PORTFOLIO THEORY (ECGE 1218)s6b009aabbba20031.jimcontent.com/download/version/1305853299… ·...

37

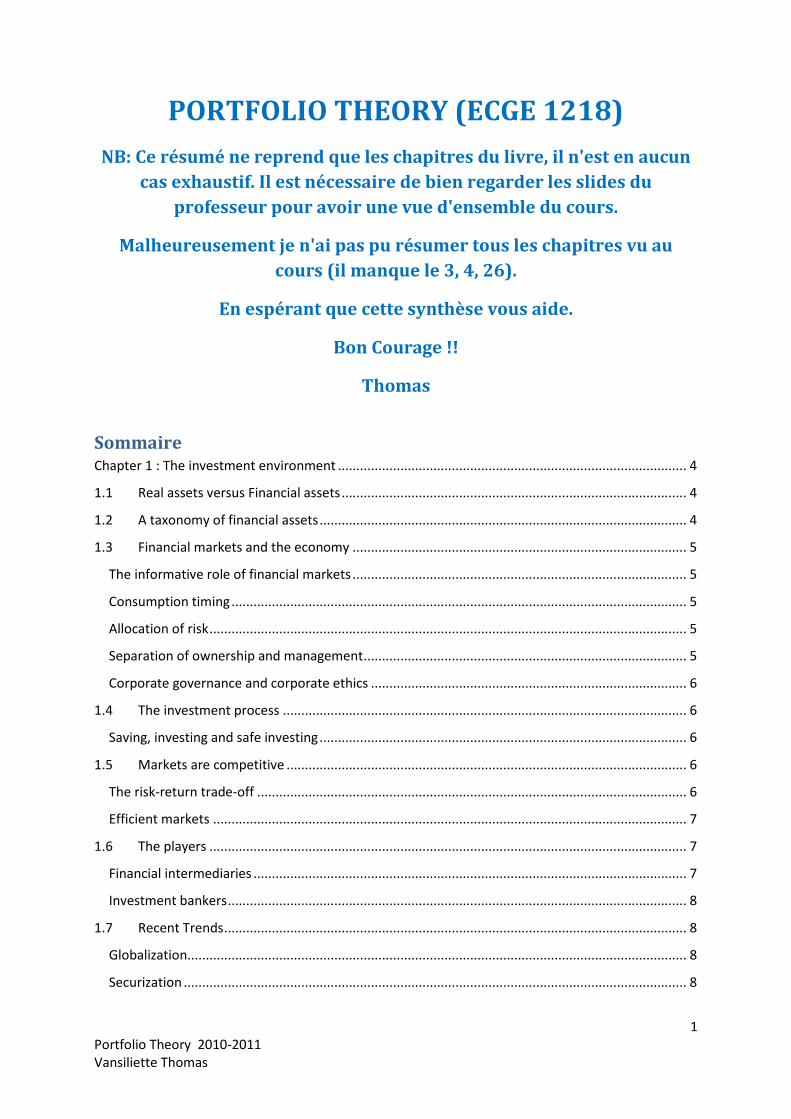

1 Portfolio Theory 2010-2011 Vansiliette Thomas PORTFOLIO THEORY (ECGE 1218) NB: Ce résumé ne reprend que les chapitres du livre, il n'est en aucun cas exhaustif. Il est nécessaire de bien regarder les slides du professeur pour avoir une vue d'ensemble du cours. Malheureusement je n'ai pas pu résumer tous les chapitres vu au cours (il manque le 3, 4, 26). En espérant que cette synthèse vous aide. Bon Courage !! Thomas Sommaire Chapter 1 : The investment environment ............................................................................................... 4 1.1 Real assets versus Financial assets .............................................................................................. 4 1.2 A taxonomy of financial assets .................................................................................................... 4 1.3 Financial markets and the economy ........................................................................................... 5 The informative role of financial markets ........................................................................................... 5 Consumption timing ............................................................................................................................ 5 Allocation of risk .................................................................................................................................. 5 Separation of ownership and management........................................................................................ 5 Corporate governance and corporate ethics ...................................................................................... 6 1.4 The investment process .............................................................................................................. 6 Saving, investing and safe investing .................................................................................................... 6 1.5 Markets are competitive ............................................................................................................. 6 The risk-return trade-off ..................................................................................................................... 6 Efficient markets ................................................................................................................................. 7 1.6 The players .................................................................................................................................. 7 Financial intermediaries ...................................................................................................................... 7 Investment bankers ............................................................................................................................. 8 1.7 Recent Trends .............................................................................................................................. 8 Globalization........................................................................................................................................ 8 Securization ......................................................................................................................................... 8

Transcript of PORTFOLIO THEORY (ECGE 1218)s6b009aabbba20031.jimcontent.com/download/version/1305853299… ·...

1 Portfolio Theory 2010-2011 Vansiliette Thomas

PORTFOLIO THEORY (ECGE 1218)

NB: Ce résumé ne reprend que les chapitres du livre, il n'est en aucun

cas exhaustif. Il est nécessaire de bien regarder les slides du

professeur pour avoir une vue d'ensemble du cours.

Malheureusement je n'ai pas pu résumer tous les chapitres vu au

cours (il manque le 3, 4, 26).

En espérant que cette synthèse vous aide.

Bon Courage !!

Thomas

Sommaire Chapter 1 : The investment environment ............................................................................................... 4

1.1 Real assets versus Financial assets .............................................................................................. 4

1.2 A taxonomy of financial assets .................................................................................................... 4

1.3 Financial markets and the economy ........................................................................................... 5

The informative role of financial markets ........................................................................................... 5

Consumption timing ............................................................................................................................ 5

Allocation of risk .................................................................................................................................. 5

Separation of ownership and management ........................................................................................ 5

Corporate governance and corporate ethics ...................................................................................... 6

1.4 The investment process .............................................................................................................. 6

Saving, investing and safe investing .................................................................................................... 6

1.5 Markets are competitive ............................................................................................................. 6

The risk-return trade-off ..................................................................................................................... 6

Efficient markets ................................................................................................................................. 7

1.6 The players .................................................................................................................................. 7

Financial intermediaries ...................................................................................................................... 7

Investment bankers ............................................................................................................................. 8

1.7 Recent Trends .............................................................................................................................. 8

Globalization ........................................................................................................................................ 8

Securization ......................................................................................................................................... 8

2 Portfolio Theory 2010-2011 Vansiliette Thomas

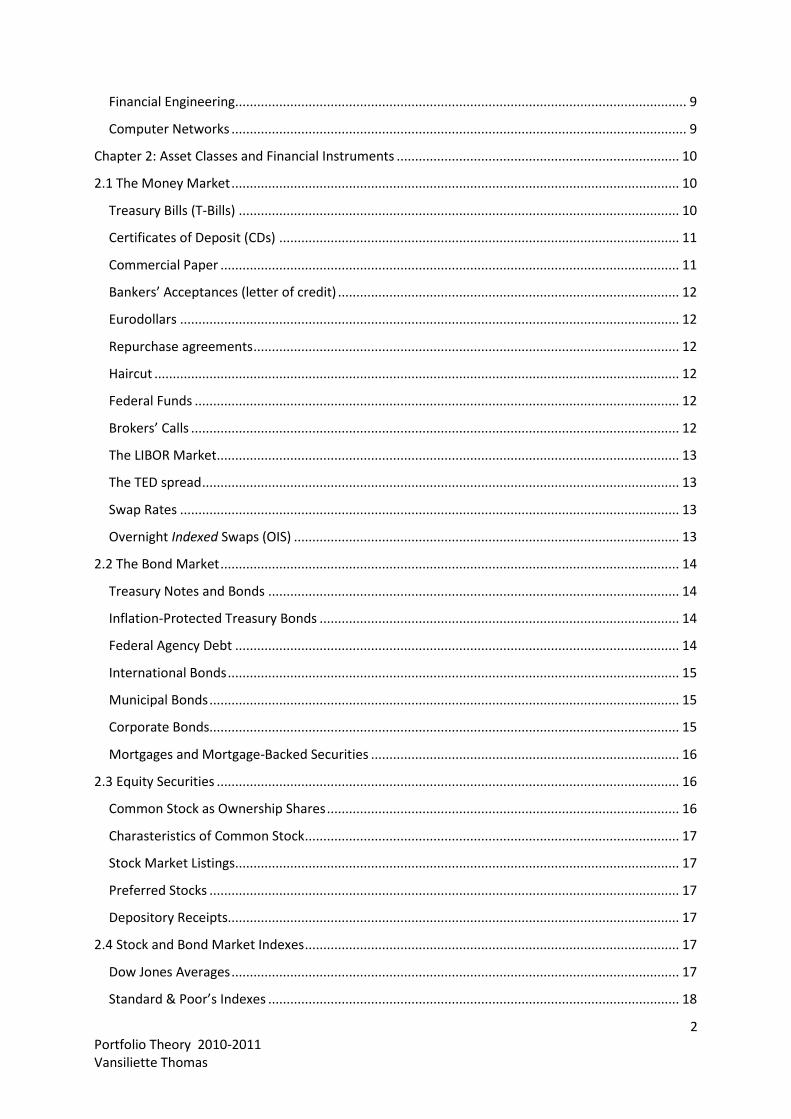

Financial Engineering........................................................................................................................... 9

Computer Networks ............................................................................................................................ 9

Chapter 2: Asset Classes and Financial Instruments ............................................................................. 10

2.1 The Money Market .......................................................................................................................... 10

Treasury Bills (T-Bills) ........................................................................................................................ 10

Certificates of Deposit (CDs) ............................................................................................................. 11

Commercial Paper ............................................................................................................................. 11

Bankers’ Acceptances (letter of credit) ............................................................................................. 12

Eurodollars ........................................................................................................................................ 12

Repurchase agreements .................................................................................................................... 12

Haircut ............................................................................................................................................... 12

Federal Funds .................................................................................................................................... 12

Brokers’ Calls ..................................................................................................................................... 12

The LIBOR Market .............................................................................................................................. 13

The TED spread .................................................................................................................................. 13

Swap Rates ........................................................................................................................................ 13

Overnight Indexed Swaps (OIS) ......................................................................................................... 13

2.2 The Bond Market ............................................................................................................................. 14

Treasury Notes and Bonds ................................................................................................................ 14

Inflation-Protected Treasury Bonds .................................................................................................. 14

Federal Agency Debt ......................................................................................................................... 14

International Bonds ........................................................................................................................... 15

Municipal Bonds ................................................................................................................................ 15

Corporate Bonds................................................................................................................................ 15

Mortgages and Mortgage-Backed Securities .................................................................................... 16

2.3 Equity Securities .............................................................................................................................. 16

Common Stock as Ownership Shares ................................................................................................ 16

Charasteristics of Common Stock ...................................................................................................... 17

Stock Market Listings......................................................................................................................... 17

Preferred Stocks ................................................................................................................................ 17

Depository Receipts........................................................................................................................... 17

2.4 Stock and Bond Market Indexes ...................................................................................................... 17

Dow Jones Averages .......................................................................................................................... 17

Standard & Poor’s Indexes ................................................................................................................ 18

3 Portfolio Theory 2010-2011 Vansiliette Thomas

International Indexes ........................................................................................................................ 18

