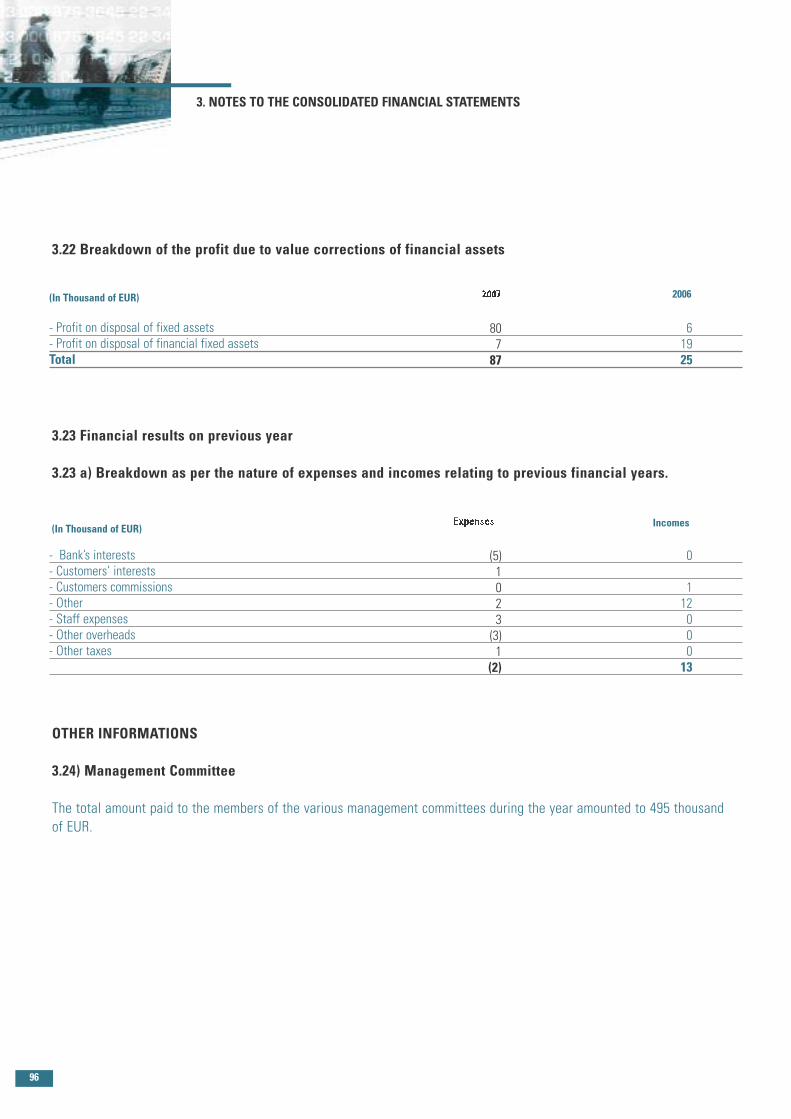

3.22 Gains ou pertes sur actif immobilisé

3.23 Résultat sur exercices antérieurs

3.23 a) Ventilation par nature des charges et produits imputables à un exercice antérieur.

AUTRES INFORMATIONS

3.24) Dirigeants

Le montant global des rémunérations allouées pendant l'exercice, en raison de leurs fonctions à l'ensemble des membresdes organes d'administration s'élève à EUR 495 milliers.

3. NOTES SUR LE BILAN

- Plus-value sur cession d’immobilisations- Reprise de provisions sur titres de participation

80787

2006

61925

(en milliers de EUR)

(en milliers de EUR)

- Intérêts banques- Intérêts clientèle- Commissions clientèle- Divers- Frais de personnel- Autres frais Généraux- Autres Impôts et taxes

(5)1023(3)1

(2)

