Le projet Mer Rouge –Mer Morte - cmimarseille.org · Eau potable : 850 Mm 3 Transfertsaumures:...

17

#WorldInCommon AGENCE FRANÇAISE DE DÉVELOPPEMENT | FRENCH DEVELOPMENT AGENCY Le projet Mer Rouge – Mer Morte Atelier régional sur les instruments économiques dans la gestion de la demande en eau en Méditerranée 13 avril 2018 Frédéric Maurel

Transcript of Le projet Mer Rouge –Mer Morte - cmimarseille.org · Eau potable : 850 Mm 3 Transfertsaumures:...

#WorldInCommonAGENCE FRANÇAISE DE DÉVELOPPEMENT | FRENCH DEVELOPMENT AGENCY

Le projet Mer Rouge – Mer Morte

Atelier régional sur les instruments économiques dans la gestion de la demande en eau en Méditerranée

13 avril 2018

Frédéric Maurel

2

Objectifs

Production d’eau potable par dessalement

Sauvegarde de la Mer Morte par transfert depuis la Mer Rouge

Renforcement de la coopérationrégionale dans le secteur de l’eau

05.09.2017 Mer Rouge – Mer Morte

3

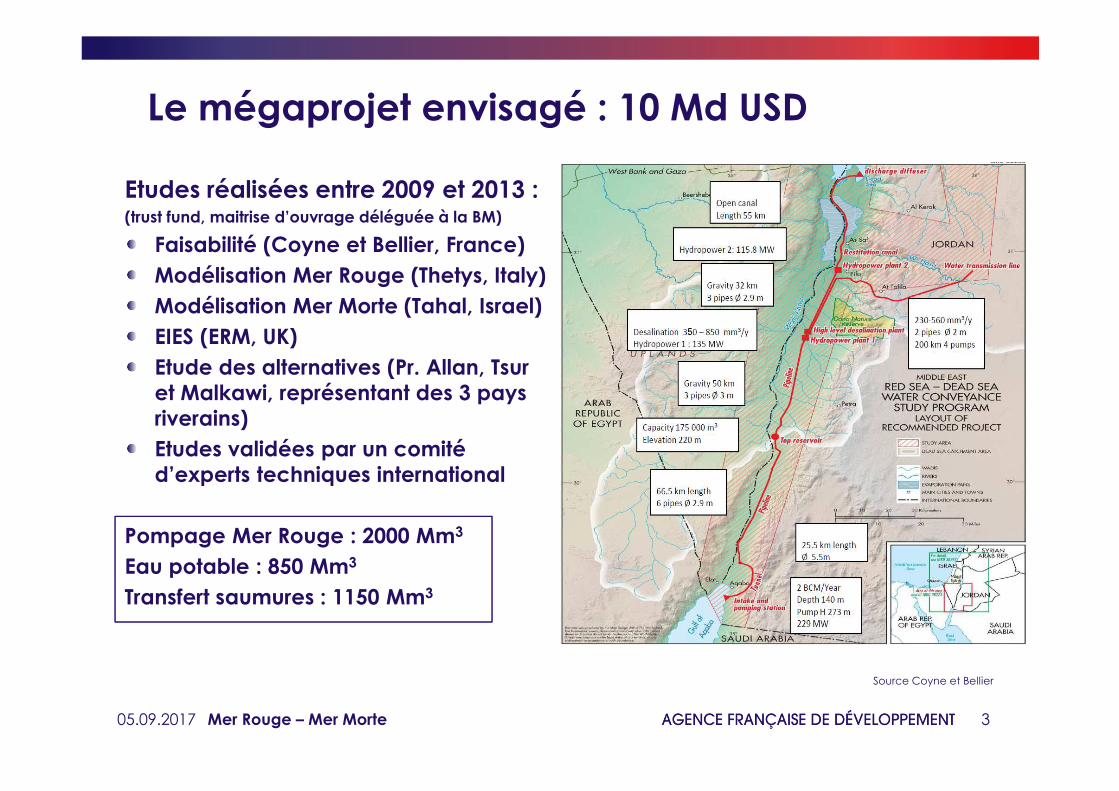

Le mégaprojet envisagé : 10 Md USD

Etudes réalisées entre 2009 et 2013 :(trust fund, maitrise d’ouvrage déléguée à la BM)

Faisabilité (Coyne et Bellier, France)

Modélisation Mer Rouge (Thetys, Italy)

Modélisation Mer Morte (Tahal, Israel)

EIES (ERM, UK)

Etude des alternatives (Pr. Allan, Tsuret Malkawi, représentant des 3 pays riverains)