2.5 Derivative Markets .......................................................................................................................... 18

Options .............................................................................................................................................. 18

Futures Contracts .............................................................................................................................. 18

Chapter 14 : Bond Prices And Yields ..................................................................................................... 19

14.1 Bond Characteristics ...................................................................................................................... 19

Treasury Bonds and Notes ................................................................................................................ 19

Corporate Bonds................................................................................................................................ 20

Yield to Call ........................................................................................................................................ 22

Realized Compound Return versus Yield to Maturity ....................................................................... 22

Chapter 20: Options, Futures and Other Derivatives ............................................................................ 23

20.1 The Option Contract ...................................................................................................................... 23

Option Trading ................................................................................................................................... 23

American and European Options ...................................................................................................... 24

Option List ......................................................................................................................................... 24

20.2 Values of Options at Expiration ..................................................................................................... 25

Call Options ....................................................................................................................................... 25

Put Option ......................................................................................................................................... 26

20.3 Option Strategies ........................................................................................................................... 27

Protective Put .................................................................................................................................... 27

Covered Calls ..................................................................................................................................... 27

Straddle ............................................................................................................................................. 28

Spreads .............................................................................................................................................. 28

20.4 The Put-Call Parity Relationship .................................................................................................... 28

Exotic options .................................................................................................................................... 29

Chapter 22: Futures Markets ................................................................................................................ 30

22.1 The Futures Contract ..................................................................................................................... 30

The Basics of Futures Contracts ........................................................................................................ 30

Existing Contracts .............................................................................................................................. 32

22.2 Mechanics of Trading in Futures Markets ..................................................................................... 33

The Clearinghouse and Open Interest ............................................................................................... 33

The Margin Account and Marking to Market .................................................................................... 34

Cash versus Actual Delivery ............................................................................................................... 34

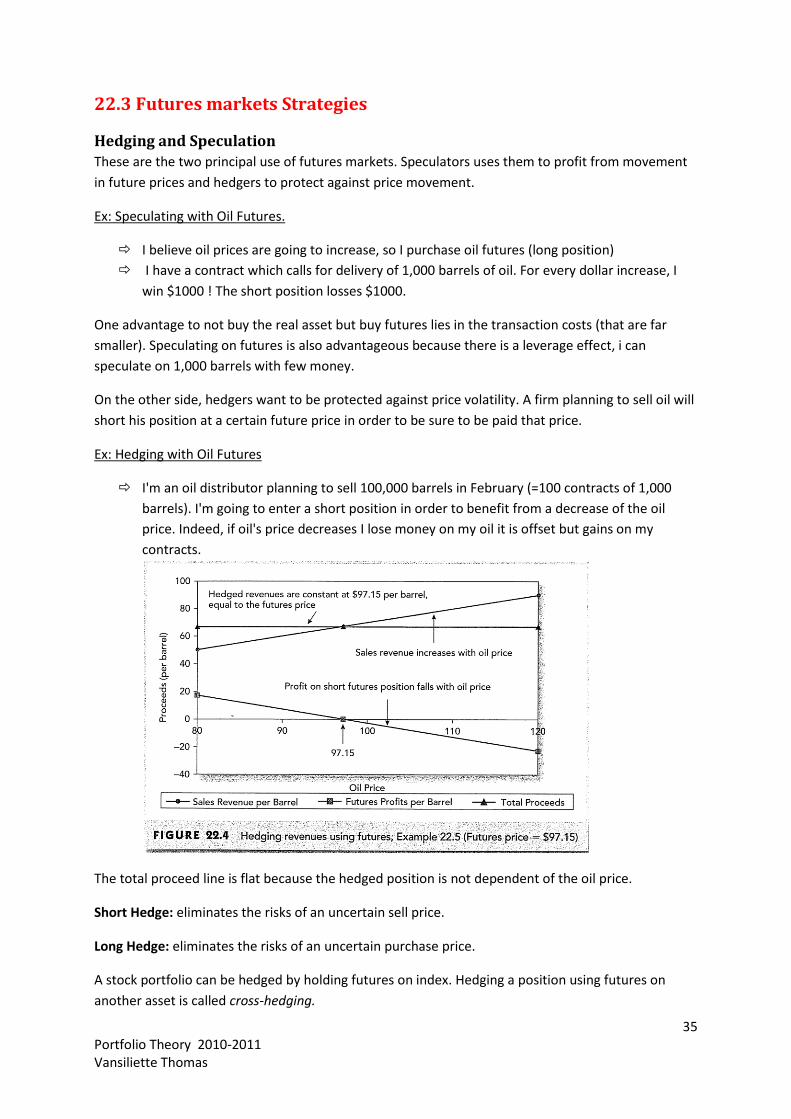

22.3 Futures markets Strategies............................................................................................................ 35

4 Portfolio Theory 2010-2011 Vansiliette Thomas

Hedging and Speculation ................................................................................................................... 35

Basis Risk and Hedging ...................................................................................................................... 36

22.4 The Determination of Futures Prices ............................................................................................ 36

The Spot-Futures Parity Theorem ..................................................................................................... 36

Chapter 1 : The investment environment

1.1 Real assets versus Financial assets

The material wealth of a society is determined by the productive capacity of its economy, that is to

say, the goods and services the members can produce.

This capacity depends on the real assets of the economy (lands, building, machines).

Financial assets (bonds and shares for example) indirectly contribute to the productive capacity,

they are the means by which individuals hold their claims on real assets. Financial assets defines the

allocation of income among investors.

Securities are liabilities of the issuer of the security, if I hold a bond from GM, he is obligated to pay

me interests.

1.2 A taxonomy of financial assets

There are three types of financial assets :

1. fixed income,

2. equity,

3. derivatives.

Fixed-income or debt securities promise a fixed stream of income or a stream of income that is

determined by a formula (ex: corporate bond, T-bills, CDs).

Money market : short term market, it refers to debt securities that are short term, highly marketable

and generally of very low risk

Capital market = Bond Market : long term securities (Treasury Bonds, Corporate Bonds)

5 Portfolio Theory 2010-2011 Vansiliette Thomas

Equity or common stock does not promise any particular payment, this is simply a share of a

corporation.

Derivative securities (options, futures) provide payoffs that are determined by the prices of other

assets such as bonds or stocks. Their value depends on the value of others assets. The primary use is

to hedge risk, they are also useful to take highly speculative positions.

1.3 Financial markets and the economy

The informative role of financial markets

Financial markets play a central role on allocation of capital, investors decide which company will live

and will die. If there are good prospects for the company, investors will bid up stock prices, then the

corporation easily borrows money and easily issue new shares. If there is a black future for the

company, investors will bid down the share prices and the company will have to downsize and

eventually disappear.

The stock market encourages allocation of capital to those firms that appear to have the best

prospects. Unfortunately, we never know of what the future is made! The market sometimes

misjudge a company because of uncertainty, it creates volatility : prices can be far from the

fundamental value of the company.

Consumption timing

Some people earn more than they spend and others spend more than they earn. That is the case for

an active that can save money every month and a retired that earns nothing but spends.

Financial markets allow individuals to store their money, thanks to them, people can make separate

decisions concerning current consumption, and you’re free from constraints imposed by current

earnings.

Allocation of risk

Capital markets allow the risk (inherent to all investments) to be borne1 to the investors who are

willing to take that risk. Some investors are risk intolerant (hedgers), others are ready to bear that

risk (speculators), this is the risk allocation.

Separation of ownership and management

Thanks to financial markets, the owner of the corporation can differ from the managers of the latter.

This gives stability to the firm’s life; this one is no longer dependent to the owner’s life.

But there are drawbacks; managers are not always ready to maximize firm’s values (that is to say

shareholders’ interests). These conflicts of interest are called agency problems.

Several mechanisms have evolved to mitigate potential agency problems:

1 à la charge de

6 Portfolio Theory 2010-2011 Vansiliette Thomas

-Compensation plan : the idea is to tie the income of managers to the success of the firm

(stock options), but this plan can create an incentive for managers to manipulate information to rise

up the stock price).

-Boards of directors can force out underperforming management team,

-Securities analysts and institutional investors can look after the firms and make the life of

poor performers uncomfortable,

-Bad performers are subject to the threat of takeover; shareholder can elect a different

board by launching a proxy contest. Unhappy shareholders try to obtain enough proxies (right to

vote the shares of other shareholder) to take control of the firm and vote in another board. The

other takeover threat comes from other firms; a strong company can acquire an underperforming

one and replace the management team.

Corporate governance and corporate ethics

Financial markets need ethics, if they are not respectful, cases as Enron occurs. Thus, the government

has to make rules in order to regulate markets. The problem is that regulation is not always a good

thing because people will try to deviate from it and take higher risk.

1.4 The investment process

Saving, investing and safe investing

Saving means not spending all of your current income on consumption, this term is often taken to

mean investing in safe assets such as an insured bank account.

Investing is choosing what assets to hold.

A portfolio is simply the collection of investment assets.

Investors make two type of decision while constructing their portfolio :

1) the asset allocation, they choose among asset classes (bonds, shares),

2) the security selection, they choose which particular security to hold within each

asset class.

“Top-down” portfolio construction starts with the asset allocation (the investor first calculate how

much he will spend on each asset class, then he chooses which specific asset he will get).

“Bottom-up” portfolio construction starts with the security selection.

Security analysis involves the valuation of particular securities that might be included in the

portfolio.

1.5 Markets are competitive

The risk-return trade-off

The no-free-lunch rule tells us that you can’t have a high return if you don’t take a high risk.

7 Portfolio Theory 2010-2011 Vansiliette Thomas

The trade-off is the following, if you hold a high risk asset, you will be well remunerated.

If there was no such link between risk and return (same return for all assets), the assets will be

mispriced. Indeed, investors would rush on low risk asset with relatively high return and their price

would skyrocket. On the other hand, nobody would want to buy a high risked asset with a low return

(the price plummets).

Efficient markets

There is no bargaining in the security market.

Passive management : consists in holding highly diversified portfolio without spending effort to

improve investment performance through security analysis.

Active management : consists in attempting to improve performance by identifying mispriced

securities or by timing the performance of an asset class (identify if the market is too high or too

low).

When you are on the market, you compete with all banking analysts.

Assumption of efficient market : The asset price reflects the information available on the underlying

asset. When new information appears, the price is immediately adjusted. The security price equals

the market consensus.

1.6 The players

There are three major players in the financial market:

1) Firms which are net borrowers,

2) Households which are net savers,

3) Governments which are lenders or borrowers (depending on the relationship between

tax revenue and government expenditures). Governments borrow money by issuing

treasury bills/bonds or notes.

Securities are not sold only to individuals; about half of all stock is held by large financial institutions

as pension funds, mutual funds, insurance companies, and banks. These institutions are called

financial intermediaries.

Financial intermediaries

They bring lenders and borrowers together; they include banks, investment companies, insurance

companies and credit unions. They are distinguished from other businesses because most of their

assets are financial.

They are able to lend tons of money because they pool the resources of many small investors.

Because they are lending to many borrowers, the risk is well diversified. They build expertise and can

monitor the risk by making economy of scale and scope.