Dans les Produits

0

112

13

50

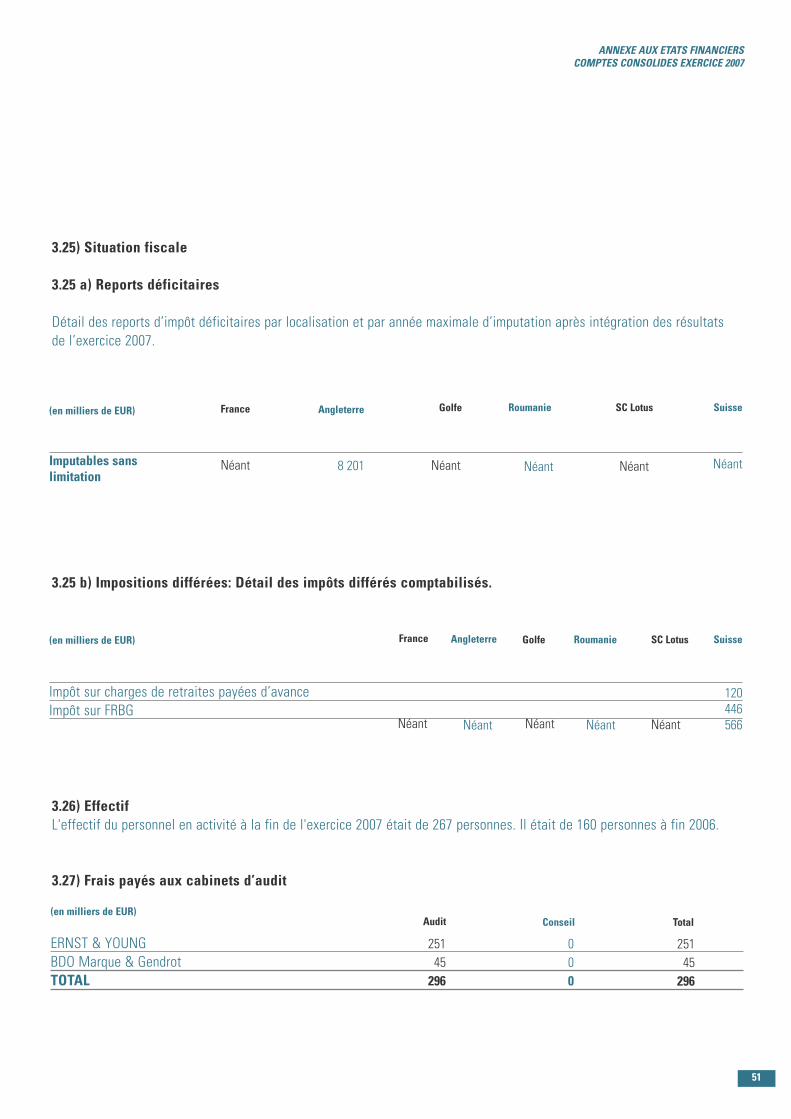

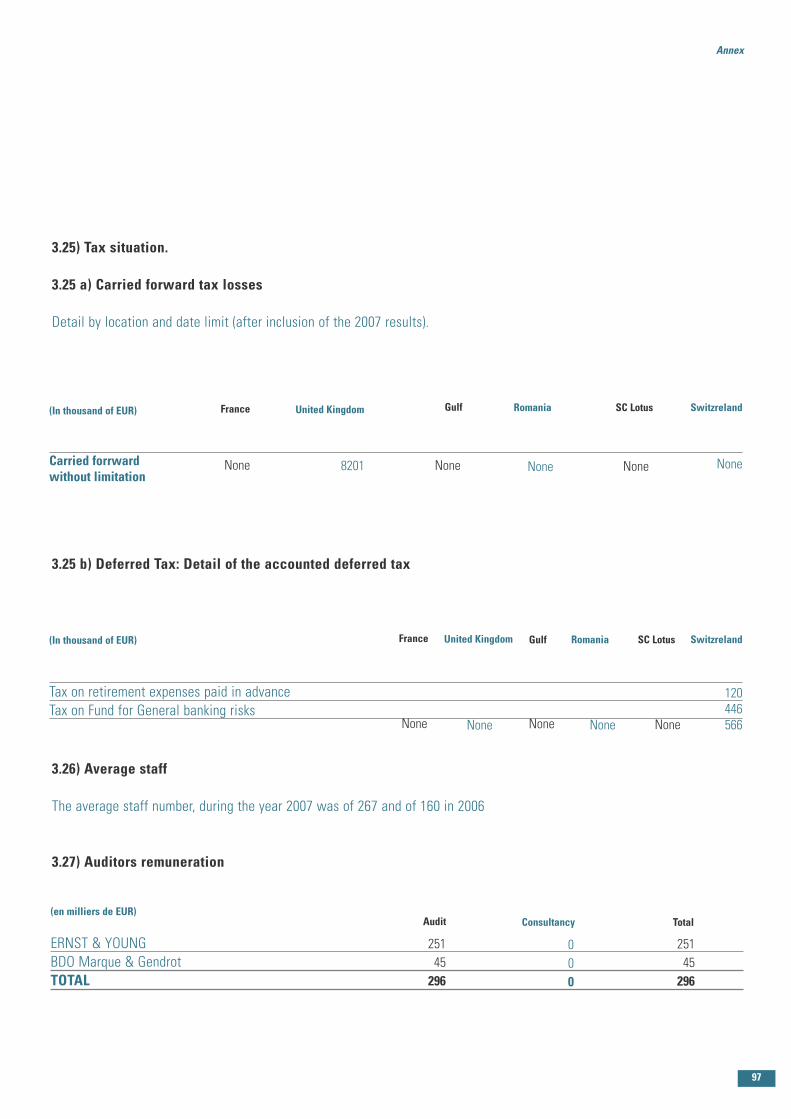

3.25) Situation fiscale

3.25 a) Reports déficitaires

Détail des reports d’impôt déficitaires par localisation et par année maximale d’imputation après intégration des résultatsde l’exercice 2007.

3.25 b) Impositions différées: Détail des impôts différés comptabilisés.

3.26) EffectifL'effectif du personnel en activité à la fin de l'exercice 2007 était de 267 personnes. Il était de 160 personnes à fin 2006.

3.27) Frais payés aux cabinets d’audit

Imputables sanslimitation

France Angleterre Roumanie SC LotusGolfe Suisse(en milliers de EUR)

Néant 8 201 Néant Néant Néant Néant

Impôt sur charges de retraites payées d’avanceImpôt sur FRBG

France Angleterre Roumanie SC LotusGolfe(en milliers de EUR)

Néant Néant Néant Néant

Suisse

120446566Néant

ERNST & YOUNGBDO Marque & GendrotTOTAL

(en milliers de EUR)Audit Conseil Total

25145296

000

25145296

ANNEXE AUX ETATS FINANCIERSCOMPTES CONSOLIDES EXERCICE 2007

51

54

At BLOM BANK Group, our mission has always been toensure the peace of mind of our customers by providing

them with comprehensive banking services and ensuringtheir satisfaction.

With that in mind, we have always placed great importance inexpanding our international network in order to spread that “ peace

of mind” as far as possible so that our customers can globally rely onour banking services

Rapport Annuel 07/ Annual Report 07

55

PRINCIPAL FEATURES OF THE FINANCIAL YEAR 2007

Similar to previous years, 2007 was characterized by an unstable environment in the MiddleEast, reinforcing BLOM Bank group’s strategy to focus on the activity of its affiliated bank inFrance. Within this context, BLOM Bank France has once again proven the sustainability of itsperformance with continuous increase in profits as well as efficient financial ratios, confirmingthe Bank’s prudent strategy characterizing its management.

This financial year has been characterized mainly by the consolidation (as of 30 November2007) of the Romanian branches with our accounts, previously affiliated with BLOM BankEgypt.