Etudes validées par un comitéd’experts techniques international

Pompage Mer Rouge : 2000 Mm3

Eau potable : 850 Mm3

Transfert saumures : 1150 Mm3

Source Coyne et Bellier

05.09.2017 Mer Rouge – Mer Morte

4

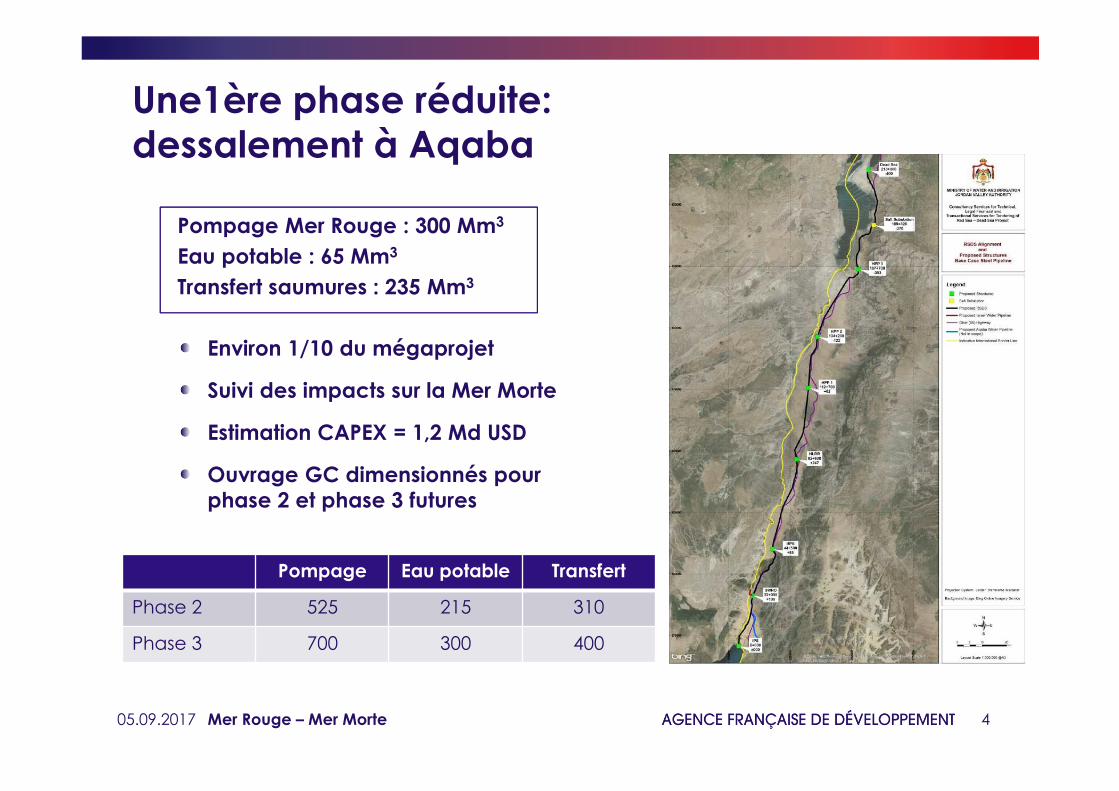

Une1ère phase réduite: dessalement à Aqaba

Pompage Mer Rouge : 300 Mm3

Eau potable : 65 Mm3

Transfert saumures : 235 Mm3

Environ 1/10 du mégaprojet

Suivi des impacts sur la Mer Morte

Estimation CAPEX = 1,2 Md USD

Ouvrage GC dimensionnés pour phase 2 et phase 3 futures

Pompage Eau potable Transfert

Phase 2 525 215 310

Phase 3 700 300 400

05.09.2017 Mer Rouge – Mer Morte

5

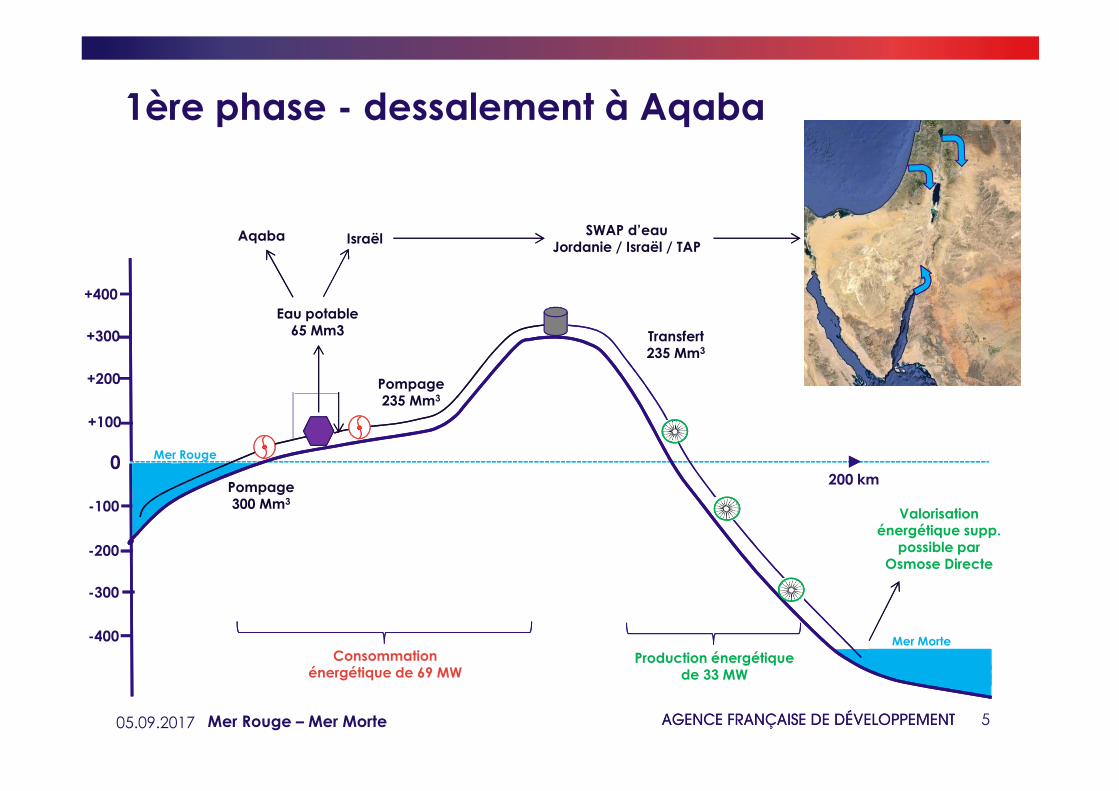

1ère phase - dessalement à Aqaba

0

-100

-200

-300

-400

+100

+200

+300

+400

Pompage300 Mm3

Mer Rouge

Mer Morte

Eau potable 65 Mm3

Pompage235 Mm3

Transfert235 Mm3

Production énergétique de 33 MW

Consommation énergétique de 69 MW

Valorisation énergétique supp.