8 Portfolio Theory 2010-2011 Vansiliette Thomas

Investment bankers

They advise corporation about the price they should set on their securities issuing. The investment

banking handles the marketing of the security in the primary market.

Investment bankers do only operate for businesses and not for individuals. The only difference

between investment and commercial banks is that the latter have generally more deposits than the

former, but they both should have positive deposits.

1.7 Recent Trends

Globalization

U.S investors can participate in foreign investment opportunities in several ways:

- Purchase foreign securities using American Depository Receipts (ADRs), this is

domestically traded securities that represent claims to shares of foreign stocks,

- Purchase foreign securities that are offered in dollars,

- Buy mutual funds that invest internationally,

- Buy derivative securities with payoffs that depend on prices in foreign security markets.

The ADR is denominated in dollars and can be traded on U.S stock exchange but this is simply a claim

on a foreign stock (ex: AB-Inbev quoted on NYSE).

Exchange-traded funds (ETFs, trackers) are a variation on ADRs, they use a depository structure but

buy entire portfolios of stocks (follows an index’s performance).

The instauration of the euro aimed a facilitation of the trades, and integration of European markets.

Securization

The Government National Mortgage Association introduced in 1970, the mortgage pass-through

securities.

These securities aggregate individual home mortgages into relatively homogeneous pools. Investors

can buy GNMA securities and receive interest payments from the mortgage pool.

The banks that originated the mortgages continue to service them (they receive fee for service), but

they no longer own the mortgage investment. Remember the example of Mr De Wolf, with the Texan

farmer’s mortgage hold by ING.

But securizing mortgages, those latter can be traded like another security. It permits to transform an

illiquid asset in a liquid security. The two biggest players on the market were Freddy Mac and Fannie

Mae.

MBS = mortgage backed securities. Today, the majority of home mortgages are pooled into MBS, but

the securitization is also effective for student loans, car loans, etc. When the mortgage loans is

pooled into a MBS, the pass-troughs agency guarantee the underlying mortgage loan. If the

homeowner defaults on the loan, the pass-troughs agency is in trouble; the investor in MBS does not

bear the credit risk.

9 Portfolio Theory 2010-2011 Vansiliette Thomas

Financial Engineering

This is the use of mathematical models and computer-based trading technology to synthesize new

financial products.

This involves unbundling securities (breaking up and allocating cash flows from one security to create

several new securities), or bundling (combining more than one security into a composite security, for

example, merge a stock and a bond into one single security).

Computer Networks

Algorithmic trading : automatic trading. High frequency trading add liquidity to the market.

Flash crash = a very sudden and quick in the Dow Jones index. In less than 20 minutes, the market

loss 9%.

Online trading: it connects a customer directly to a brokerage firm. Online brokerage firms can

process trades more cheaply and therefore can charge lower commissions.

Internet: it allows a huge amount of information to be cheaply and widely available for the public.

10 Portfolio Theory 2010-2011 Vansiliette Thomas

Chapter 2: Asset Classes and Financial Instruments

The asset allocation consists in choosing where you’re going to put your money; you have the choice

between money market securities, bonds, stocks…

The security selection is about selecting specific assets from a more detailed menu.

Financial markets are segmented into money markets (liquid and low-risk)and capital markets (long-

term, risky).

2.1 The Money Market Short-term securities (<1year), liquid and fixed-income securities.

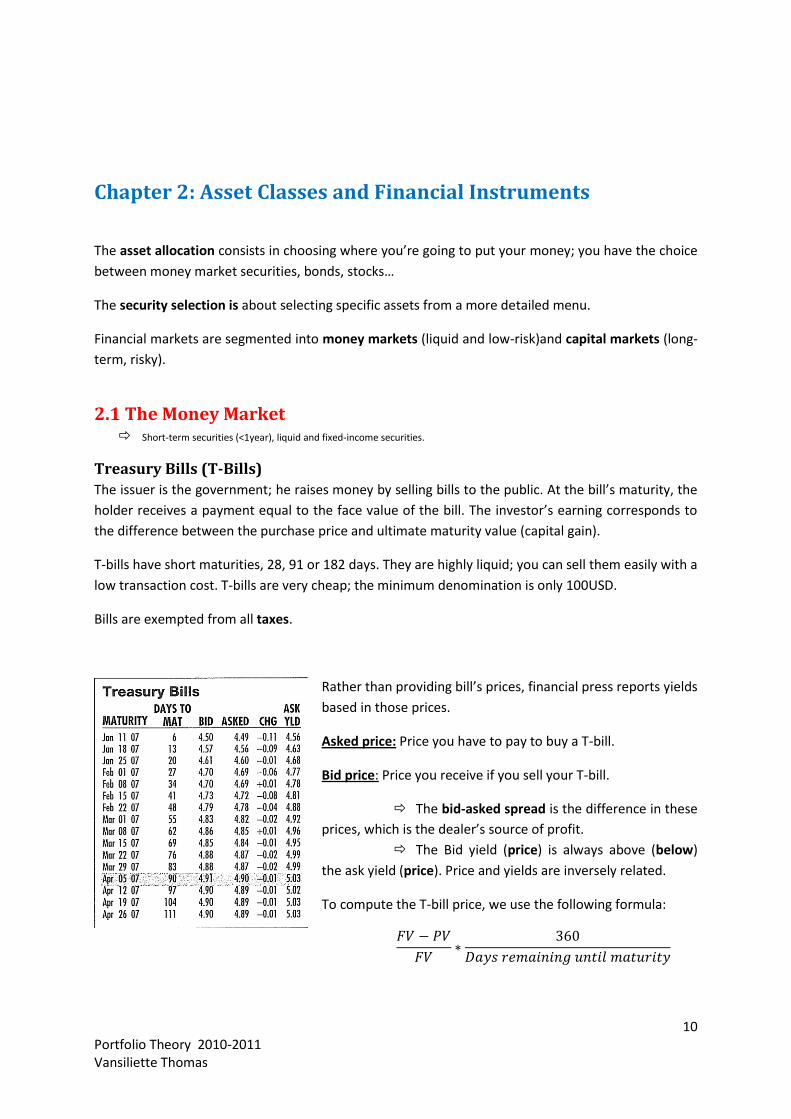

Treasury Bills (T-Bills)

The issuer is the government; he raises money by selling bills to the public. At the bill’s maturity, the

holder receives a payment equal to the face value of the bill. The investor’s earning corresponds to

the difference between the purchase price and ultimate maturity value (capital gain).

T-bills have short maturities, 28, 91 or 182 days. They are highly liquid; you can sell them easily with a

low transaction cost. T-bills are very cheap; the minimum denomination is only 100USD.

Bills are exempted from all taxes.

Rather than providing bill’s prices, financial press reports yields

based in those prices.

Asked price: Price you have to pay to buy a T-bill.

Bid price: Price you receive if you sell your T-bill.

The bid-asked spread is the difference in these

prices, which is the dealer’s source of profit.

The Bid yield (price) is always above (below)

the ask yield (price). Price and yields are inversely related.

To compute the T-bill price, we use the following formula:

11 Portfolio Theory 2010-2011 Vansiliette Thomas

The ASK YLD column gives the bond-equivalent yield (BEY) at the ask (i.e. the offer) is the

annualized return and can be computed as follows:

As an example, we observe in the table that the bill maturing on April 5, days to maturity are 90 and the yield asked is 4.90%.

This means that the dealer wants to sell the bill at a discount from par value of:

4.90 %*(90/360) = 1.225%.

A bill whose par value is 10000$ can be purchased at the price of 100000*(1-0.01225) = 9877.25$

If we want to see at which price the dealer is willing to purchase the bill, we take the bid yield

(4.91%) and we compute: 10000*[1-0.0491*(90/360)] = 9877.25$.

Certificates of Deposit (CDs)

A CD is a time deposit with a bank; the depositor cannot withdraw his money when he wants. A CD

has a fixed term; the bank pays interest and the principal at the end of the term.

Some worthy CDs (over 100.000$) can be negotiated, that is to say they can be sold to another

investor if the owner needs to cash in the certificate before his maturity date.

It is like a saving account, risk-free, with a fixed term (3, 6 months or 1 year) and higher interest

rates.

Commercial Paper

A company can issue commercial paper that worth 100,000$; this is a short-term (less than 1 or 2

months) unsecured debt note. Small investors can invest in commercial papers only indirectly

(through mutual funds, like a SICAV).

Your money is frozen; the commercial paper is backed by a bank to help the borrower to pay off the

paper at maturity (if needed).

Special case : Asset-backed commercial papers : they are issued by financial institutions to

raise funds and invest in other assets. The backing assets are here a pool of mortgages. Mortgage

backed commercial paper (MBCP) = a specific case of the asset-backed commercial paper. MBCP

є MBS family.

Asset-backed commercial papers include backing assets (pool of mortgages: MBS, mortgage-

backed securities, credit loans, student loans, …)

If maturity of the paper < 9 months : no SEC (Security & Exchange Commission) registration

cheaper!

12 Portfolio Theory 2010-2011 Vansiliette Thomas

Bankers’ Acceptances (letter of credit)

It’s an order to a bank by a bank’s customer to pay a sum of money at a future date (within 6

months). When the order is “accepted”, the bank assumes responsibility to pay off the holder of the

acceptance. It can be traded on the secondary market.

Eurodollars

Eurodollars are dollar-denominated deposits at foreign banks or foreign branches of American banks.

Thanks to the location outside the USA; these banks escape regulation by the Federal Reserve.

The London branch of Bank of America (located outside the US) can issue Eurodollars. The yield is

higher because the Eurodollars CDs are considered less liquid and riskier than domestic CDs. The

higher the risk, the higher the return.

During the cold War, the Russian banks wanted to hold USD & the Eurodollars has been a solution:

Russian Banks opened accounts in London

Repurchase agreements

The dealer sells government securities to an investor on an overnight basis, and he promises to buy it

back the next day at a higher price. The dealer takes out a 1-day loan from the investor and the

government securities are used as collateral2.

For example, you sell 10 stocks to your bank on Monday and you receive 100$. The next day, you buy

back your 10 stocks at 110$, therefore you've paid a interest rate of 10%.

The Repo rate is the difference of prices of the past and next day (overnight interest).

Haircut

It exists because some bonds (or repos seller) are more risky than others. Maybe the collateral is very

risky. The haircut imposes a margin on the collateral seller.

The amount of money borrowed is lower than the face value of the bond.

Example: If I got a risky bond which worth 10m$ with a haircut of 20%, I can only borrow 8m$.

Federal Funds

Banks maintain deposits at the Federal Reserve Bank. Each member of the Fed is required to

maintain a minimum balance in a reserve account with the Fed.

Large banks tends to have a shortage3 of federal funds, banks with excess funds can lend them

money. Nowadays, the Fed funds rate is simply the rate of interest on very short-term loans directed

to financial institutions.

Brokers’ Calls

Individuals who buy stocks sometimes borrow part of the fund to pay for the stocks from their

broker. The latter borrows money from the bank, agreeing to pay the bank immediately (on call) if

she requests it.

2 Garantie

3 Manque

13 Portfolio Theory 2010-2011 Vansiliette Thomas

The LIBOR Market

The London Interbank Offered Rate is the rate at which large ban in London lends money among

themselves. This rate is taken as a reference in the European money market.