The performance of the year 2007 has also been marked by the implementation of a neworganizational structure, which focuses mainly on:- separation between the structure of the headquarters - reinforced by the functionaldepartmentation- and the Paris branch- implementation of integrated channels within branches, and reporting to various managementunits at headquarters in the fields of risk management, information technology, humanresources, finance and accounting as well as internal audit.- implementation of new budgetary measures- integration of Board members in the Audit Committee and the adoption of an audit charter

On exclusively financial basis, and despite the continuous depreciation of the USD/Euro (lessthan 12% for 2007 and less than 25% in two years), the financials of BLOM Bank France haveprogressed (+11% for the individual branches and +9% for the consolidated accounts). Profitsincreased to EUR 9,844,492 for individual branches and EUR 14,555,865 for the consolidatedaccounts (thus +27% and +23% respectively compared to 2006).

Despite the deteriorating situation in Lebanon, the parent company, BLOM BANK SAL, whichholds 99% of the shares, presented for the year 2007 improving financial results. All thesubsidiaries of the Group have grown and the consolidated figures reflect strong growthlevels.

BLOM BANK SAL has been rated by Moody’s ‘”Aa1,lb” the highest local financial strength rating.

Similar to the BLOM BANK FRANCE group, the other companies affiliated to BLOM BANK SAL,whether in Syria with Bank of Syria and Overseas or in Egypt with BLOM Bank Egypt, havemaintained their growth.

The main characteristics of the parent company, BLOM BANK SAL, on a consolidated basis forthe financial year 2007 are the following:- 17% increase in the total assets to USD 16.6B- 17% increase in deposits to USD13.7B- Net profits of USD 204.9M (increasing 13.8%)- Capital adequacy ratio more than double of the required ratio in Lebanon.- Capitalization (Tier I and Tier II capital) to USD1.4B

PRINCIPAL FEATURES OF THE FINANCIAL YEAR 2007

56

The total assets of BLOM Bank France amounted at EUR1,816M at the end of 2007, increasing by9.3% compared to the end of 2006.

Loans to customers stood at EUR307M at the end of 2007, compared to EUR249M at the end of 2006(increasing by 23,55% due to the consolidation of the Romanian branches).

Fixed assets stood at 10.79M at the end of 2007, increasing by 121% mainly due to the accountingfor the properties of the Romanian branches.

Customers deposits increased by 8% compared to last year to EUR1,437M at the end of 2007 (20.8%for the figures in USD) with the share of Romanian branches’ deposits amounting to EUR 41M.

Customers’ engagements represented only 21% of total customers deposits and only 19% of totaldeposits, reflecting the excellent level of global liquidity and confirming the prudent strategy alreadymentioned.

Net banking income stood at EUR 36,42M in 2007 (EUR 35.71M excluding Romania) compared to EUR31.09M in 2006.

General operating expenses (general expenses, staff expenses, taxes, etc…) have increased17.85% to EUR15.87M in 2007 compared to EUR13.47M in 2006. Apart from the integration costsof the Romanian branches at 10%, this increase is mainly driven by the rise in staff expenses dueto the recruitment of new employees during the year, mainly for the Paris and UAE branches, inaddition to the salary adjustment in the UAE caused by the high inflation in this region.

Allocations to the depreciation of fixed assets remained stable and amount to EUR0.50M in 2007(0.53M in 2006)

Allocations to provisions for doubtful loans stood at EUR0.92M (1.49M in 2006)

Operating income (before income tax, provisions and provisions write-back, but after depreciation)accounted to EUR20.04M (compared to 17.09M in 2006), thus increasing by 17.26%.

Consolidated income of the year stood at EUR 14,555,864.69 compared to EUR 11,799,888.61 in 2006

The political environment in the Middle East coupled with the economic turmoil of the markets willhave no discernable effect on BLOM Bank France’s prudent strategy of development and growth. Ourcompany expects to reap the fruits of its recent development (internal and external) and remainsoptimistic with respect to its future development.

The organizational structure adopted this year by BLOM Bank should be pursued and our companylooks forward to any opportunity for development taking into consideration the risk aspects of anynew venture.