possible par Osmose Directe

SWAP d’eau Jordanie / Israël / TAP

Aqaba

200 km

Israël

05.09.2017 Mer Rouge – Mer Morte

6

« SWAP » d’eau avec Israel

SWAP Jordanie/Israël :

o Au Nord Israël vend de l’eau du Lac Tibériade pour les Gouvernorats du

Nord de la jordanie(35 à 50 MMC / an)

o Au Sud : la Jordanie vend l’eaudessalée à Israël (Eilat)

Accord Israélo-Palestinien :

o Fourniture de 50 Mm3 aux TAP

o Accord en cours de négociations

Lac Tibériade

Gouvernorats du Nord (Irbid,

Jerash, Asloun)

RDS dessalement 1ère phase

Eilat

Washington, 9 decembre 2013

Followed by agreement between Israel and Jordan 26 feb 2015

05.09.2017 Mer Rouge – Mer Morte

7

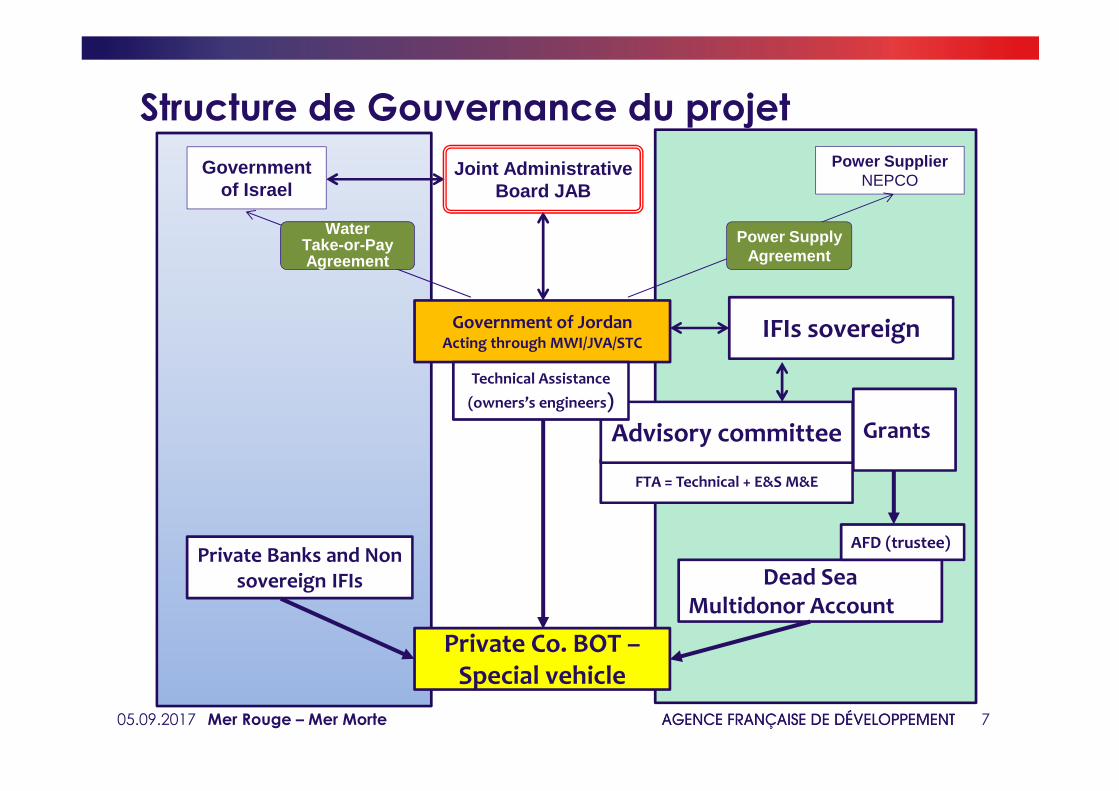

Structure de Gouvernance du projet

Private Co. BOT –Special vehicle

Government of JordanActing through MWI/JVA/STC

Private Banks and Non sovereign IFIs

Grants

Dead Sea Multidonor Account

AFD (trustee)

IFIs sovereign

FTA = Technical + E&S M&E

Advisory committee

Technical Assistance

(owners’s engineers)