LIBOR rates are used to measure the ‘international cost of money’ in all major currencies in the world

(USD but also EUR, JPY, GBP, CAD, AUD, CHF, etc.).

It’s also a benchmark rate when a bond is issued with a floating coupon: £ + 100bps (spread).

The TED spread

The TED spread is an indicator of perceived credit risk in the general economy and in the private

banking sector in particular:

T-bills are considered risk-free while LIBOR reflects the credit risk of lending to

commercial banks.

When the TED spread increases, it is a sign that lenders believe the risk of default on

interbank loans (also known as counterparty risk) is increasing.

TED spread = USD Libor rate – T-bill rate

The T-bill is considered risk-free and the USD Libor rate represents the risk of lending to banks.

In 2008, the TED spread has extremely increased.

Swap Rates

Swap rates are used when A wants to pay floating interest and B wants to pay fixe interest. A and B

are going to enter into an interest rate swap(IRS) over a fixed time period.

Overnight Indexed Swaps (OIS)

This is a special case of fixed-to-floating IRS. The benchmark for the floating rate is the overnight cash

rate, which is the Fed fund rate in the US (not Libor or Euribor).

They are for relatively short terms (only out to 1 year). For example, the most popular 3-month OIS

will measure the average of overnight interest rates expected until maturity.

Counterparty risk (the risk bore by investor B) is limited to the difference between the agreed OIS

fixed rate and the actual (floating) OIS observed until maturity. You just have to pay the difference

between the fixed and the floating payment of interests: you do not have to put cash on the table at

the beginning of the transaction: OIS do not require the payment of a principal amount. The risk of

that instrument is related to changes in the Fed Fund Rate. Contrary to Libor loans, there is no

money changing hands before maturity.

14 Portfolio Theory 2010-2011 Vansiliette Thomas

2.2 The Bond Market

The bond market is composed by Treasury notes and bonds, corporate bonds, municipal bonds,

mortgage securities and federal agency debt.

Treasury Notes and Bonds

U.S. government borrows money by issuing Treasury notes and Treasury Bonds. The maturity of T-

notes is up to 10 years and T-bonds’ maturity is between 10 and 30 years.

They make semiannual interest payments called coupon payments. If the interest equal 4%, you get

2$ twice a year. Prices are quoted as a percentage of the par value (if it is written 95%, and par value

is 100, this means that the price is 95$).

The yield to maturity is the interest rate that makes the present value of the bond’s payments equal

to its price.

Inflation-Protected Treasury Bonds

Governments of many countries issue bonds that are linked to an index of the cost of living. This

provides a hedge from inflation risk.

In the U.S., these bonds are called TIPS (Treasury Inflation-Protected Securities); they provide a

stream of income in real dollars.

Federal Agency Debt

Some government agencies issue their own securities to finance their activities. These agencies are

formed to finance a particular sector of the economy when the money might not come from private

sources.

The major mortgage-related agencies are:

• The Federal Home Loan Bank,

• The Federal National Mortgage Association (FNMA or Fannie Mae),

• The Government National Mortgage Association (GNMA or Ginnie Mae),

• The Federal Home Loan Mortgage Corporation (FHLMC or Freddie Mac).

These agencies are government owned or government sponsored, these agencies get the funding by

issuing MBS (Mortgage Backed Securities).

15 Portfolio Theory 2010-2011 Vansiliette Thomas

International Bonds

• Foreign Bond : The international market allows investors to buy bonds from foreign issuer

and firms to borrow abroad.Foreign bonds are issued by a ‘foreign’ borrower in the currency

of the ‘domestic’ country in which it is sold.

• Eurobond : A Eurobond is a bond denominated in a currency other than that of the country

in which it is issued. For example, a American bond issued in London (in $) is called a

Eurodollar bond.

Municipal Bonds

Municipal Bonds are issued by state (e.g. Florida) and local (e.g. Miami) governments and exempted

from the federal income tax.But there is still a tax on the capital gain if they are sold for more than

the price paid by the investor.

The key feature of municipal bonds is their tax-exempt bonds. Because investors pay neither federal

nor state taxes on the interest proceeds they are willing to accept lower yields on these securities.

Hence, investors have to compare the return of tax-exempt bonds and taxable bonds.

Example (ex4 TP1 CFA problems):

Short-term municipal bonds offer yields of 4%, taxable bonds pay 5%. Compare the yields knowing

that the tax bracket is:

a. 0 Bonds have higher payoff (5%>4%).

b. 10% Bonds have a payoff equal to 0.05(1-0.1) = 4.5%, still higher payoffs than Munies.

c. 20% Bonds have a payoff equal to 0.05(1-0.2) = 4%, same payoffs.

d. 30% Bonds have a payoff equal to 0.05(1-0.3) = 3.5%, I prefer Munies.

Therefore, the formula used to compute the after-tax rate of taxable bonds is r(1-t).

Rm is the rate on municipal bonds, if r(1-t)=Rm, I’m indifferent between Munies and Bonds.

When t = 1 – (Rm/r), I’m also indifferent between Munies and Bonds.

The equivalent taxable yield equals: r = Rm/(1-t).

Corporate Bonds

By using corporate bonds, firms can borrow money directly from the public. They are issued by

private firms. The coupons are semi-annual (annual) interest payments in US (EU). They are

subjected to larger default risk than government securities

There are several types of bonds:

1. Secured bonds: they have specific collateral backing them in case of bankruptcy.

2. Debentures: they are unsecured bonds, they don’t have any collateral.

3. Subordinated debentures: they have a lower-priority claim on the firm’s assets in case of

bankruptcy.

16 Portfolio Theory 2010-2011 Vansiliette Thomas

4. Callable bonds: they give the firm the option to repurchase their bond from the holder at a

stipulated bond price. Higher the stipulated price, higher the bond’s price.

5. Convertible bonds: they give the shareholder the option to convert his bond into a stipulated

number of shares of stock.

6. Mortgage bonds: - Issued to buy a property (e.g., real estate). The property is ‘pledged’, i.e.

the lender can seize and liquidate in case of default by the borrower.

7. Equipment trust certificates(ETCs):Typically issued by transportation companies (railroads,

airlines, etc.) to buy equipment (freight cars, railroad engines, airplanes) which serves as

collaterals

8. Collateral trust bonds : The borrower pledge (i.e. commit as collaterals) financial assets, such

as stocks, bonds, notes (held by the trustee)

Mortgages and Mortgage-Backed Securities

A mortgages-backed security can be :

- An ownership claim in a poole of mortgages,

- An obligation that is secured by such a pool.

Mortgage lenders sell packages of the loans they’ve just originated in the secondary market. They sell

their claim tot he cash inflows from the mortgages.

The mortgage originator continues to service the loan, he collects principal and interest payments,

and passes along these payments to purchaser of the mortgage. Mortgage-backed securities are also

called pass-throughs.

GNMA (government national mortgage association) pass-throughs carry a guarantee from the U.S

government. That is to say, the payment of principal and interest are ensured, even if the borrower

defaults on the mortgage. Investors can buy or sell GNMA securities like any other bond.

2.3 Equity Securities

Common Stock as Ownership Shares

Common Stock entitles its owner to one vote during the annual corporation meeting and to a share

in the financial benefits.

The corporation is controlled by a board of directors elected by the shareholders. The board selects

the managers and monitor them to see if they act in the best interests of shareholders.

A corporation whose stock is not publicly traded is said to be closely held.

17 Portfolio Theory 2010-2011 Vansiliette Thomas

Charasteristics of Common Stock

Two important charasteristics :

- Residual claim :Stockholders are the last in line of all those who have a claim on the assets

and income of the corporation. In case of liquidation (bankruptcy), they pass after : tax

authorities, employees, suppliers, bondholders…

- Limited liability :This means that stockholders cannot lose more than their original

investment in case of bankruptcy.

Stock Market Listings

The P/E ratio or the price-earnings ratio, is the ratio oft he current stock price to last’s earnings per

share. This ratio tells us how much stock purchasers must pay per dollar of earnings that the firm

generates.

Preferred Stocks

This stock is almost like a bond, it promises to pay to ist holders a fixed amount of income each year.

Preferred stocks do not provide voting power. Preferred dividends are usually cumulative, unpaid

dividends cumulate and must be paid in full before any dividends is paid to holders of common stock.

Preferred stocks are also different for the tax treatment, they are not tax-deductible expenses

because they are treated as dividends rather than interest. Preferred stock may be callable by the

issuing firm, they are redeemable, they are also convertible into common stock.

Depository Receipts

American Depository Receipts (ADRs) are certificates traded in the U.S. markets that represent

ownership in shares of a foreign company. Each ADR correspond to a share part in a foreign firm.

They are the most common way for U.S. investors to invest in and trade the shares of foreign

coporations.

2.4 Stock and Bond Market Indexes

Dow Jones Averages

The Dow Jones Industrial Average (DJIA) of 30 large corporations (« blue-chip » corporation, the best

values) has been computed since 1896.

Originally, the DJIA was calculated as the simple average of the stocks included in the index, they

simply added up the price of the 30 stocks and divide by 30. DJIA corresponds to a portfolio that

holds one share of each stock, the investment in each company in that portfolio is proportional to

the company’s share price. Therefore, DJIA is called a price-weighted average.

Nowadays, DJIA NO LONGER corresponds to the average prices of the 30 stocks because the

averaging procedure is adjusted whenever a stock splits or pays a stock dividend more than 10%, or

when a company from the index is replaced by another. The divisor is adjusted as soon as there is a

change in the DJIA composition. In the same way that the divisor is updated for stock splits, if one

18 Portfolio Theory 2010-2011 Vansiliette Thomas

firm is dropped from the average and another firm with a different price is added, the divisor has to

be updated to leave the average unchanged by the substitution.

DJIA must reflect the representation of the broad market, there are changes in the index as soon as

there are changes in the economy’s major trends.

Illustration:

A firm wants to split her shares, like this, her stock’s price would drop. The problem is that if the

stock’s price fall, the average will also fall. In order to keep the index representative of the market

price level, you have to change the divisor of the average in order to keep the index unchanged

Why a company would want to split his stock, in order to decreasing her share’s price ?

A perk from splitting the stock’s price is that you can access to small investors. These latters are not

willing to pay a high priced stock because if they do they wouldn’t have enough money to correctly

diversify their portfolio. Imagine that you only have $1000, you cannot buy a single apple’s stock

without having a weight of 30% of IT in your portfolio (because apple’s shares cost $300).

Standard & Poor’s Indexes

The Standard & Poor’s Composite 500 (S&P 500) stock index represents an improvement over the

Dow Jones Averages in two ways:

There are not only 30 firms represented in this index but 500!

S&P 500 is a market-value-weighted index (company’s weight is based on the value, the

capitalisation of the firm => stock’s price*numbers of shares)

International Indexes

DAX (Germany), Nikkei (Japan), FTSE (UK, pronounced footsie), TSX (Canada), Willshire 5000.

2.5 Derivative Markets

Options

Futures Contracts

A futures contract calls for delivery of an asset at a specified delivery or maturity date for an agreed-upon price, called the futures price, to be paid at contract maturity.