57

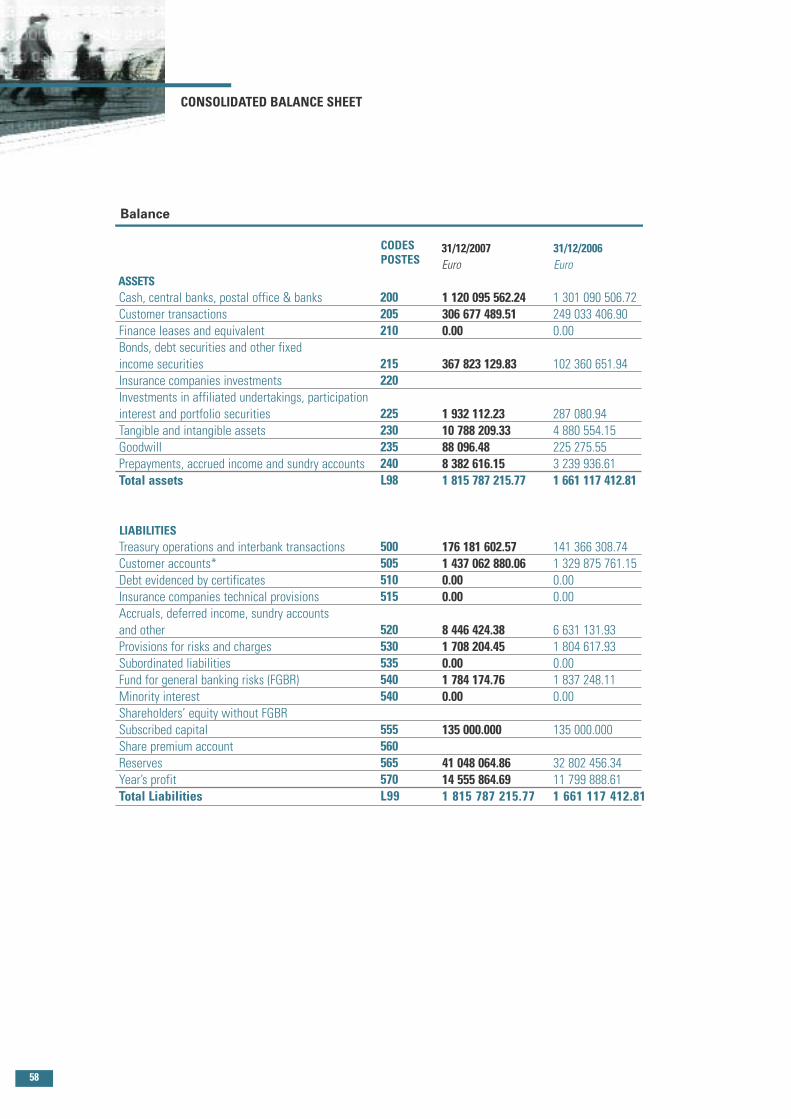

CONSOLIDATED BALANCE SHEET

ASSETSCash, central banks, postal office & banksCustomer transactionsFinance leases and equivalentBonds, debt securities and other fixedincome securitiesInsurance companies investmentsInvestments in affiliated undertakings, participationinterest and portfolio securitiesTangible and intangible assetsGoodwillPrepayments, accrued income and sundry accountsTotal assets

LIABILITIESTreasury operations and interbank transactionsCustomer accounts*Debt evidenced by certificatesInsurance companies technical provisionsAccruals, deferred income, sundry accountsand otherProvisions for risks and chargesSubordinated liabilitiesFund for general banking risks (FGBR)Minority interestShareholders’ equity without FGBRSubscribed capitalShare premium accountReservesYear’s profitTotal Liabilities