Joint Administrative Board JAB

Government of Israel

Power SupplierNEPCO

WaterTake-or-Pay Agreement

Power Supply Agreement

05.09.2017 Mer Rouge – Mer Morte

8

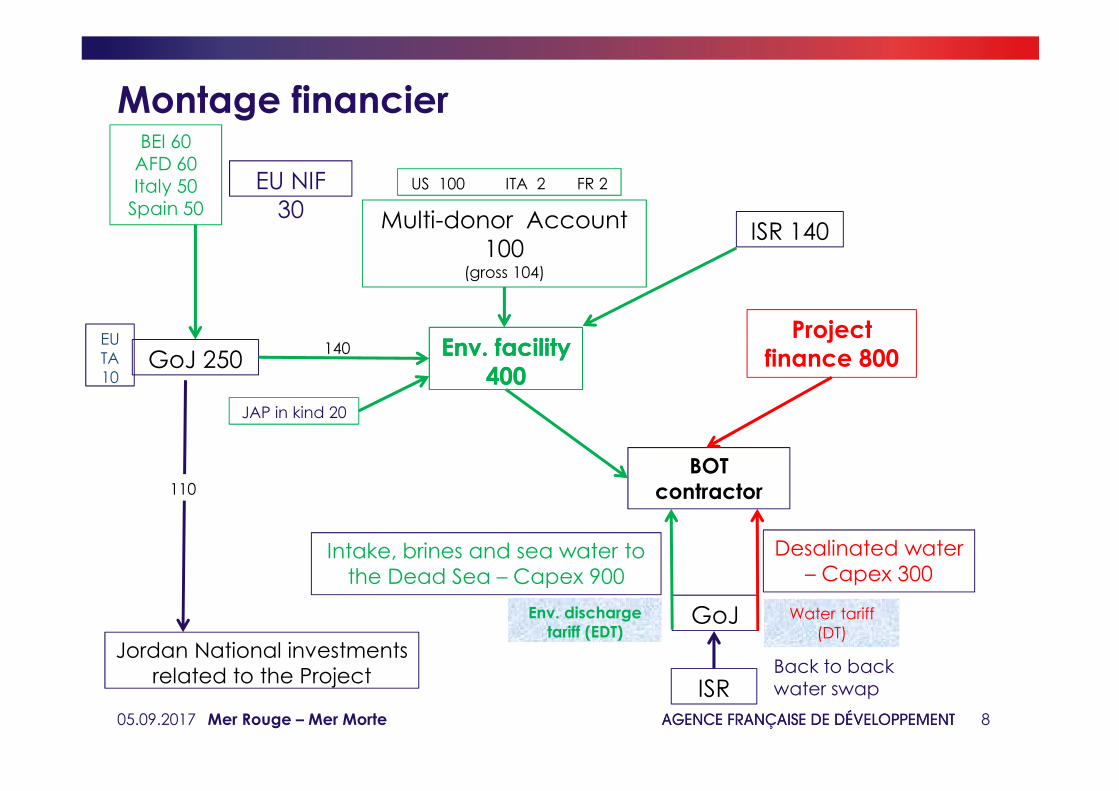

Montage financier

ISR

EU NIF 30

BEI 60AFD 60Italy 50

Spain 50

BOT contractor

ISR 140

GoJ 250

Multi-donor Account100

(gross 104)

Intake, brines and sea water to the Dead Sea – Capex 900

Desalinated water – Capex 300

GoJ

Back to backwater swap

Env. facility400

Env. facility400

Project finance 800

Water tariff (DT)

Env. discharge tariff (EDT)

US 100 ITA 2 FR 2

JAP in kind 20

Jordan National investmentsrelated to the Project

EU TA 10

140

110

05.09.2017 Mer Rouge – Mer Morte

9

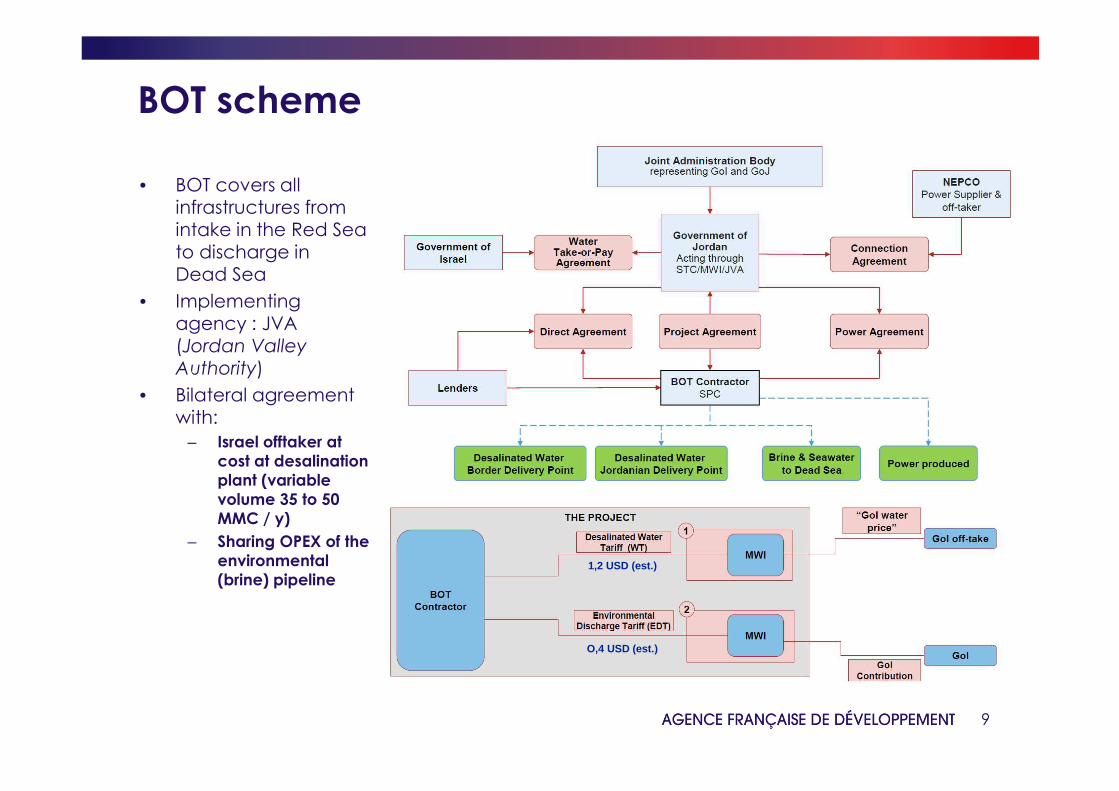

BOT scheme

• BOT covers all infrastructures from intake in the Red Sea to discharge in Dead Sea

• Implementing agency : JVA (Jordan Valley

Authority)

• Bilateral agreement with:

– Israel offtaker at cost at desalination plant (variable volume 35 to 50 MMC / y)

– Sharing OPEX of the environmental (brine) pipeline

1,2 USD (est.)