The long position is when you have to buy the asset on the delivery date.

The short position commits the trader to deliver the asset at contract maturity.

When you hold a long position, you expect the price to increase.

If I bought a contract saying that I have the right to buy corn at $100 and next week the price hits $120, I made a profit of $20!

When you hold a short position, you expect the price to decrease.

I bought a contract on oil with a price of $100, if it falls at $80, I make a profit by selling!

19 Portfolio Theory 2010-2011 Vansiliette Thomas

Chapter 14 : Bond Prices And Yields

A debt security is a claim on a specified periodic stream of income. Debt Securities are often called

fixed-income securities, indeed they promise a fixed amount of income during a fixed period.

14.1 Bond Characteristics

A bond is a security issued through a borrowing arrangement. The coupon bond obligates the issuer

to make semiannualpayments to the bond’s holder. When the bond matures, the issuer repays the

debt by paying the bond’s par value (=face value).

The coupon rate determines the interest payments, the annual payment is the coupon rate times

the bond’s par value.

The coupon rate, maturity date, and par value of the bond are part of the bond indenture (acte),

which is the contract between the issuer and the bondholder.

Ex : Par Value : $1,000 – Coupon rate : 8%

The buyer of this bond will receive two coupons per year of $40 each.

There are also zero-coupon bonds, they don’t make coupon payments. The bondholder will simply

receive the par value of the bond at maturity.

Those bonds are sold at a price below the par value, like this the bondholder can make a profit at

maturity.

Treasury Bonds and Notes

The difference between treasury bonds and treasury notes is about the maturity.

Treasury Bonds Treasury Notes

Maturity : up to 10 years Maturity : from 10 to 30 years

The bid price and the ask price are quoted in points plus fractions of

of a point. Bonds are usually

sold in denominations of $1,000, the prices are quoted as a percentage of par value.

Ex: Bid price:98 : 07 = 98

= 98.219% That means that the bond price is $982.19.

Ex: Asked price: 99

% = $992.5. Because = 0.25.

Obviously the asked price is higher than the Bid price, this is because the broker has to take

his commission.

20 Portfolio Theory 2010-2011 Vansiliette Thomas

The yield to maturity is a measure of the average rate of return to an investor who purchases the

bond for the asked price and holds it until its maturity.

Accrued Interest and Quoted Bond Prices:The bond prices we can see in the financial pages

are not the prices that investors pay for the bond. The quoted price does not include the interest that

accrues between coupon payment dates. If a bond is purchased between coupon payments, the

buyer must pay the seller for accrued interest.

Therefore there is a difference between the invoice price and the asked price.

Invoice price = Asked price + accrued interest

Ex : If 30 days have passed since the last coupon payment, knowing that there are 182 days

in the semiannual payment. The bond’ seller has the right to ask for the due interest of the

30 days.

Ex : Coupon rate : 8%, annual coupon $80, semiannual coupon $40. Since 30 days have

passed since the last coupon payment is $40*(30/182) = $6.59. If the quoted price of the

bond is $990, then the invoice price will be $990 + $6.59 = $996.59

Corporate Bonds

Corporation borrows money by issuing bonds. Safer bonds with higher ratings (AAA) promise lower

yields to maturity than other riskier bonds.

The default premium can be computed by substracting the yield of the firm’s bond and the

yield of the T-bond.

Call Provisions on Corporate Bonds:Some bonds are issued with call provisions allowing the

issuer to repurchase the bond before the maturity date at a specified call price.

These bonds come with a call protection, an initial time during which the bonds are not callable

(deferred callable bonds).

Corporations are issuing such bonds because of the volatility of market interet rates.

Ex: A firm issued bonds with a coupon rate of 5% when the central bank’s rate was 6%. If the

rate falls to 4%, the firm is tempted by calling the bond and issues a new one with a lower

interest rate.

Therefore, the investor can loose his bond, to compensate that risk callable bonds are issued with

higher coupons and YTM.

21 Portfolio Theory 2010-2011 Vansiliette Thomas

A bond callable at a price of 105 is cheaper than a bond callable at 110. This is because when

i invest my money i prefer to receive 110 than 105! The price of the 105 bond is lower so the

maturity is higher.

Convertible Bonds:

Convertible Bonds give bondholders an option to exchange each bond for a specified number of

shares of common stock of the firm.

The conversion ratio is the number of shares for which each bond may be exchanged,

The market conversion value is the current value of the shares for which the bonds may be

exchanged,

The conversion premium is the excess of the bond value over its conversion value.

Ex: I have a convertible bond (par value $1,000), it’s convertible into 40 shares. If the stock

price is $20, it is not profitable to convert the bonds, if it’s $40 then I have an advantage to

convert my bonds because I’ll get $1,200 instead of $1,000.

Ex: At the $20 price, the bond’s conversion value is $800.

Ex: If the bond is currently selling for $950, the premium would be $150.

Puttable Bonds:

A puttable bond gives the option for the bondholder to extend or retire at the call date.

If the market rates are under the coupon rate, the bondholder will extend the bond’s life. On the

contrary, if the market rates are below the coupon rate, the bondholder will short the bond’s life.

Floating-Rate Bonds:

Interest payments are tied to the market rates. The rate might be adjusted annually to the current T-

bill rate + 2%. This bond pays approximately current market rates.

Preferred Stock:

Preferred Stocks promises to pay a specified stream of dividends. The dividends owed cumulate, and

the common stockholders may not receive any dividends until the preferred stockholders have been

paid in full. Preferred stocks rarely give its holders full voting privileges.

If the firm goes bankrupted, the priority of refund is the following:

1. First, the bondholder,

2. Second, the preferred stock’s holders,

3. Finally, the common stock’s holders.

Unlike interest payments on bonds, dividends of preferred stocks are not considered tax-deductible

expenses to the firm. Therefore, it is less attractive for the firm to issue preferred stocks than bonds.

22 Portfolio Theory 2010-2011 Vansiliette Thomas

Yield to Call

The yield to call is the yield of a callable bond. The issuer of the callable bond says that it can call the

bond if the interest rate falls, it’s interesting for him because he can call back the bond and issue a

new one with a lower coupon rate.

Ex: A bond can be callable at 110% of par value, that is to say $1100. When interest rates

falls, the present value of the bond will rise over par value and when it gets to $1100, the

firm will buy back the bond at the call price (110%).

The call premium is the difference between par value and call price.

At high interest rates the risk of call is negligible because the present value of scheduled payments is

less than the call price; therefore the value of the straight and callable bonds will converge. On the

contrary, at low interest rates the values of the bonds begin to diverge, the difference illustrate the

willingness of the firm to buy back the bond. When the interest rate is very low, the present value

exceeds the call price and the bond is called back.

The yield to call is computed like the yield to maturity except that the time until call replaces time

until maturity, and the call price replaces the par value.

Realized Compound Return versus Yield to Maturity

YTM will equal the rate of return realized over the life of the bond if all coupon are reinvested at an

interest rate equal to the bond’s yield to maturity.

The compound rate of return is calculated as follows :

=

23 Portfolio Theory 2010-2011 Vansiliette Thomas

Chapter 20: Options, Futures and Other Derivatives

20.1 The Option Contract

Call Option: It gives its holder the right to purchase an asset for a specified price called exercise price,

or strike price.

The holder of the call is not required to exercise his call, if it is profitable (that means that the

exercise price is under the market price) he will exercise it, if not he won’t. If the option is not

exercised at the expiration date, she just expires and no longer has value.

The net profit on the call is the value of the option minus the price originally paid to purchase it.

The purchase price of the option is called the premium.

Seller of call option are said to write calls. Their profit depends if the option’s purchaser will exercise

or not. If the purchaser does not exercise his option, the profit of the writer is equivalent to the

option’s premium. If the purchaser exercises his option, the writer risks a loss. Indeed, if the call is

exercised the profit to the option writer is the premium income minus the difference between the

value of the stock (that must be delivered) and the exercise price that is paid for those shares. If that

difference is larger than the initial premium, the writer will incur a loss.

Put Option: It gives its holder the right to sell an asset for a specified price or a strike price on or

before some expiration date. The holder might make a profit if the market value of the asset falls.

Indeed, if the market value falls under $100 and you have the right to sell it for $110, you make a

profit of $10 minus the premium.

A put will be exercised only if the exercise price is greater than the price of the underlying asset.

While profits on call option increasewhen the asset increases in value, profits on put options increase

when the asset value falls.

In the money: When exercising an option is profitable.

Out of the money: When exercising an option is unprofitable.

At the money: When the exercise price and the asset price are equal.

Option Trading

Some option trade on over-the-counter markets. OTC markets offers the advantage that the terms of

the option contract (exercise price, expiration date, number of shares committed) can be adapted to

the needs of the traders. However, the costs of establishing an OTC contract are higher than a classic

one.

Options contracts traded are standardized by specific expiration dates and exercise prices for each

listed option. Like this, all market participants trade in a limited and a uniform set of securities.

24 Portfolio Theory 2010-2011 Vansiliette Thomas

This lowers trading costs and results in a more competitive market.

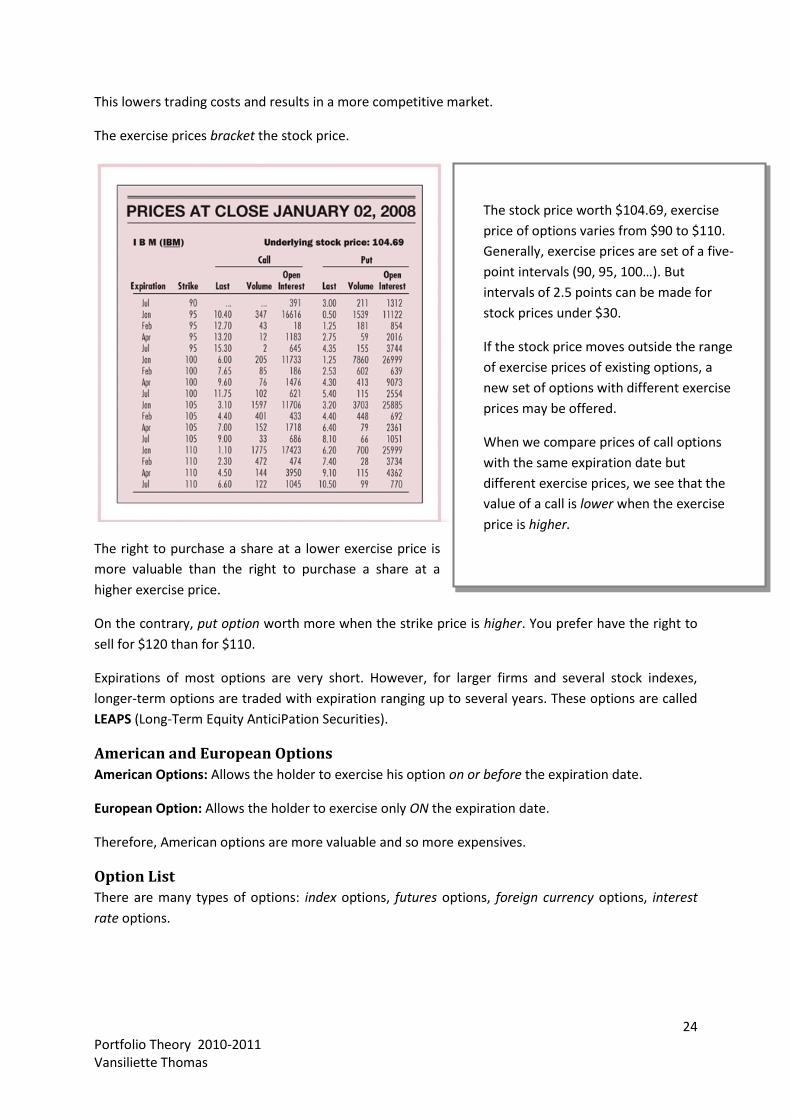

The exercise prices bracket the stock price.