Balance

1 120 095 562.24306 677 489.510.00

367 823 129.83

1 932 112.2310 788 209.3388 096.488 382 616.151 815 787 215.77

176 181 602.571 437 062 880.060.000.00

8 446 424.381 708 204.450.001 784 174.760.00

135 000.000

41 048 064.8614 555 864.691 815 787 215.77

1 301 090 506.72249 033 406.900.00

102 360 651.94

287 080.944 880 554.15225 275.553 239 936.611 661 117 412.81

141 366 308.741 329 875 761.150.000.00

6 631 131.931 804 617.930.001 837 248.110.00

135 000.000

32 802 456.3411 799 888.611 661 117 412.81

31/12/2007Euro

31/12/2006Euro

200205210

215220

225230235240L98

500505510515

520530535540540

555560565570L99

CODESPOSTES

58

COMMITMENTS GIVEN

- Financing commitments- Guarantees- Commitments given on securities- Commitments given on insurance activity

COMMITMENTS RECEIVED

- Guarantees- Commitments given on securities- Commitments received on insurance activity

CONTINGENT LIABILITIES

62 082 167,6893 209 692,060.00

21 104 686,410.00

50 204 186,9573 027 483,830,00

13 110 769,740.00

31/12/2007Euro

31/12/2006Euro

810820830840

870880890

CODESPOSTES

(*) Clients deposits : We must take into consideration, in addition to the above amount, the other client funds not included inBLOM BANK (SWITZERLAND) balance sheet (Fiduciary deposits placed outside the group and the client's securities portfolio)nor in BLOM BANK FRANCE balance sheet (client's securities portfolio) these funds amounts to EUR 355 Millions, which bringthe total client deposit to EUR 1 792 "USD 2 637" (compared to EUR 1 733 Millions at the end of 2006)

59

CONSOLIDATED PROFIT AND LOSS ACCOUNT

Interest and similar incomeInterest and similar chargesIncome from variable-yield securitiesCommission (income)Commission (expenses)+/- Profit or loss on negotiableportfolio transactions+/- Portfolio or loss on portfolioheld for sale and equivalentOther banking operation incomeOther banking operation charges+/- Margin on insurance activities+/- Net of the other activitiesNet banking earning :- General operating charges- Depreciation expenses andprovisions for intangible andtangible fixed assets

Gross trading result :+/- Risk cost

Trading result :+/- Share in the net result of the companiesput in equivalence+/- Profit or loss on fixed assets

Ordinary pre-tax profit or loss :+/- Exceptional profit or lossIncome taxAllocation for amortizationof goodwill+/- Allocation for funds for generalbanking risks+/- Minority share

Profit or loss for the financial year group share:- Profit or loss by share- Profit or loss diluted by share

CONSOLIDATED PROFIT AND LOSS ACCOUNT

86 143 648.98(60 592 139.68)163 909.396 612 304.11(749 525.84)

4 371 489.08

0.00809 104.73(342 930.33)

0.0036 415 860.44(15 871 345.37)

(499 835.94)20 044 679.13(920 668.45)19 124 010.68

87 160.0219 211 170.700.00(4 518 126.94)

(137 179.07)

0.00

14 555 864.693.233.23

66 212 620.00(46 543 309.94)1.005 592 838.44(743 811.19)

5 934 597.20

189 466.06774 336.32(326 699.41)

0.0031 090 038.48(13 467 508.21)

(528 405.52)17 094 124.75(1 491 351.58)15 602 773.17

24 968.5715 627 741.740.00(3 690 674.06)

(137 179.07)

0.00

11 799 888.615.245.24

31/12/2007Euro

31/12/2006Euro

500505530540545

550

555560565570580600605

610

620625630

635640650655660

670

675680690

CODESPOSTES

60

STATUTORY AUDITORS’ REPORT ON THE CONSOLIDATED FINANCIAL STATEMENTS

62

63

64

Table of Contentof Year 2007 Annex

1. PRINCIPLES OF CONSOLIDATION1.1 General1.2 Consolidation method1.3 Goodwill

2. ACCOUNTING RULES AND EVALUATION METHODS2.1 General2.2 Accrual basis of accounting2.3 Foreign currency translation2.4 Foreign currency transactions2.5 Local rules2.6 Unpaid loans, doubtful debts and provisions2.7 Securities Portfolio2.8 Fixed Assets2.9 Deferred taxation2.10 Staff benefits2.11 Provisions for general banking risks

3. NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS3.1 Cash, Central Banks, Postal Office & Banks3.2 Customers’ accounts3.3 Securities portfolio3.4 Tangible and intangible fixed assets and amortisations3.5 Prepayments, Accrued Income and Sundry Accounts3.6 Accrued interests3.7 Due to banks & financial institutions3.8 Customers’ accounts3.9 Provisions3.10 Other liabilities3.11 Accrued interests3.12 Shareholders’ Equity3.13 Fund for general banking risks3.14 Contra-Accounts - Apportionment as per participation3.15 Details of forex forward transactions not closed at the end of the financial year3.16 Leasing contracts3.17 Client’s Securities Portfolio3.18 Geographical breakdown of income3.19 Détail des commissions3.20 General Operating Charges3.21 + / - Risk Cost3.22 Breakdown of the profit due to value corrections of financial assets3.23 Financial results on previous year3.24 Management Committee3.25 Tax situation3.26 Average stafff3.27 Auditors remuneration

65

Annex

1. PRINCIPLES OF CONSOLIDATION

1. PRINCIPLES OF CONSOLIDATION

1.1 General

The consolidated financial statement presented hereunder includes the accounts of:

- BLOM BANK SWITZERLAND- “SC LOTUS SERVICES AND TRADING SRL” (Romania)

Both companies are under exclusive control and have been consolidated using the fullconsolidation method as their activities are an extension of banking, financing orrelated activities as fixed by the article L.311-2 of the monetary and financial code, evenwhen, like in the case of the service company “LOTUS SERVICES”, the individualaccounts are structured differently than those of the other companies included in theconsolidation, because they belong to different sectors such as insurance, real estate orcomputer science and service.

The financial statements of these two companies have been prepared accordingly to thelocal accounting regulations, including the adjustments and reclassifications necessaryto comply with the standards of the modified Regulation 91-01 of the « BanksRegulation Committee », and with the regulation 99-07 of the « Accounting RegulationCommittee », as well as with the rules generally adopted by the French and internationalbanking industry.

The investments of BLOM BANK FRANCE in companies the activity of which cannot beconsidered as an extension of the Bank’s activity are not consolidated if they do notmatch with the consolidated criteria specified by the CRC 99-07.

BLOM BANK FRANCE Group accounts are consolidated in the accounts of its parentcompany BLOM BANK S.A.L. (Lebanon) using the full consolidation method.

1.1 Consolidation method

The global consolidation method has been adopted to prepare the consolidated financialstatements, as BLOM BANK FRANCE holds more than 50 % of BLOM BANK (SWITZERLAND)capital and SC LOTUS SERVICES .

69

1. PRINCIPLES OF CONSOLIDATION2. ACCOUNTING RULES AND EVALUATION METHODS

The global consolidation method consists in replacing the value of the securities on handby each of the elements of the assets and liabilities of the subsidiary, then eliminating allreciprocal operations between the parent company and the subsidiary.The share of minority interest in the equity and the results of operations are shownseparately in the consolidated balance sheet and consolidated in the income statements.

1.3 Goodwill

The item « Goodwill » appearing in the assets represents the positive difference between theacquisition value of the shares of BLOM BANK (SWITZERLAND) and the net book value of theseshares at their acquisition date. These differences are amortized on a linear basis over aperiod of 20 years and this is reported as an expense in the income statement.

The Goodwill has been fixed at the exchange rate in force on the acquisition dates and it hasbeen calculated as follows:

It is important to note that the goodwill, which is equal to the difference at the acquisition date,is not modified by the profits recorded after the acquisition date ; these profits beingintegrated in the consolidated shareholders equity. So whatever the future value of theshareholders equity, the goodwill will be amortised on a linear basis.