O,4 USD (est.)

10

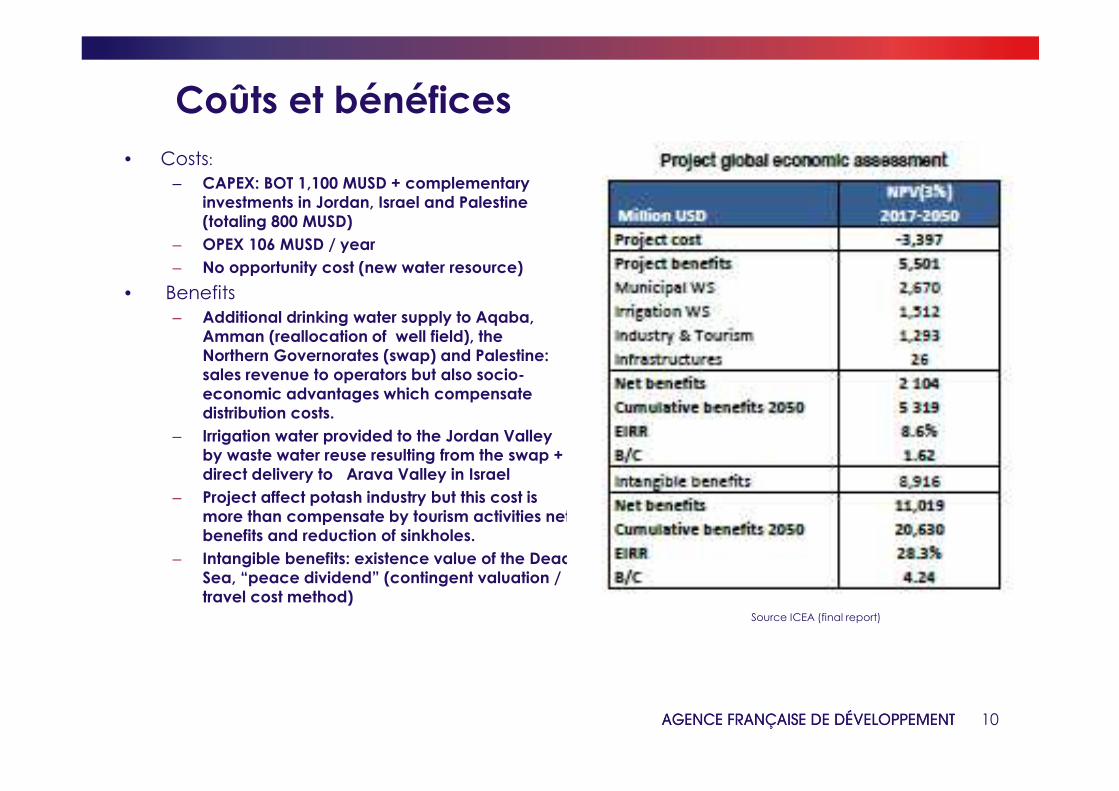

• Costs:

– CAPEX: BOT 1,100 MUSD + complementary investments in Jordan, Israel and Palestine (totaling 800 MUSD)

– OPEX 106 MUSD / year

– No opportunity cost (new water resource)

• Benefits

– Additional drinking water supply to Aqaba, Amman (reallocation of well field), the Northern Governorates (swap) and Palestine: sales revenue to operators but also socio-economic advantages which compensate distribution costs.

– Irrigation water provided to the Jordan Valley by waste water reuse resulting from the swap + direct delivery to Arava Valley in Israel

– Project affect potash industry but this cost is more than compensate by tourism activities net benefits and reduction of sinkholes.

– Intangible benefits: existence value of the Dead Sea, “peace dividend” (contingent valuation / travel cost method)

Coûts et bénéfices

Source ICEA (final report)