The right to purchase a share at a lower exercise price is

more valuable than the right to purchase a share at a

higher exercise price.

On the contrary, put option worth more when the strike price is higher. You prefer have the right to

sell for $120 than for $110.

Expirations of most options are very short. However, for larger firms and several stock indexes,

longer-term options are traded with expiration ranging up to several years. These options are called

LEAPS (Long-Term Equity AnticiPation Securities).

American and European Options

American Options: Allows the holder to exercise his option on or before the expiration date.

European Option: Allows the holder to exercise only ON the expiration date.

Therefore, American options are more valuable and so more expensives.

Option List

There are many types of options: index options, futures options, foreign currency options, interest

rate options.

The stock price worth $104.69, exercise

price of options varies from $90 to $110.

Generally, exercise prices are set of a five-

point intervals (90, 95, 100…). But

intervals of 2.5 points can be made for

stock prices under $30.

If the stock price moves outside the range

of exercise prices of existing options, a

new set of options with different exercise

prices may be offered.

When we compare prices of call options

with the same expiration date but

different exercise prices, we see that the

value of a call is lower when the exercise

price is higher.

25 Portfolio Theory 2010-2011 Vansiliette Thomas

20.2 Values of Options at Expiration

Call Options

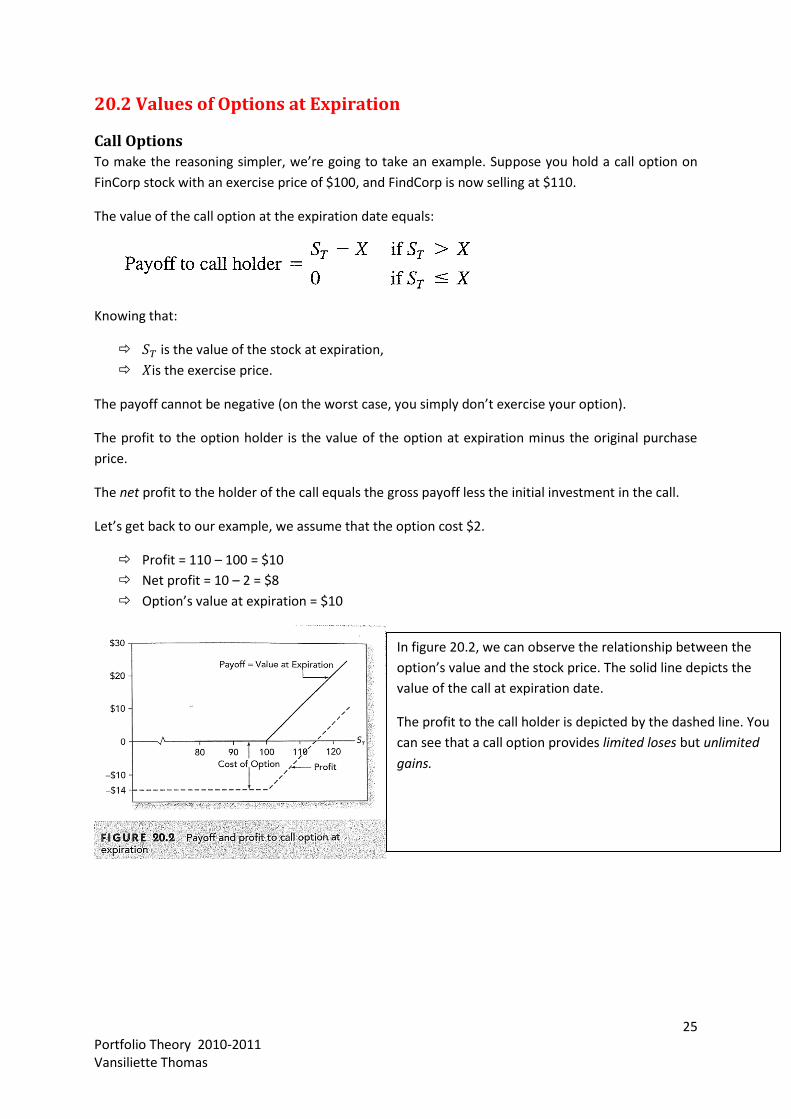

To make the reasoning simpler, we’re going to take an example. Suppose you hold a call option on

FinCorp stock with an exercise price of $100, and FindCorp is now selling at $110.

The value of the call option at the expiration date equals:

Knowing that:

is the value of the stock at expiration,

is the exercise price.

The payoff cannot be negative (on the worst case, you simply don’t exercise your option).

The profit to the option holder is the value of the option at expiration minus the original purchase

price.

The net profit to the holder of the call equals the gross payoff less the initial investment in the call.

Let’s get back to our example, we assume that the option cost $2.

Profit = 110 – 100 = $10

Net profit = 10 – 2 = $8

Option’s value at expiration = $10

In figure 20.2, we can observe the relationship between the

option’s value and the stock price. The solid line depicts the

value of the call at expiration date.

The profit to the call holder is depicted by the dashed line. You

can see that a call option provides limited loses but unlimited

gains.

26 Portfolio Theory 2010-2011 Vansiliette Thomas

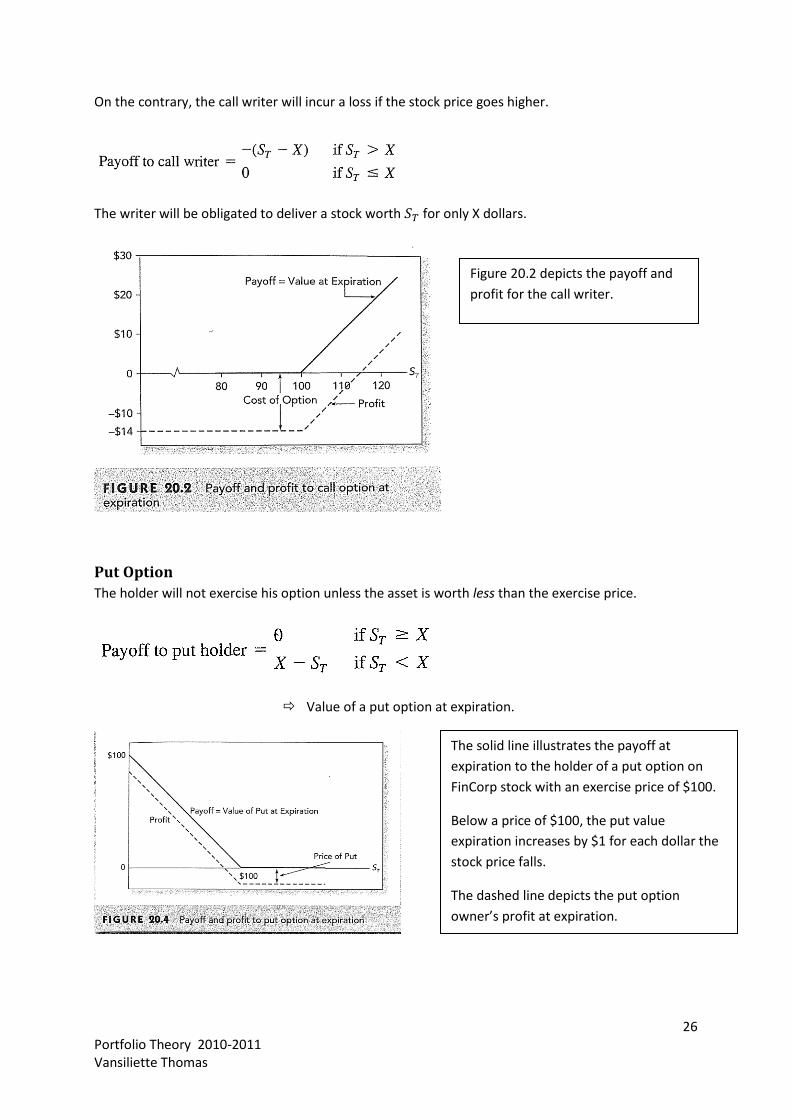

On the contrary, the call writer will incur a loss if the stock price goes higher.

The writer will be obligated to deliver a stock worth for only X dollars.

Put Option

The holder will not exercise his option unless the asset is worth less than the exercise price.

Value of a put option at expiration.

Figure 20.2 depicts the payoff and

profit for the call writer.

The solid line illustrates the payoff at

expiration to the holder of a put option on

FinCorp stock with an exercise price of $100.

Below a price of $100, the put value

expiration increases by $1 for each dollar the

stock price falls.

The dashed line depicts the put option

owner’s profit at expiration.

27 Portfolio Theory 2010-2011 Vansiliette Thomas

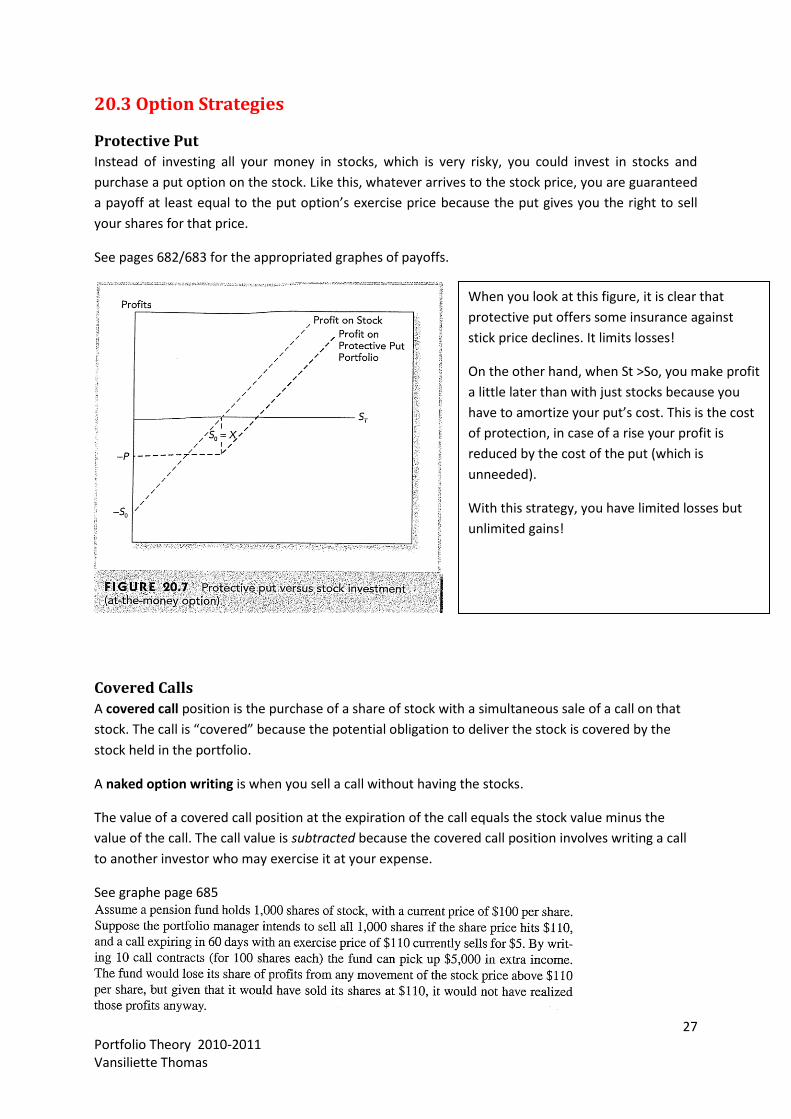

20.3 Option Strategies

Protective Put

Instead of investing all your money in stocks, which is very risky, you could invest in stocks and

purchase a put option on the stock. Like this, whatever arrives to the stock price, you are guaranteed

a payoff at least equal to the put option’s exercise price because the put gives you the right to sell

your shares for that price.