This goodwill has been amortised on a 20 year period as follows and the amortisation isapplied on the goodwill set in EUR at the historical cost.

The exchange difference resulting from the difference between the amount at the beginning ofthe period (after amortisation) set at the initial exchange rate and the counter value at theexchange rate as at the end of the year, is added to the consolidated reserves. The exchangedifference amounted to EUR. 82 889.52 (negative) as at 31st December 2007.

A. Acquisition value of 20,000 shares ofBLOM BANK SWITZERLAND (100%) :B. Book value of the shares as at 31/12/07The difference being:Converted into EUR at the initial exchange rate

CHF-CHFCHFEUR

29 730 192.8025 192 518.584 537 674.222 743 581.33

Accumulated amortisation from 1988 to 2006Amortisation for 2007:Consequently, the balance of goodwill as at 31.12.2007(after amortisation and conversion into Euros)

EUREUR

EUR

2 518 305.78137 179.07

88 096.48

70

Annex

2. ACCOUNTING RULES AND EVALUATION METHODS

2.1 General

As stated above, the financial statements are prepared and presented in accordance with theregulation CRB 91-01 (Banking Regulation Committee) modified, the regulation CRC 99-07(Accounting Regulation Committee) and the 2000-04 CRC regulation. The rules to be followed forthe preparation of the balance sheet and the income statement are in accordance with theaccounting standards of the banking industry in France. These accounts were prepared inconformity with the conservatism and consistency concepts and the continuity of the evaluationmethod. The consolidated accounts included for the first time the new Romanian Branches whohave joined the group as at the 1st December 2007.

2.2 Accrual basis of accounting

The expenses and the revenues are, usually recorded by using the « accrual basis ofaccounting ». The « Cash Basis » is used in few exceptions, such as documentary creditsand fiduciary deposit commission transactions.

2.3 Foreign currency translation

The financial statements recorded in the local currency of the consolidated company hasbeen translated into euros at the official year end closing rate for the balance sheet, and atan average year rate for the income statement.The exchange difference resulting from the translated net worth at closing as compared toits historical value is posted into a separate account under networth, labelled « CurrencyTranslation Profit » and is added or deducted from the consolidated reserves in the balancesheet.Therefore, the difference resulting from the translated networth at closing as compared to itshistorical value is not accounted for in P&L statement but posted into separate accountamong reserves under networth.Whenever local regulation requires to account as a revenue or a loss any exchangedifference resulting from the translated networth or from any other structural position, areprocessing is carried out in order to neutralize the impact on P&L. This reprocessingconsists in earmarking the exchange difference resulting from the translated networth or anyother structural position within regularization accounts related to capital allocation ofbranches. Said exchange difference resulting from structural position, if unfavourable andentailing an irreversible and final loss, is subject to a provision allowance.

71

2. ACCOUNTING RULES AND EVALUATION METHODS

2.4 Foreign currency transactions

Foreign currency positions are valued on a monthly basis, at the closing official rate ofthe period ; the resulting profits and losses, are accrued. The results of the « SWAP »transactions (spot against forward) are recorded pro rata temporis.

2.5 Local rules

In order to comply with the local regulations, the United Arab Emirates branches are requiredto create a legal reserve amounting to 10 % of the net profit of each year. The appropriation ofthe net profit amount for 2007 is AED 3 883 552 (718 thousand EUR).Moreover, in accordance with the UAE Central Bank request, a general reserve representing2 % of the unclassified loan portfolio has to be maintained in the branches local accounts, Thisreserve is also created as an appropriation of the net profit The appropriation of the net profitamount for 2007 isAED 1 057 183 (196 thousand EUR), and the global amount of this reserve reaches as atDecember’s 2007 AED 10 540 894 (1 950 thousand EUR)In the statutory and consolidated accounts of BLOM BANK FRANCE, the whole net profit isretained. A capital allocation is accounted at the date of the approval of the accounts asrequired the local rules.

2.6 Unpaid loans, doubtful debts and provisions