11

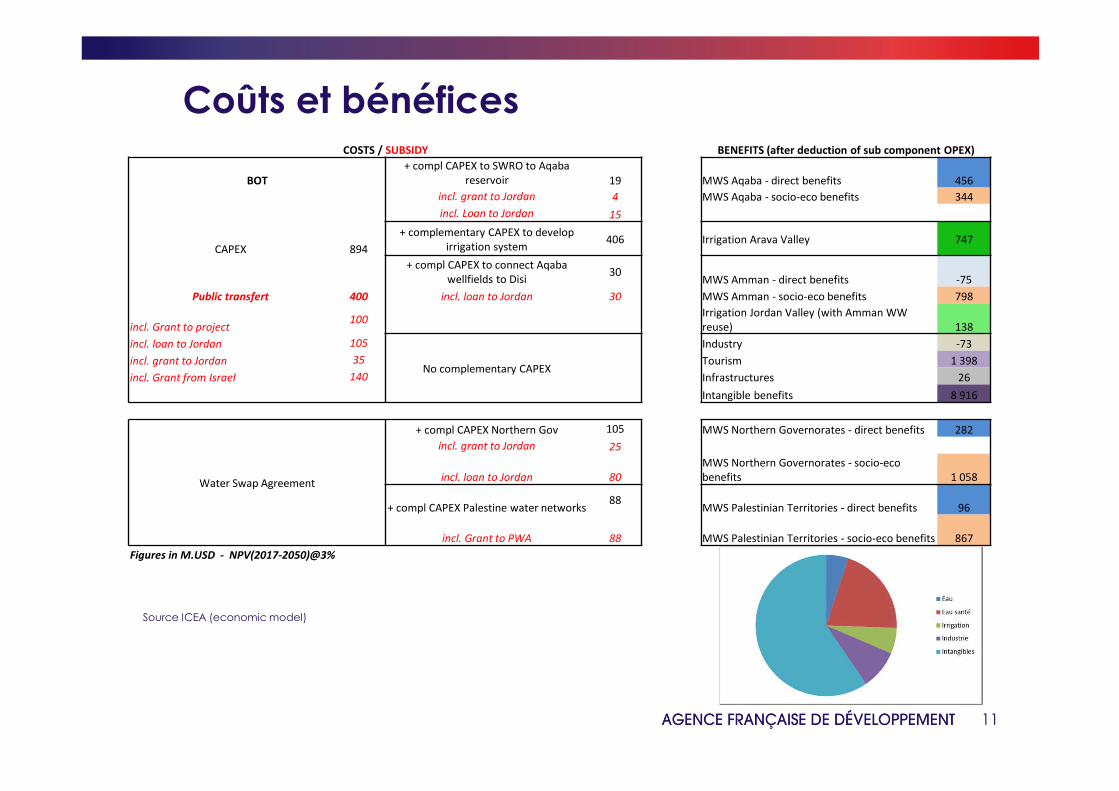

Coûts et bénéfices

Source ICEA (economic model)

COSTS / SUBSIDY BENEFITS (after deduction of sub component OPEX)

BOT

+ compl CAPEX to SWRO to Aqaba

reservoir 19 MWS Aqaba - direct benefits 456

incl. grant to Jordan 4 MWS Aqaba - socio-eco benefits 344

incl. Loan to Jordan 15

CAPEX 894

+ complementary CAPEX to develop

irrigation system406 Irrigation Arava Valley 747

+ compl CAPEX to connect Aqaba

wellfields to Disi 30

MWS Amman - direct benefits -75

Public transfert 400 incl. loan to Jordan 30 MWS Amman - socio-eco benefits 798

incl. Grant to project100

Irrigation Jordan Valley (with Amman WW

reuse) 138

incl. loan to Jordan 105

No complementary CAPEX

Industry -73

incl. grant to Jordan 35 Tourism 1 398

incl. Grant from Israel 140 Infrastructures 26

Intangible benefits 8 916

Water Swap Agreement

+ compl CAPEX Northern Gov 105 MWS Northern Governorates - direct benefits 282

incl. grant to Jordan 25

incl. loan to Jordan 80

MWS Northern Governorates - socio-eco

benefits 1 058

+ compl CAPEX Palestine water networks88

MWS Palestinian Territories - direct benefits 96

incl. Grant to PWA 88 MWS Palestinian Territories - socio-eco benefits 867

Figures in M.USD - NPV(2017-2050)@3%

12

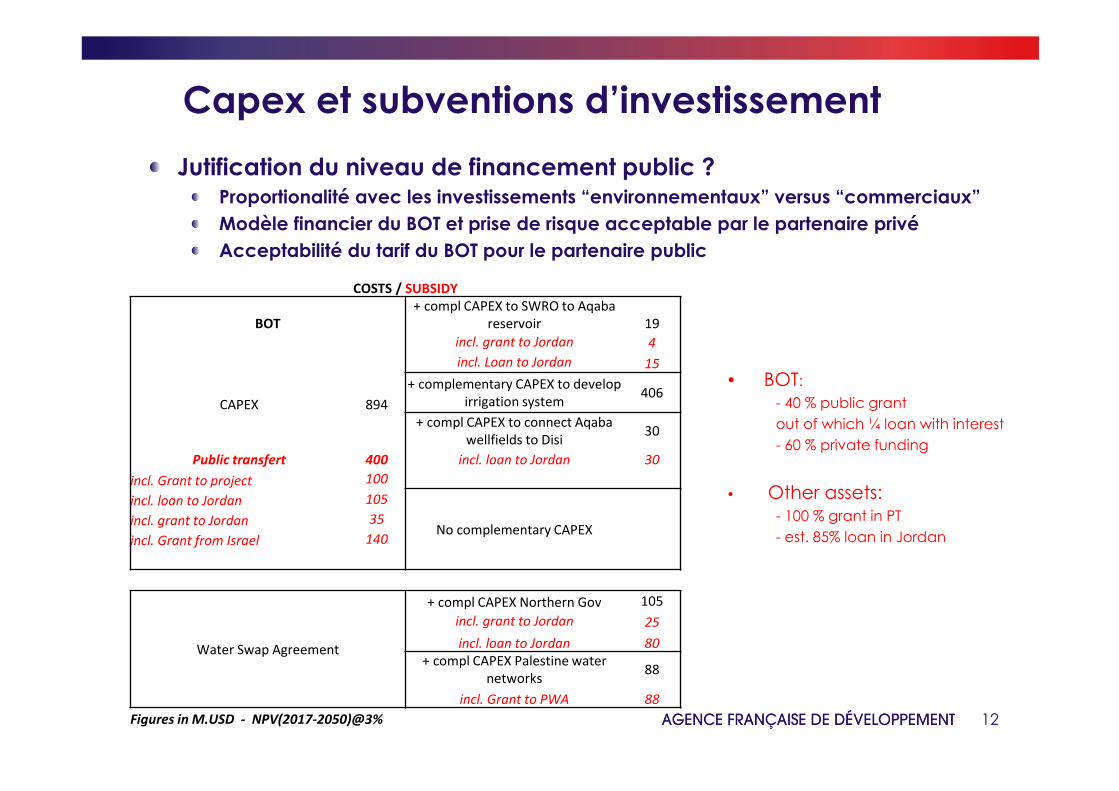

Capex et subventions d’investissement

• BOT:

- 40 % public grant

out of which ¼ loan with interest

- 60 % private funding

• Other assets:- 100 % grant in PT

- est. 85% loan in Jordan

Jutification du niveau de financement public ?Proportionalité avec les investissements “environnementaux” versus “commerciaux”