See pages 682/683 for the appropriated graphes of payoffs.

Covered Calls

A covered call position is the purchase of a share of stock with a simultaneous sale of a call on that

stock. The call is “covered” because the potential obligation to deliver the stock is covered by the

stock held in the portfolio.

A naked option writing is when you sell a call without having the stocks.

The value of a covered call position at the expiration of the call equals the stock value minus the

value of the call. The call value is subtracted because the covered call position involves writing a call

to another investor who may exercise it at your expense.

See graphe page 685

When you look at this figure, it is clear that

protective put offers some insurance against

stick price declines. It limits losses!

On the other hand, when St >So, you make profit

a little later than with just stocks because you

have to amortize your put’s cost. This is the cost

of protection, in case of a rise your profit is

reduced by the cost of the put (which is

unneeded).

With this strategy, you have limited losses but

unlimited gains!

28 Portfolio Theory 2010-2011 Vansiliette Thomas

Straddle

A long straddle is established by buying both a call and a put on a stock, each with the same exercise

price X, and the same expiration date T.

Such a strategy is advised when a stock price is about to move a lot in price but the investor doesn’t

know which direction it is going to take.

The worst-case scenario for a straddle is that the stock price doesn’t move at all because both the

call and the put will be worthless. When you straddle, you bet on volatility.

On the contrary, if you write straddle, you must think that the stock is less volatile. You hope that the

stock price will not change before option expiration.

See page 688 for graphes.

Strips: 2 puts + 1 call

Straps: 1 put + 2 calls

Spreads

A spread is a combination of two or more call options (two or more puts) on the same stock with

differing exercise prices or times to maturity. Some options are bought, whereas some options are

written.

Vertical or Money spread: purchase of one option and simultaneous sale of another with different

exercise price.

Horizontal or Time spread: sale or purchase of options with differing expiration dates

See page 689 for graphe.

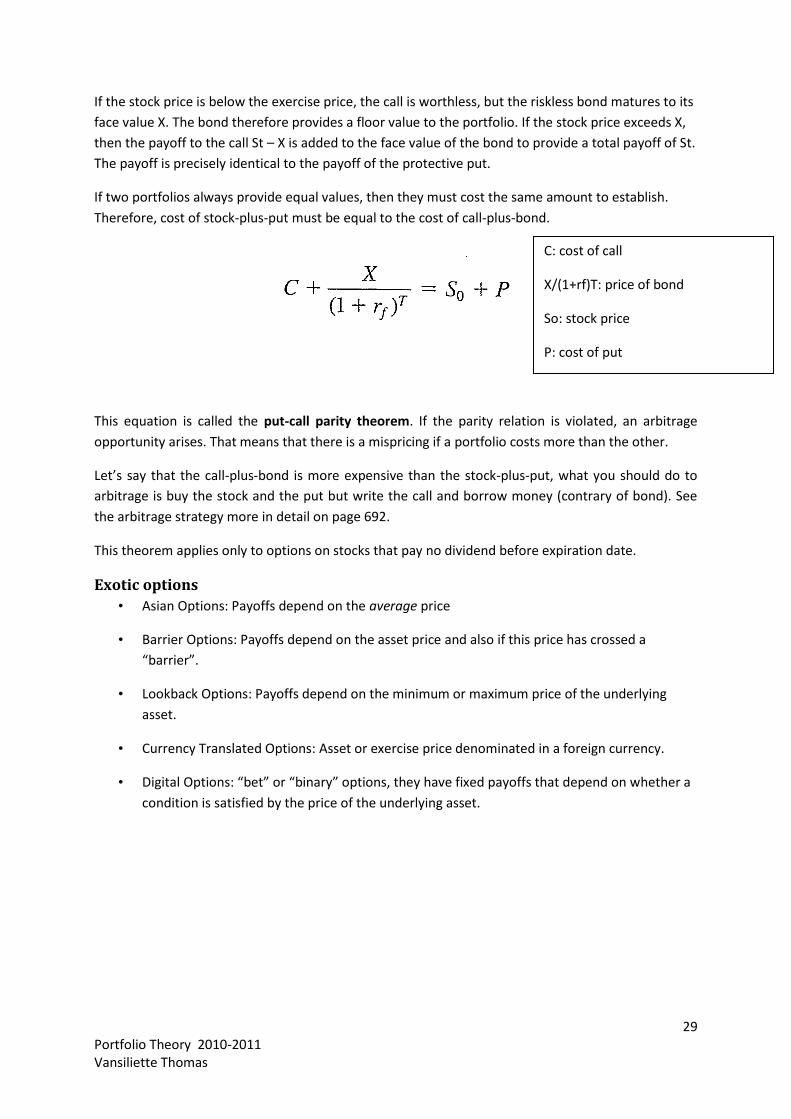

20.4 The Put-Call Parity Relationship Another way to have limited losses but unlimited gains is to combine call option and T-bills (like the

protective put strategy).

The strategy is about buying a call option and, in addition, buying treasury bills with face value equal

to the exercise price of the call and with a maturity equal to the expiration date of the option.

For each option that you hold with exercise price X, you purchase a risk-free zero-coupon with face

value X.

When the bond matures and the option is at expiration, the payoff is:

29 Portfolio Theory 2010-2011 Vansiliette Thomas

If the stock price is below the exercise price, the call is worthless, but the riskless bond matures to its

face value X. The bond therefore provides a floor value to the portfolio. If the stock price exceeds X,

then the payoff to the call St – X is added to the face value of the bond to provide a total payoff of St.

The payoff is precisely identical to the payoff of the protective put.

If two portfolios always provide equal values, then they must cost the same amount to establish.

Therefore, cost of stock-plus-put must be equal to the cost of call-plus-bond.

This equation is called the put-call parity theorem. If the parity relation is violated, an arbitrage

opportunity arises. That means that there is a mispricing if a portfolio costs more than the other.

Let’s say that the call-plus-bond is more expensive than the stock-plus-put, what you should do to

arbitrage is buy the stock and the put but write the call and borrow money (contrary of bond). See

the arbitrage strategy more in detail on page 692.

This theorem applies only to options on stocks that pay no dividend before expiration date.

Exotic options

• Asian Options: Payoffs depend on the average price

• Barrier Options: Payoffs depend on the asset price and also if this price has crossed a

“barrier”.

• Lookback Options: Payoffs depend on the minimum or maximum price of the underlying

asset.

• Currency Translated Options: Asset or exercise price denominated in a foreign currency.

• Digital Options: “bet” or “binary” options, they have fixed payoffs that depend on whether a

condition is satisfied by the price of the underlying asset.

C: cost of call

X/(1+rf)T: price of bond

So: stock price

P: cost of put

30 Portfolio Theory 2010-2011 Vansiliette Thomas

Chapter 22: Futures Markets

Futures and forward are almost like options. Unless that the carrier of an option will not exercise it if

it's not profitable. In the case of futures contracts, there is the obligation to go through with the

agreed-upon transaction.

A forward contract is a commitment today to transact in the future. Futures are useful instruments

for speculators and hedgers.

22.1 The Futures Contract A forward contract is simply a deferred-delivery sale of some asset with the sales price agreed on

now. Each party is willing to lock in the ultimate price to be paid or received for delivery of the

commodity. A forward contract protects each party from future price fluctuations.

In the case of a forward contract, no money changes hand until the delivery date.

In the case of a future contract, there is a daily settle up for any gains or losses on the contract.

The Basics of Futures Contracts

The futures contract calls for the delivery of a commodity at a specified delivery or maturity date, for

an agreed-upon price, called the futures price, to be paid at contract maturity.

The place or means of delivery is specified as well. It is usually made by transfer from warehouse to

warehouse or by wire transfer for financial transaction. But delivery rarely occurs. Parties mostly

close their positions before contract maturity, taking gains or losses in cash.

Long position: The trader commits to purchase the commodity on a delivery date. He buys the

contact.

Short position: The trader commits to delivering the commodity at contract maturity. He sells the

contract.

We use the words "buy" and "sell" figuratively because nobody really buys or sells a contract. This

latter is entered by a mutual agreement. At the time the contract is entered into, no money changes

hands.

Futures contracts rarely result in actual delivery of the underlying asset. Positions are mostly closed

out before the contract expires. Only 1% to 3% of the contracts result in an actual delivery.

31 Portfolio Theory 2010-2011 Vansiliette Thomas

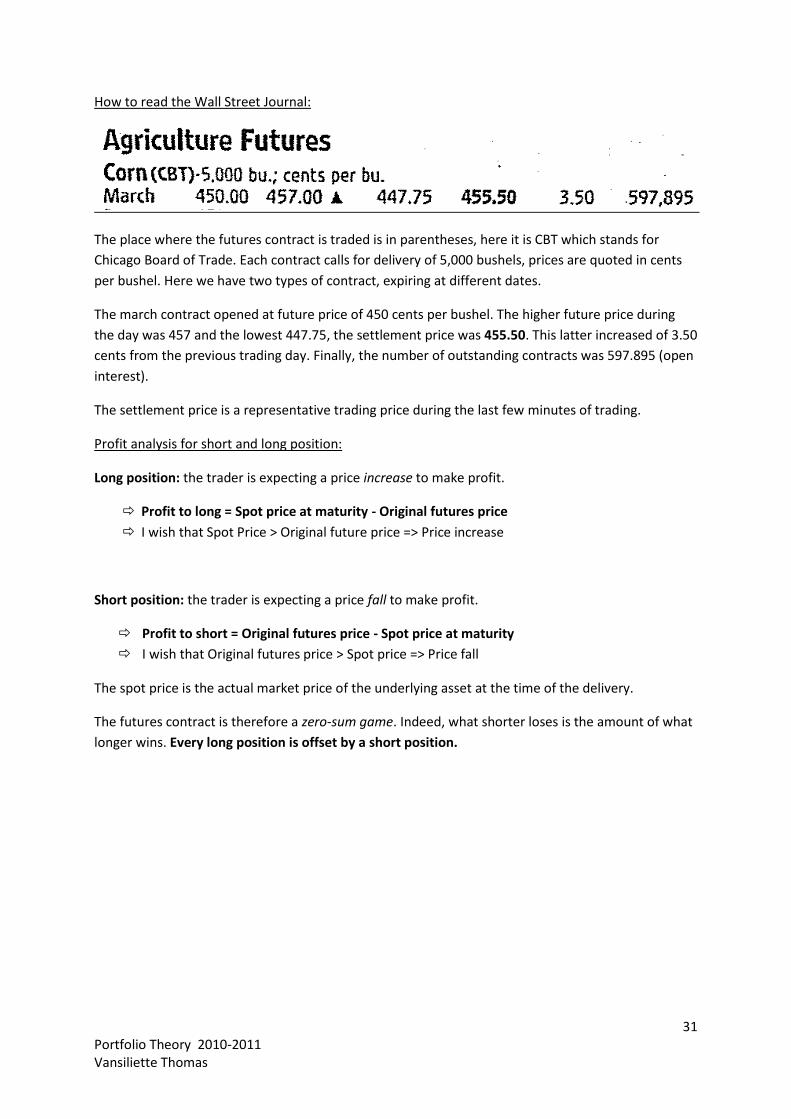

How to read the Wall Street Journal:

The place where the futures contract is traded is in parentheses, here it is CBT which stands for

Chicago Board of Trade. Each contract calls for delivery of 5,000 bushels, prices are quoted in cents

per bushel. Here we have two types of contract, expiring at different dates.