Modèle financier du BOT et prise de risque acceptable par le partenaire privé

Acceptabilité du tarif du BOT pour le partenaire public

COSTS / SUBSIDY

BOT

+ compl CAPEX to SWRO to Aqaba

reservoir 19

incl. grant to Jordan 4

incl. Loan to Jordan 15

CAPEX 894

+ complementary CAPEX to develop

irrigation system406

+ compl CAPEX to connect Aqaba

wellfields to Disi 30

Public transfert 400 incl. loan to Jordan 30

incl. Grant to project 100

incl. loan to Jordan 105

No complementary CAPEXincl. grant to Jordan 35

incl. Grant from Israel 140

Water Swap Agreement

+ compl CAPEX Northern Gov 105

incl. grant to Jordan 25

incl. loan to Jordan 80

+ compl CAPEX Palestine water

networks88

incl. Grant to PWA 88

Figures in M.USD - NPV(2017-2050)@3%

13

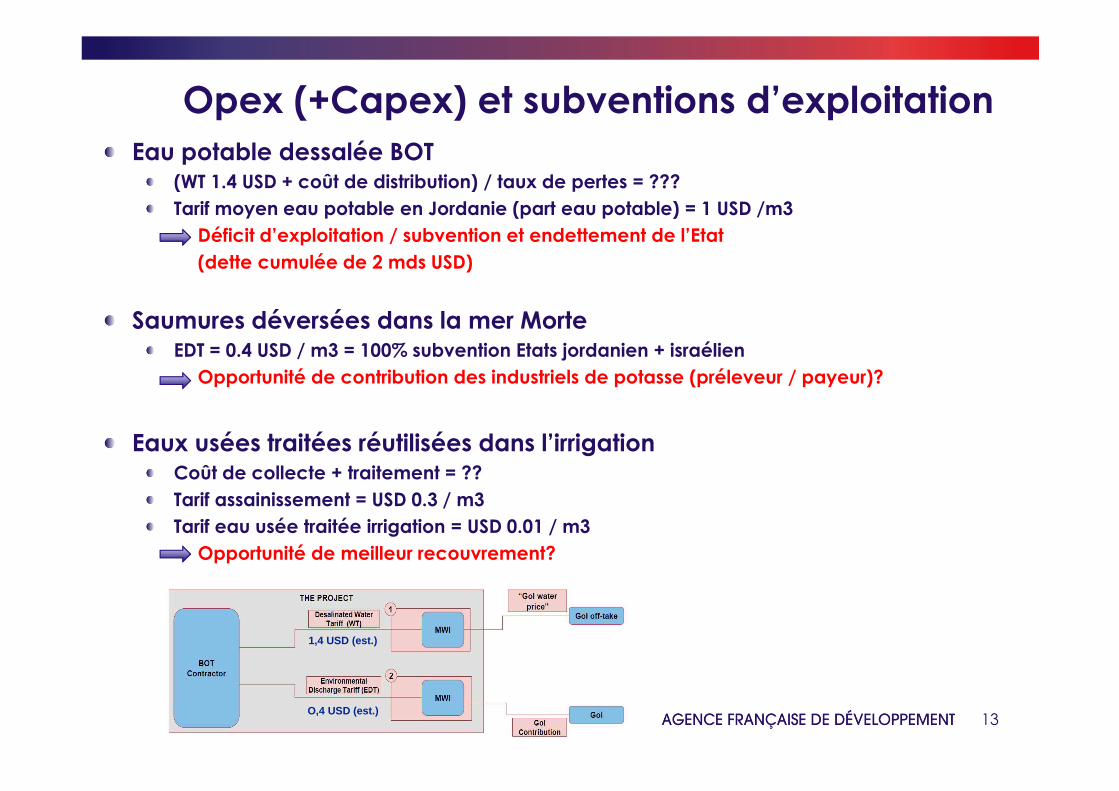

Opex (+Capex) et subventions d’exploitationEau potable dessalée BOT

(WT 1.4 USD + coût de distribution) / taux de pertes = ???

Tarif moyen eau potable en Jordanie (part eau potable) = 1 USD /m3

Déficit d’exploitation / subvention et endettement de l’Etat

(dette cumulée de 2 mds USD)

Saumures déversées dans la mer MorteEDT = 0.4 USD / m3 = 100% subvention Etats jordanien + israélien

Opportunité de contribution des industriels de potasse (préleveur / payeur)?

Eaux usées traitées réutilisées dans l’irrigationCoût de collecte + traitement = ??

Tarif assainissement = USD 0.3 / m3

Tarif eau usée traitée irrigation = USD 0.01 / m3

Opportunité de meilleur recouvrement?

1,4 USD (est.)

O,4 USD (est.)