The march contract opened at future price of 450 cents per bushel. The higher future price during

the day was 457 and the lowest 447.75, the settlement price was 455.50. This latter increased of 3.50

cents from the previous trading day. Finally, the number of outstanding contracts was 597.895 (open

interest).

The settlement price is a representative trading price during the last few minutes of trading.

Profit analysis for short and long position:

Long position: the trader is expecting a price increase to make profit.

Profit to long = Spot price at maturity - Original futures price

I wish that Spot Price > Original future price => Price increase

Short position: the trader is expecting a price fall to make profit.

Profit to short = Original futures price - Spot price at maturity

I wish that Original futures price > Spot price => Price fall

The spot price is the actual market price of the underlying asset at the time of the delivery.

The futures contract is therefore a zero-sum game. Indeed, what shorter loses is the amount of what

longer wins. Every long position is offset by a short position.

32 Portfolio Theory 2010-2011 Vansiliette Thomas

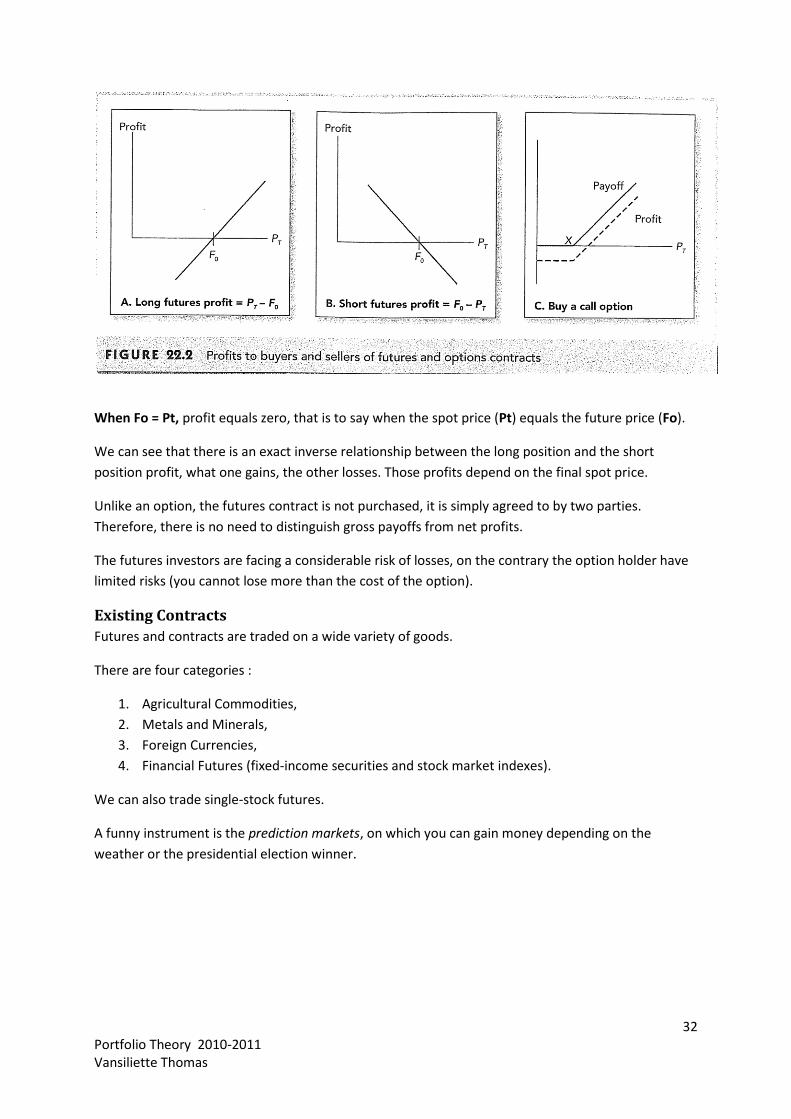

When Fo = Pt, profit equals zero, that is to say when the spot price (Pt) equals the future price (Fo).

We can see that there is an exact inverse relationship between the long position and the short

position profit, what one gains, the other losses. Those profits depend on the final spot price.

Unlike an option, the futures contract is not purchased, it is simply agreed to by two parties.

Therefore, there is no need to distinguish gross payoffs from net profits.

The futures investors are facing a considerable risk of losses, on the contrary the option holder have

limited risks (you cannot lose more than the cost of the option).

Existing Contracts

Futures and contracts are traded on a wide variety of goods.

There are four categories :

1. Agricultural Commodities,

2. Metals and Minerals,

3. Foreign Currencies,

4. Financial Futures (fixed-income securities and stock market indexes).

We can also trade single-stock futures.

A funny instrument is the prediction markets, on which you can gain money depending on the

weather or the presidential election winner.

33 Portfolio Theory 2010-2011 Vansiliette Thomas

22.2 Mechanics of Trading in Futures Markets

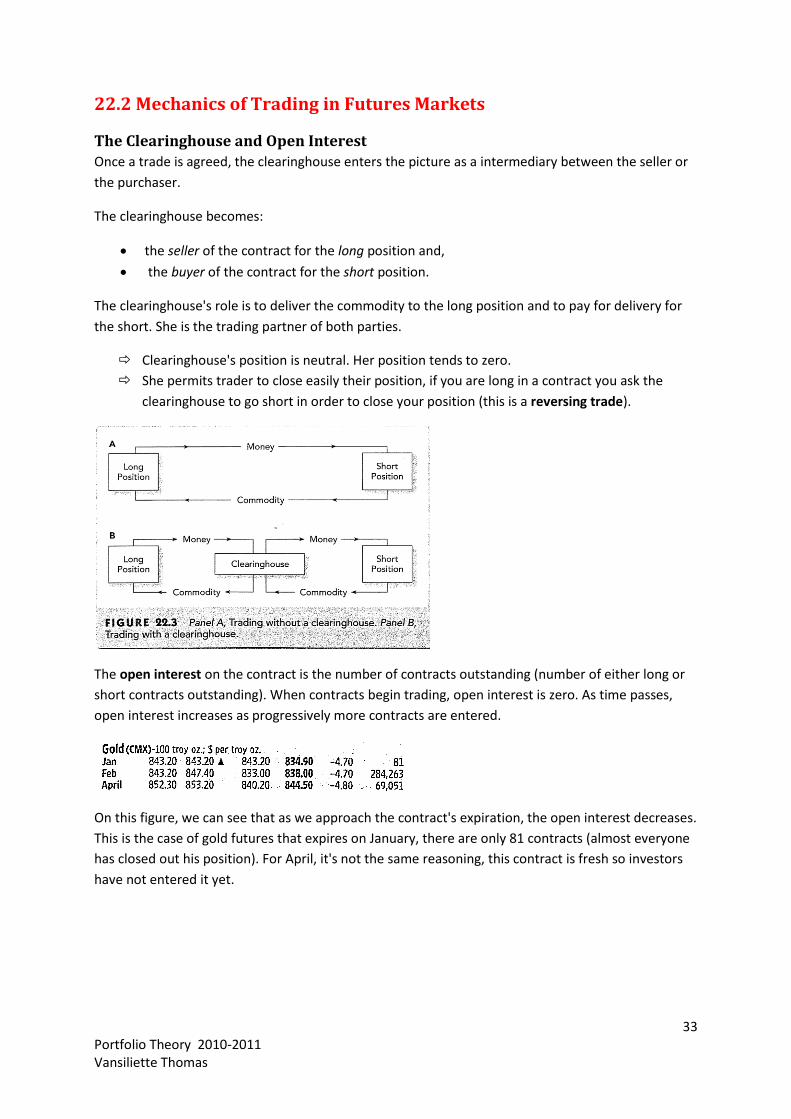

The Clearinghouse and Open Interest

Once a trade is agreed, the clearinghouse enters the picture as a intermediary between the seller or

the purchaser.

The clearinghouse becomes:

the seller of the contract for the long position and,

the buyer of the contract for the short position.

The clearinghouse's role is to deliver the commodity to the long position and to pay for delivery for

the short. She is the trading partner of both parties.

Clearinghouse's position is neutral. Her position tends to zero.

She permits trader to close easily their position, if you are long in a contract you ask the

clearinghouse to go short in order to close your position (this is a reversing trade).

The open interest on the contract is the number of contracts outstanding (number of either long or

short contracts outstanding). When contracts begin trading, open interest is zero. As time passes,

open interest increases as progressively more contracts are entered.

On this figure, we can see that as we approach the contract's expiration, the open interest decreases.

This is the case of gold futures that expires on January, there are only 81 contracts (almost everyone

has closed out his position). For April, it's not the same reasoning, this contract is fresh so investors

have not entered it yet.

34 Portfolio Theory 2010-2011 Vansiliette Thomas

The Margin Account and Marking to Market

The total profit or loss realized by the long trader who buys a contract at time 0 and closes or

reverses it at time t, is just the change in the futures price over the period, Ft - Fo. Short trader earns

Fo - Ft.

The marking to market is the process by which profits or losses accrue. When they making a trade,

each trader establishes a margin account. The margin is a security account when you can find

secured securities (T-bills) or cash that ensures the trader is able to satisfy the obligations of the

futures contract. Both parties must post margin.

The initial margin is usually set between 5% and 15% of the total value of the contract. If the

contracts is on a highly volatile asset, it requires a higher margin.

On any day that futures contracts trade, futures prices may rise or fall. And every day, the

clearinghouse states if we are in gain or losses. If the corn's price rises, the clearinghouse credits the

margin account of the long position and takes this amount from the short position's margin account.

This daily setting is called marking to market.

This marking to market only stands for futures contracts.

Forward contracts are simply held until maturity and no funds are transferred until that date,

although the contracts may be traded.