14

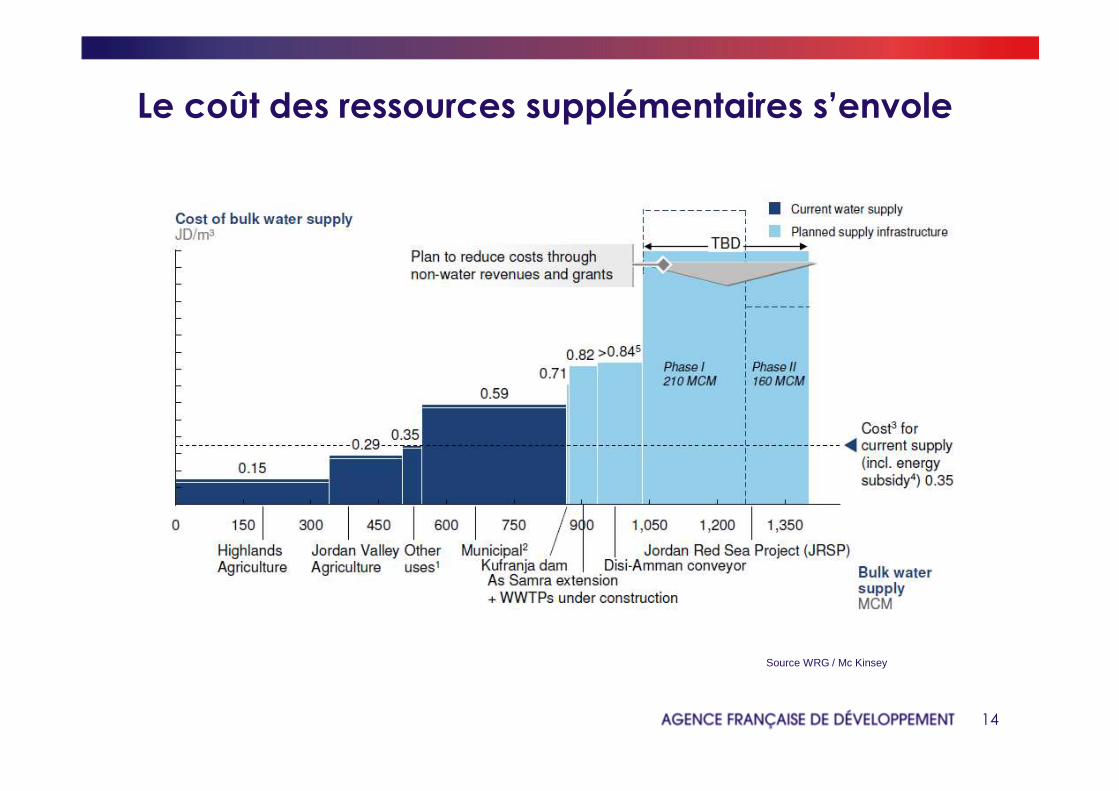

Le coût des ressources supplémentaires s’envole

Source WRG / Mc Kinsey

15

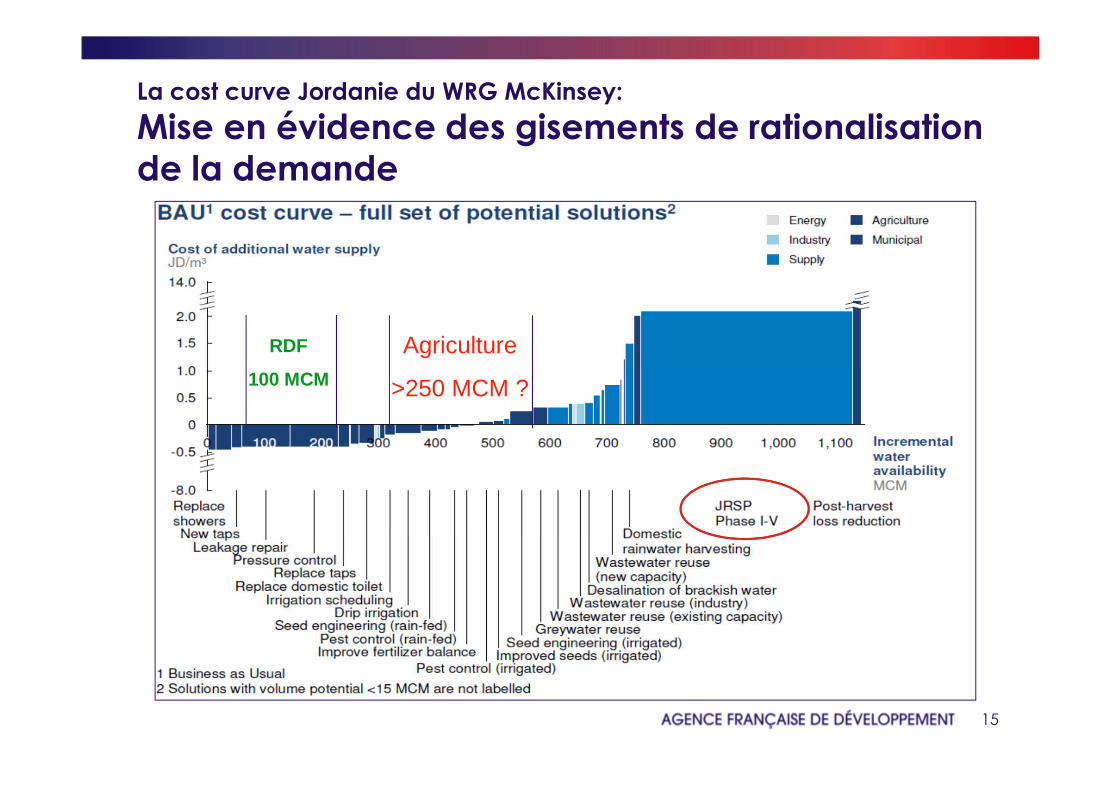

La cost curve Jordanie du WRG McKinsey:

Mise en évidence des gisements de rationalisation de la demande

Agriculture

>250 MCM ?

RDF

100 MCM

#WorldInCommonAGENCE FRANÇAISE DE DÉVELOPPEMENT | FRENCH DEVELOPMENT AGENCY

MERCI

afd.fr

1705.09.2017 Mer Rouge – Mer Morte

Génèse

Préfaisabilité 1995 - 1998 (Harza)

Mai 2005 : Jordanie, Israel et Palestine sollicite la BM pour mobiliser des fondset mettre en oeuvre la faisabilité

WB Trust Fund (16 MUSD, dont 3 MUSD de la France), démarrage des étudesen 2008